Paragraphes de la section

2023: a new balance for the power system, departing from the trends of the last decade

Overview

The year 2022 was marked by three independent and simultaneous energy crises that, combined, placed the French power system under strain: threats to gas supply following Russia's invasion of Ukraine, leading to a surge in prices; a crisis in French nuclear power generation (at its lowest since 1988); and a hydropower generation crisis due to low rainfall (at its lowest since 1976). Despite this very unfavourable context, the French power system showed resilience and managed to avert supply disruption. This can be attributed to the decrease in electricity consumption within France and neighbouring countries, well-functioning exchanges with neighbouring countries in accordance with the rules of operation of the European common market, and the securement of gas supplies.

During 2023, the determinants of security of supply returned to a more favourable situation:

- electricity generation from all low-carbon sources has increased significantly (nuclear power, hydropower, wind power, solar power);

- consumption decreased compared to the previous year, facilitating the coverage of demand, in line with the trend observed in the autumn of 2022;

- price levels decreased both on the spot market and the futures markets, with a reduction of the risk premiums held by market players;

- the electricity exchange balance once again became significantly export-oriented, reaching 50.1 TWh, and France reclaimed its traditional position as the leading electricity exporter in Europe (in volume);

- emissions related to electricity generation reached their lowest level since the early 1950s.

Thus, the power system returned to a situation of equilibrium, in which concerns about security of supply have been largely mitigated. This "new balance" does not, however, constitute a return to the pre-crisis situation, given the substantial evolution in the production of various sources and the consumption structure since the late 2010s.

Detailed analysis

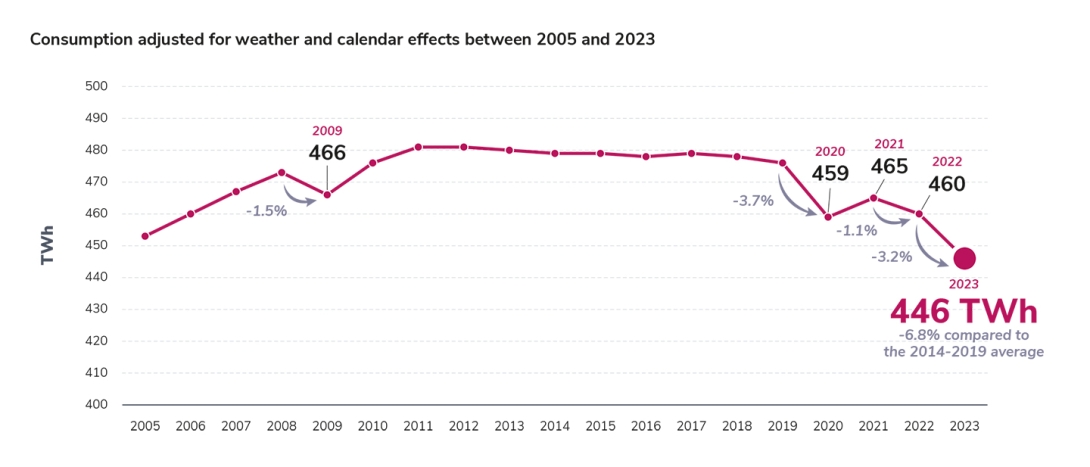

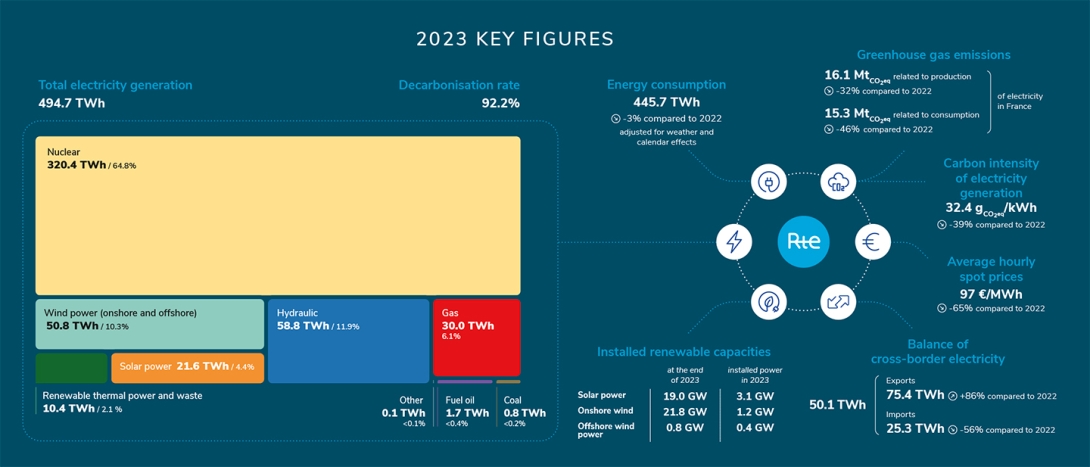

The clear downward trend of French consumption, which began in the autumn of 2022 amid the worsening energy crisis, continued throughout the year 2023. As a result, the volume of consumption (adjusted due to weather variations) for the year decreased by 3.2% compared to that of the previous year, reaching 445.7 TWh.

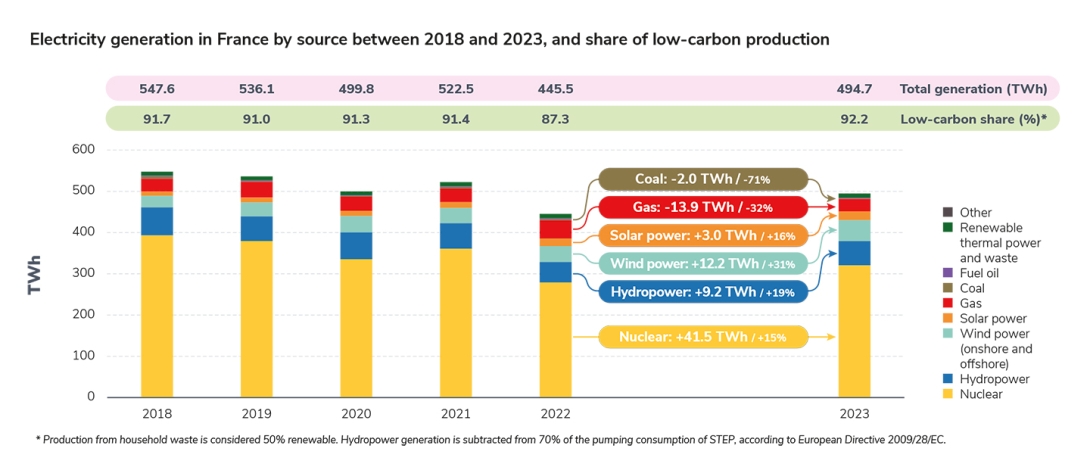

The total volume of electricity generation increased by 11% between 2022 and 2023 to 494.7 TWh, while remaining below pre-2020 levels.

- The availability of the nuclear fleet recovered during the year, compared to the historically low levels reached in 2022, but it remained significantly lower compared to that of the pre-crisis years. The volume of nuclear power generation rose to 320.4 TWh (compared to 279.0 TWh in 2022 and 394.7 TWh on average between 2014 and 2019);

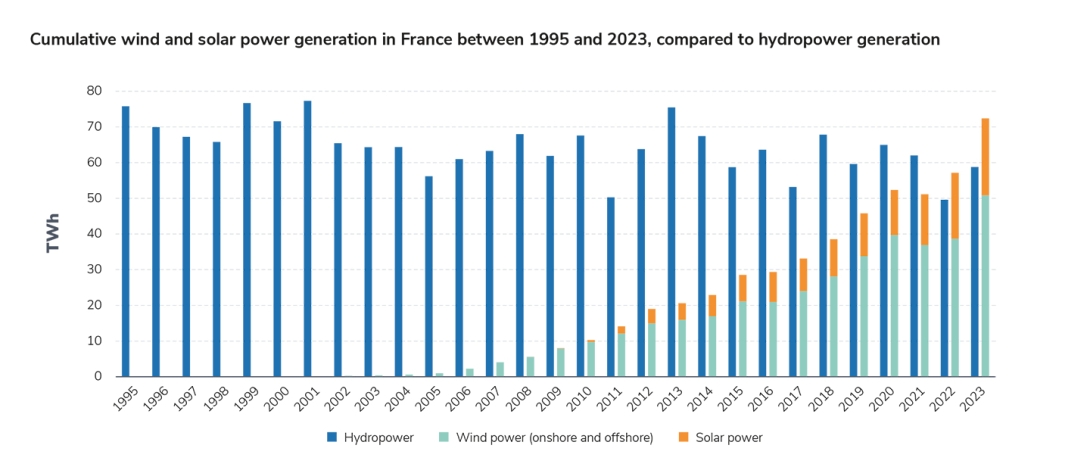

- The year 2023 was characterised by power generation records for both wind power (50.8 TWh) and solar power (21.6 TWh), which together accounted for nearly 15% of electricity generation, thereby contributing to security of supply and the increase in the supply of low-carbon electricity in France and in neighbouring countries through exchanges. In 2023, France saw record new generation capacity additions for solar power and offshore wind;

- Hydropower generation (58.8 TWh) maintained its position as the second-largest electricity source. Notably, there was a significant recovery compared to 2022, primarily attributed to more abundant rainfall that enabled reservoir levels to remain high throughout the year;

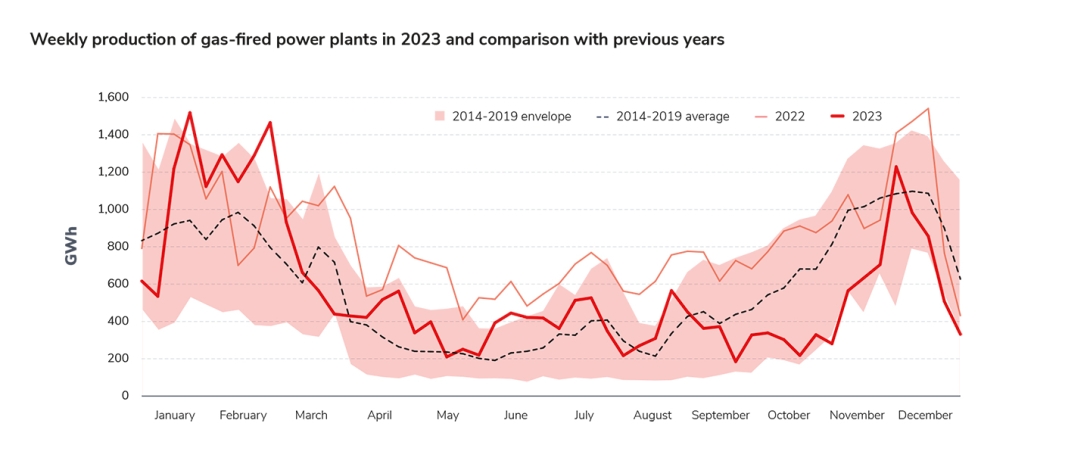

- The simultaneous reduction in demand and the increase in low-carbon production collectively diminished the reliance on fossil fuels, particularly gas (with gas generation decreasing from 44.0 TWh in 2022 to 30.0 TWh in 2023);

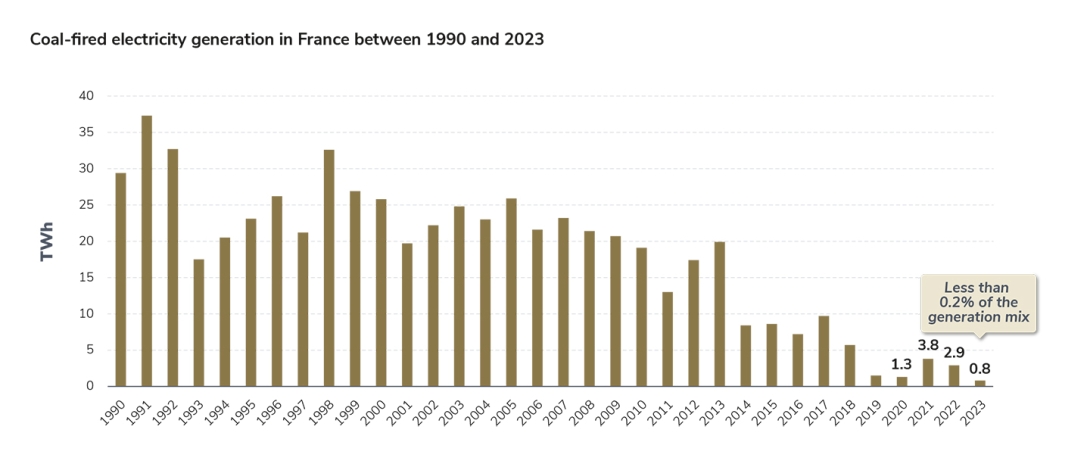

- The generation of electricity from coal has reached an unprecedented low and currently holds an insignificant position in the French energy mix (0.17% of French electricity generation in 2023).

Overall, low-carbon sources continued to largely dominate the electricity mix: for nearly twenty years, French electricity generation has been among those with the lowest emissions in terms of greenhouse gases in Europe. This was confirmed in 2023 with nearly 92% low-carbon production. These factors have strengthened the national power system's role as a key contributor to the decarbonisation of Europe’s electricity mix, through the export of a significant share of its low-carbon production.

The increase in electricity generation has led to reduced dependence on imports and increased export volumes: after an exceptional year in 2022, marked by a net import balance (16.5 TWh net yearly imports) for the first time since 1980, France returned to its traditional role as a net electricity exporter in 2023, with a balance of 50.1 TWh.

The easing of pressure on electricity supply had a positive impact on market prices, bringing them back to levels comparable to those seen in 2021. The sharp mismatch between forward prices and market fundamentals observed in 2022, reflecting a risk premium specific to France due to market players' fears about the security of supply (which were disproportionate to reality), gradually diminished in 2023, leading to a convergence between France and neighbouring countries1

1

For forward prices for delivery in the 1st quarter of 2024.

Consumption has declined, confirming the trend that began in 2022

In 2023, electricity consumption in France, adjusted for weather and calendar effects2,

represented 445.7 TWh, a decrease of 3.2% compared to the previous year, when consumption had already reached a low of 460.2 TWh due to the energy crisis. In 2023, it was 6.8% lower than pre-crisis consumption (average 2014–2019), below the level reached in 2020 (458.7 TWh), a year marked by the Covid pandemic from spring onwards, and a fortiori below that of 2021, when consumption slightly recovered (465.4 TWh). One has to go back to the early 2000s to find consumption levels comparable to those of 2023.

In addition, the decrease in consumption between 2022 and 2023 is one of the largest ever observed: it is more significant than those observed between 2021 and 2022 (-1.1%), and between 2008 and 2009 following the global economic crisis (-1.5%), and very close to the decrease in consumption between 2019 and 2020 (-3.7%).

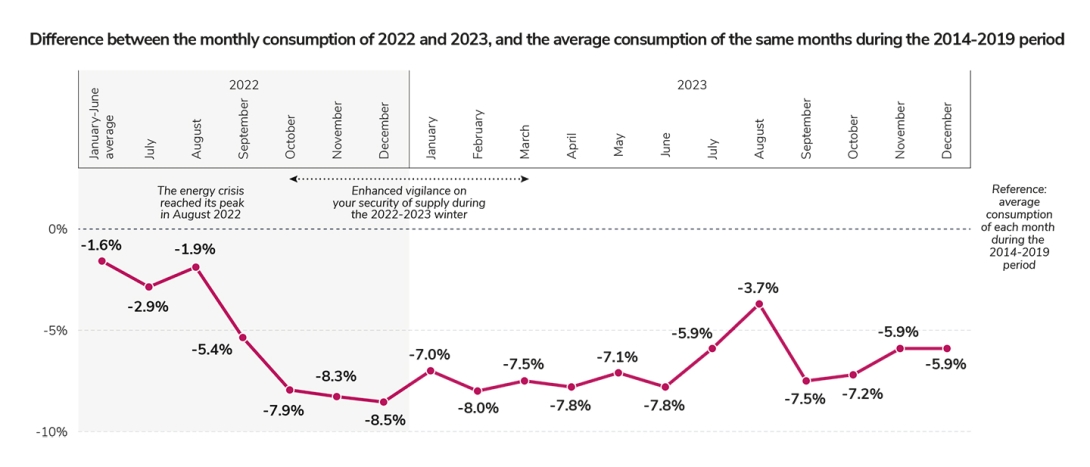

The downward trend observed in 2022, which intensified from autumn onwards at the height of the crisis, continued throughout 2023. This affected all sectors (residential, industrial, tertiary). The results of the survey carried out by RTE in partnership with the IPSOS institute on a large panel of French people (13,000 people) suggest that this reduction is not only the result of voluntary sobriety measures, but also stems from a reaction by the population and economic players to the rise in prices in the economy as a whole.

This prolonged fall in consumption is due, on the one hand, to ongoing efforts to promote energy savings in public administrations, in businesses and in households, with the launch of a second government plan in October 2023.

On the other hand, consumer surveys and the sharp fall in industrial consumption seem to indicate that the worsening macroeconomic situation was an even more decisive factor in the fall in electricity consumption in France and Europe, driven by persistent inflation (4.9% in 2023 compared with 5.2% in 2022, according to INSEE). In particular, 27% of the structural decline in consumption is attributable to large industrial consumers, even though this category account for only about 14% of total electricity consumption over the period 2014–2019. Companies are also more exposed to changes in energy prices than individuals: INSEE estimated at the beginning of 2023 that professional consumers would experience an 84% increase in electricity prices over the whole of 20233. For individuals who have opted for the regulated tariff, the price shield implemented in 2022 helped to smooth out and limit the impact of price hikes for households, even though its ceiling was raised twice in 2023 (first by an average of 15% on 1 February, then by an average of 10% in August).

The high temperatures in 2023, the second warmest year on record in France, have pushed "gross" consumption (without adjustment for climate effects) further down. It reached 438.7 TWh, its lowest level since 2002.

Due to the consequences of the energy and geopolitical crises, consumption has remained for several years at much lower levels than the figures observed until 2019. This trend is set to continue in the short term, against a backdrop of macro-economic constraints and the continuation of energy-saving measures, which for households have largely been based on simple gestures (lowering the temperature, switching off unnecessary lights and appliances on standby, adopting energy-saving cooking methods, etc.).

However, the effects of the current economic situation are part of a wider dynamic of changes in consumption patterns: development of energy efficiency, electrification of end-use consumption, changes in the production structure, energy saving. These changes are having contrasting effects, and should result in an upward trend over the next few years, which is necessary if France is to achieve its objectives of reindustrialising the economy and moving away from fossil fuels, although it is difficult to estimate when this upward trend will materialise given the uncertainties that characterise the current economic climate.

Graphe

Legend and filters

Normal and actual temperature

Last update: 29 February 2024 at 15:02

Legend and filters

>

Hide

- Incomplete year

- Preliminary data

Informations and sources

This graph compares the actual daily temperature with the normal temperature.

2

An adjustment that allows a comparison from one year to the next, regardless of weather variability, and an identification of the structural effects that affect the level of consumption.

Overall electricity generation is on the rise, thanks to the increase in renewables and the partial recovery in nuclear power generation

The total volume of electricity produced in France in 2023 reached 494.7 TWh, an 11% increase compared to 2022, a year which was characterised by an all-time low in production since 1992 (445.5 TWh).

However, French electricity generation in 2023 remains relatively low compared to recent history, and in particular lower than in 2020 (499.8 TWh).

Nuclear and hydropower generation volumes rose, after a particularly bad year in 2022, when they were hit hard, mainly by the crisis caused by stress corrosion cracking, but also partly by low rainfall. Nuclear power generation amounted to 320.4 TWh, an increase of 41.5 TWh compared to the previous year, thanks to better availability (corresponding to about four additional reactors on average over the year). However, this volume remains lower than those of previous years (394.7 TWh on average over the period 2014–2019). Hydropower generation amounted to 58.8 TWh, an increase of 9.2 TWh compared to the previous year, close to usual levels (61.7 TWh on average over the period 2014–2019), despite a period of marked drought at the beginning of the year.

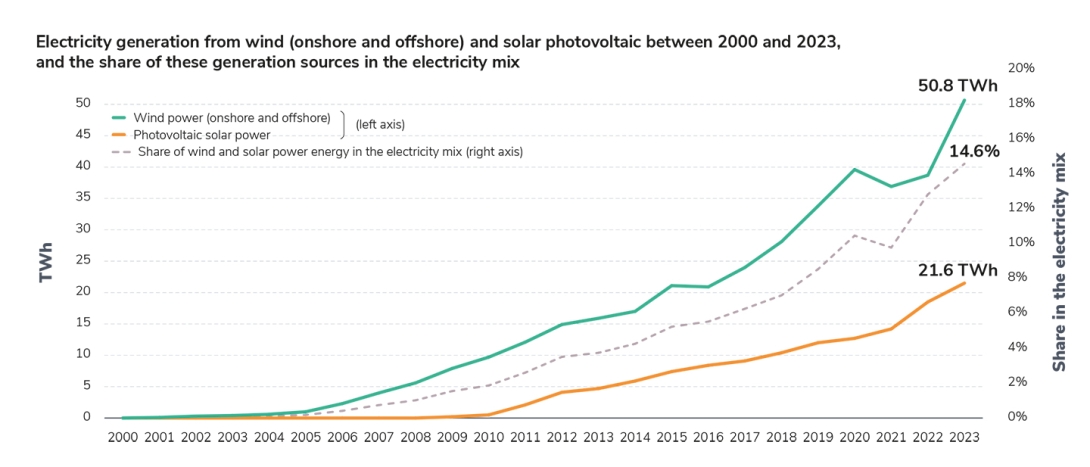

Wind and solar power generation reached record volumes. Wind power generation (onshore and offshore) has firmly gained the third place in the French generation mix, with 50.8 TWh produced (compared to 38.6 TWh in 2022), far surpassing the previous record of 2020 (39.7 TWh). This was made possible by an increase in installed capacity and a good load factor resulting from favourable weather conditions. Solar power generation amounted to 21.6 TWh, compared to 18.5 TWh in 2022, the previous record, thanks to the development of installed capacity. These energies sources are becoming a permanent part of the electricity mix, accounting for almost 15% of the generation mix in 2023.

The increase in low-carbon production (nuclear, hydro, wind and solar) made it possible to limit the use of fossil fuels for electricity generation: fossil-fuel thermal production reached its lowest level since 2014 (32.6 TWh), a decrease mainly driven by the reduction in gas-fired generation, from 44.0 TWh in 2022 to 30.0 TWh in 2023. Indeed, gas-fired generation was particularly in demand in 2022 to compensate for the low nuclear and hydropower generation. Generation from coal-fired power plants accounted for just 0.8 TWh in 2023, corresponding to 1.7 thousandths of the total production volume (less than 0.17% of the mix) and is now insignificant in the French electricity mix.

Nuclear power generation started to recover but is still far from its historic levels

In 2023, nuclear power generation rose to 320.4 TWh, an increase of 41.5 TWh compared to 2022, when the production volume reached an all-time low since 1988 (279.0 TWh), due in particular to the identification of stress corrosion cracking defects on certain reactors.

In 2023, nuclear generation remained by far the predominant source of electricity generation in France (65% of the mix); however, it remains at a low level, close to that of 19924, and a fortiori below the levels of the period 2014–2019 (an average of 394.7 TWh), and even that of 2020, when production was strongly affected by lockdowns5 (335,4 TWh).

Graphe

Legend and filters

Electricity generation from nuclear power plants in France

Last update: 29 February 2024 at 15:05

Legend and filters

>

Hide

Annual

Monthly

- Incomplete year

- Preliminary data

Informations and sources

This graph represents the evolution of electricity production in France from nuclear power plants. Annual and monthly nuclear power production balances are shown, and can be compared with each other.

- Nuclear generation was much lower un 2022 than in previous years, It was also lower than in 2020 which has been an exceptional year due to the health crisis. The drop in generation en 2022 is explained by the historical low availability of the fleet during the year.

The significant improvement in nuclear power generation compared to last year reflects the higher availability of the fleet, particularly from the end of the spring and throughout the second half of the year. Indeed, the availability of the nuclear fleet in 2023 clearly improved compared to 2022, which was marked by inspections and repairs linked to the phenomenon of stress corrosion cracking, as well as to a lesser extent by the densification of stops due to decennial inspections and the disruption of maintenance schedules following the Covid pandemic. The average availability in 2023, all factors combined, amounted to 38.6 GW (63% of the fleet), compared to 33.2 GW in 2022 (54%). Availability improved especially during the last four months of the year, as winter approached, close to the minimums of the pre-Covid range6. Two episodes of marked decline nevertheless characterised this period: the first due to a combination of events, including the effects of Storm Ciarán7(around the turn of October and November) and the second at the end of December, linked to an optimisation of the fuel stock in a context of low demand and high renewable production. During the same period, the increase in availability compared to that observed in 2022 was marked: 41.4 GW on average over these four months in 2023 compared to 31.4 GW in 2022.

Although the risk to security of supply was lower in 2023 than in 2022, the nuclear fleet has not returned to nominal operation.

The nuclear fleet's production has indeed recorded a structural decline compared to the maximums reached in the early 2000s. The closure of the two Fessenheim reactors accounts for part of this reduction, but it is far from the majority of it: the drop in availability between 2000 and 2021–2022 represents the equivalent of the closure of fourteen 900 MW reactors.

The reduction in nuclear power generation is not due to the development of renewables: modulating the output of reactors is a technical skill for their operators, enabling them to optimise production according to market prices (i.e., producing less during periods of low prices to save fuel and maximising output during periods of higher prices). In fact, there are very few situations in which modulation is "forced" due to a lack of demand (in such cases, nuclear power is often not the only one to modulate, as the most recent renewable fleets are also phased out).

This downward trend in nuclear power generation is due to the scale of the industrial programme required to extend the operating life of the reactors and to take into account the feedback from Fukushima. The Covid pandemic, by disrupting maintenance schedules at a critical time in the ramp-up of the biggest projects, and then the identification at the end of 2021 of a generic stress corrosion cracking defect, have ended up constraining an already highly optimised schedule.

Over the next decade, the challenge is to return to higher levels of availability and production than in recent years, which is one of the essential levers for achieving industrial objectives and initiating the transition to a low-carbon economy. In drawing up the ten-year projections in the latest “Bilan prévisionnel” (Generation Adequacy Report), RTE assumed a rapid return to an average annual production volume of around 360 TWh, including the Flamanville EPR, and considered a level of around 400 TWh, as in the 2010 decade, as a higher scenario8.

Graphe

Legend and filters

Nuclear capacity availability

Last update: 29 February 2024 at 15:07

Legend and filters

>

Hide

- Incomplete year

- Preliminary data

Informations and sources

This graph shows the availability of French nuclear power plants for electricity generation.

The daily available power values of nuclear power plants are presented over the last three years and can be compared with an average vision represented by the envelope over the 2015-2019 period.

- The availability drop in 2022 is due to outages for maintenance and inspections related to stress corrosion cracking, and is particularly wide in the summer as the maintenance operations were concentrated in these months in order to have maximum availability during the coldest periods.

4

The historic nuclear fleet was not yet fully in service with, at the time, several reactors under construction. Six reactors have been commissioned since 1992 (Penly 2, Golfech 2, Chooz B 1, Chooz B 2, Civaux 1, Civaux 2) and two reactors have been shut down (Fessenheim 1 and Fessenheim 2).

5

The closure of the Fessenheim power plant in June 2020 had led to a reduction in installed nuclear power capacity from 63.1 GW to 61.4 GW.

6

In accordance with the trajectories published by RTE in the autumn of 2023, the availability on 1 December was close to 43 GW, which reinforced the trend of improving the availability of the nuclear fleet for the winter of 2023–2024 compared to the two previous winters.

7

In particular, this has led to the shutdown of reactors at Flamanville and Paluel due to problems with the evacuation of generation from the grid.

Hydropower generation returned to levels in line with historical averages thanks to good stock replenishment

With a total of 58.8 TWh in 2023, hydropower generation increased by 19% compared to 2022 (49.6 TWh), a year affected by very low rainfall, during which production had reached its minimum since 1976. The hydropower generation source thus retained the second place in the French electricity mix ( 12% of the electricity mix), remaining the main renewable source ahead of onshore wind power.

Hydropower generation in 2023 was nevertheless below the average over the period 2014–2019 (61.7 TWh). Indeed, it was particularly low during the months of February and March as a result of low rainfall during the winter of 2022-20239 particularly in February, when a large proportion of annual production is usually concentrated. From October onwards, however, production volumes exceeded the highest levels observed during the period 2014–2019.

Graphe

Legend and filters

Evolution of hydropower generation

Last update: 29 January 2024 at 10:52

Legend and filters

>

Hide

Annual

Monthly

Global

Energy source

- Incomplete year

- Preliminary data

Informations and sources

Hydropower plants are an important part of the French electricity mix.

Hydropower plants can be divided into three categories, depending on the size of the reservoir upstream of the plant:

- Lake-type plants associated with a reservoir whose filling time exceeds 400 hours. Lake-type plants are managed on an annual basis, in order to use the available water when it is of maximum value to the power system, while respecting the technical constraints associated with water management in hydraulic valleys.

- Lock-type plants associated with a reservoir whose filling time is between 2 and 400 hours. Lock-type plants are managed on a daily to weekly basis.

- Run-of-river plants associated with a reservoir whose filling time is less than 2 hours. Run-of-river plants have low modulation capacities and their production is mainly conditioned by hydraulic inflows.

This graph gives a monthly and annual overview of hydropower production in France, broken down by sub-sector: lake, lock, run-of-river, other.

Water stocks reached very high levels compared with the previous year and the historical average from spring onwards, after a start to the year characterised by low rainfall, when they had remained close to average. These high stock levels were made possible by cautious management by operators at the start of the year due to low rainfall and by the improvement in rainfall from the spring onwards. The availability of good levels of hydropower stocks was a very favourable element for security of supply during the winter of 2023–2024.

Graphe

Legend and filters

Evolution of water reserves

Last update: 29 February 2024 at 15:22

Legend and filters

>

Hide

- Incomplete year

- Preliminary data

Informations and sources

This graph presents an aggregated view of the producibility contained in water reserves in France.

- The use of water in hydraulic dams is managed in such a way as to optimally distribute the production of the power plants concerned over time, by arbitrating between immediate use, or deferred use in substitution of more costly means of production. This is achieved by estimating the opportunity cost of deferred use of the power plant (or use value). The plant only produces at a given time if the market value of the electricity exceeds the opportunity cost of future use. The value depends on the time in question, the level of consumption, the level of remaining stock, as well as that of other modeled stocks and expected future prices for fuels and electricity. It may therefore happen that the use value of lake hydropower is higher than the cost of thermal power.

- The graph shows, for each year, the evolution of water reserves in aggregated vision and converted into electrical producibility. The evolution of the hydraulic stock depends on the inflows received and the quantity of electricity produced by the hydropower plants.

.

9

The 2022–2023 meteorological winter was characterised by a rainfall deficit of 25% on average. In particular, this deficit reached an exceptional level in February. The low rainfall during the winter of 2022–2023 also led to a lack of snow on all the French massifs. – Météo-France, Climate report 2023, 2024

Wind and solar power generation reached record levels, the solar fleet grew in an unprecedented manner

Wind and solar power generation reached record levels in 2023: 50.8 TWh for wind power and 21.6 TWh for photovoltaic solar power. Together, these two sources surpassed hydropower generation for the second year in a row, while hydropower generation returned to usual levels in 2023: this shows that these variable renewable energies already occupy an important part of the French electricity mix, accounting for nearly 15% of total production, and also contributing to security of supply (see the Flexibilities section).

Graphe

Legend and filters

Wind power generation in France

Last update: 29 January 2024 at 10:55

Legend and filters

>

Hide

Annual

Monthly

Global

Energy source

- Incomplete year

- Preliminary data

Informations and sources

This graph gives an annual and monthly overview of wind power generation, both overall and by sub-sector: onshore wind power, offshore wind power.

- The development of wind power production is an important parameter in the energy transition, since it is a renewable and low-carbon energy source. Wind power generation in France began to develop with the construction of onshore wind farms. In 2022, the first offshore wind farm went into service.

- In 2022, despite relatively unfavourable weather conditions, output rose on the back of expanded capacity.

The data can be of various kinds:

- Data from RTE meters and distribution network operators. In order to draw up global consumption or production balances, we need to have an aggregated view of all metering data on the transmission and distribution perimeters. These data are only available on the 15th of each month for the month just ended. Although updates are possible for at least 12 months, the consolidated data is very robust from the first date of availability.

Provisional data, derived from telemetry set up by network operators at various points on the power grid, supplemented by estimates for non-telemetered production or consumption. Provisional data provide an initial overview, available very quickly after each deadline; they are not of the same quality as metering data (estimates taken into account, less accurate measurement than metering data, etc.). Graph elements based on provisional data are indicated by a specific pictogram on the portal.

Graphe

Legend and filters

Solar power generation in France

Last update: 29 February 2024 at 15:05

Legend and filters

>

Hide

Annual

Monthly

- Incomplete year

- Preliminary data

Informations and sources

This graph provides an annual and monthly overview of solar power generation in France.

- The evolution of solar photovoltaic generation is an important parameter in the energy transition, as it is a renewable and low-carbon energy.

- In 2022, solar power generation rose sharply on the back of expanded capacity and good sunlight.

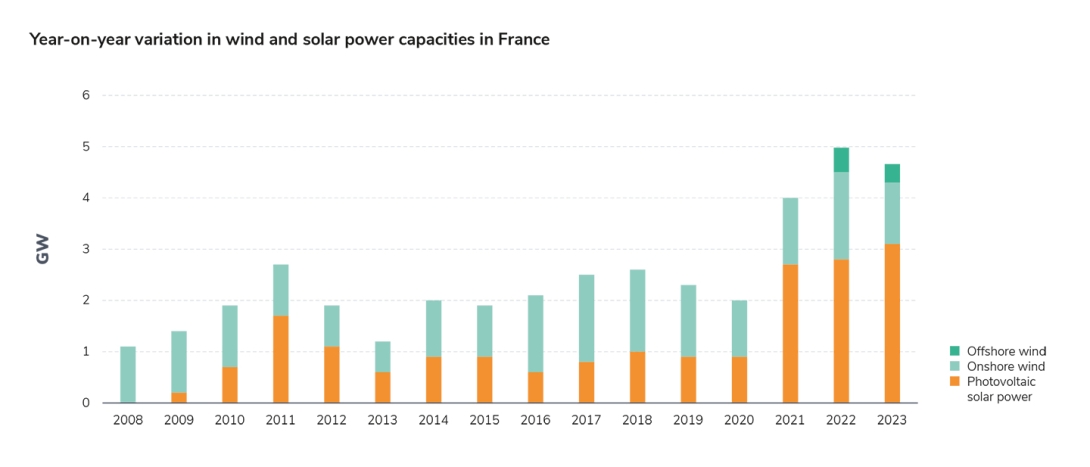

In particular, onshore wind power generation (48.9 TWh) has far surpassed the previous record of 2020 (39.7 TWh) thanks to the combined effects of favourable weather conditions and an installed fleet that has continued to grow. The average load factor for onshore wind power was 26.2%, the second highest in the last decade after that of 2020 (26.6%) which had been particularly windy. Since 2022, offshore wind power generation has begun to be visible in the French generation mix: with three wind farms, one of which has been fully in service since the end of 2022 (St-Nazaire) and two of which are being deployed in 2023 and whose installation is expected to be completed in 2024 (St-Brieuc and Fécamp), offshore wind power accounted for 1.9 TWh in 2023, compared to 0.6 TWh in 2022.

Wind power generation is generally higher during the autumn and winter months, due to higher winds during this period: this was particularly true in 2023, when wind power generation reached unprecedented levels during the months of January, March, November and December, close to or exceeding 6 TWh for each of these months. Wind power has thus contributed to security of supply during the cold seasons, making it possible to limit the use of fossil fuel-fired power plants. In 2023, the volume of wind power generation far exceeded that of gas-fired power plants (30.0 TWh).

Similarly, the combined effects of an expanding solar fleet and normal levels of sunshine10 have made it possible to produce 21.6 TWh of photovoltaic origin, surpassing the previous record of 2022 (18.5 TWh).

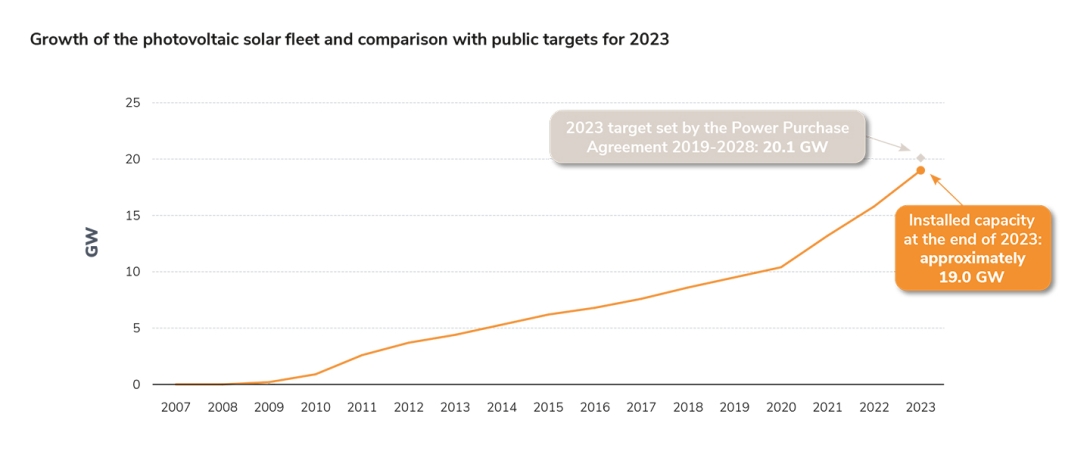

The installation of photovoltaic capacities has also increased at an unprecedented rate, with an installed capacity of 3.1 GW (compared to 2.7 GW in 2021 and 2.8 GW in 2022), marking the start of a necessary acceleration in the years ahead. The photovoltaic solar fleet thus increased from 15.9 GW at the end of 2022 to 19.0 GW at the end of 2023.

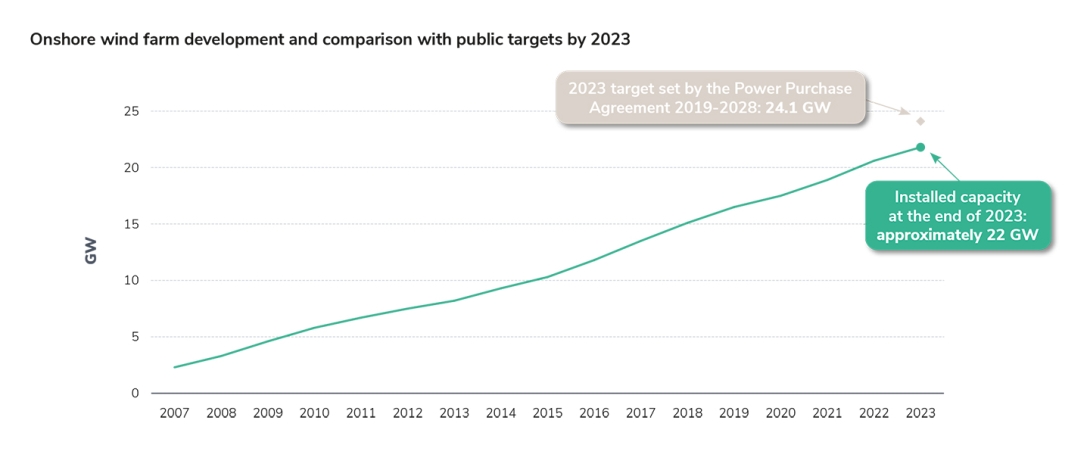

On the other hand, the rate of installation of onshore wind power has slowed slightly compared to the average rate of development in recent years: power from onshore wind farms increased by 1.2 GW in one year, from 20.6 GW at the end of 2022 to 21.8 GW at the end of 2023, compared to 1.4 GW on average over the previous five years. At the same time, the development of offshore wind farms is continuing: after the first wind farm offshore of Saint-Nazaire (480 MW), completed at the end of 2022, two other wind farms are being installed offshore of Fécamp and Saint-Brieuc. The latter will eventually represent nearly 500 MW each and should be completed in 2024: at the end of December 2023, the installed capacities reached 224 MW and 136 MW respectively.

Despite the good progress of the two generation sources in 2023 compared to previous years, the installed capacities did not make it possible to achieve the objectives that had been set by the public authorities on this horizon11 with a slight difference for solar power (1.1 GW) and a greater delay for onshore wind power (2.3 GW) and offshore wind power (1.6 GW). These delays correspond to about four months of development for solar power, at the average rate of installation over the last five years, and about one and a half years of delay for onshore wind power. To achieve the objective concerning offshore wind power, approximately two additional wind farms, in addition to the finalisation of those of Fécamp and Saint-Brieuc, would be necessary.

The acceleration of the development of renewable energies is an essential lever for rapidly increasing low-carbon production, particularly over the next decade, to achieve the European decarbonisation objectives of 2030 and a carbon-neutral economy in 205012. The French energy strategy will be specified during 2024 thanks to the programmatic declarations backed by the SFEC, in particular, the decree on the future multiannual energy plan for the period 2024–2035. The information made available in November, which was submitted to public consultation, shows an objective of maintaining the trend rate of installation of onshore wind power (approximately 1.5 GW/year) and an acceleration of the deployment of photovoltaic capacities (by doubling the rate to between 5.5 and 7 GW/year). With regard to offshore wind power, a new objective of 45 GW in 2050 was announced in 2023. As provided for by the acceleration law adopted in March 2023, the modalities of public debate have evolved from a project-based approach to a global approach by facade. In particular, the French national commission for public debate has organised a national debate on planning for all of metropolitan France's maritime facades, open until the end of April 2024. This overall planning aims to support an ambitious increase in installed capacity, with an objective of 18 GW in 2035.

11

2023 objectives according to the second Multiannual Energy Plan (2019–2028): 24.1 GW for onshore wind power, 2.4 GW for offshore wind power, 20.1 GW for solar power.

12

Please see the Bilan prévisionnel (Generation Adequacy Report) published by RTE in the autumn of 2023, in particular the Production chapter.

The fossil-fuel thermal fleet has been used much less than in 2022, thanks to the recovery in nuclear and hydro power, the increase in renewable production and the fall in consumption

In 2023, the volume of fossil fuel thermal production decreased by 34% compared to the previous year, across all generation mixes, from 49.2 TWh in 2022 to 32.6 TWh in 2023, its lowest level since 2014. This decline was mainly driven by that of gas-fired production. The increase in carbon production that took place in 2022, at the height of the energy crisis, came to an end in 2023, with the power system returning to a level of operation close to that of previous years: this was indeed a one-off, temporary phenomenon, which does not appear likely to call into question the long-term trend towards a reduction in the use of fossil fuels in French electricity generation.

Graphe

Legend and filters

Evolution of fossil-fired thermal generation

Last update: 29 January 2024 at 10:55

Legend and filters

>

Hide

Annual

Monthly

Global

Energy source

- Incomplete year

- Preliminary data

Informations and sources

This graph presents annual and monthly fossil-fired thermal generation, in total or segmented by type of fossil-fired thermal generation: oil, coal and gas.

The data can be of various kinds:

- Data from RTE meters and distribution network operators. In order to draw up global consumption or production balances, we need to have an aggregated view of all metering data on the transmission and distribution perimeters. These data are only available on the 15th of each month for the month just ended. Although updates are possible for at least 12 months, the consolidated data is very robust from the first date of availability.

Provisional data, derived from telemetry set up by network operators at various points on the power grid, supplemented by estimates for non-telemetered production or consumption. Provisional data provide an initial overview, available very quickly after each deadline; they are not of the same quality as metering data (estimates taken into account, less accurate measurement than metering data, etc.). Graph elements based on provisional data are indicated by a specific pictogram on the portal.

The increase in fossil-fuel production in 2022 mainly concerned gas production: not surprisingly, it is the reduced recourse to this source (30.0 TWh compared to 44.0 TWh in 2022) that has dragged down production from fossil fuels in 2023. This is the result of the increased availability of the nuclear fleet and the increase in hydro, wind and solar power generation, as well as the drop in consumption in the last months of 2022. The gas-fired production source returned to fourth place in the electricity mix (6% ), behind wind power (10%) as was the case in 2020 and 2021. With the exception of January and February 2023, months characterised by low rainfall, which affected hydropower generation, and by the still very low availability of the nuclear fleet, gas-fired power generation was generally within the range of production volumes for the period 2014–2019. In the last quarter, it was even clearly at the low end of the historical envelope due to high volumes of hydropower and wind power generation against a backdrop of low consumption.

The production from coal, which had already been extremely low in 2022, decreased further to represent, in 2023, only 0.8 TWh, or 0.17% (1.7 thousandths) of electricity generation in France. The two power plants still in operation at the end of 2023 operated on an ad hoc basis during the first months of the year, but production was negligible over the rest of the year, including in November and December. The exit of coal in France is already almost effective as far as the volumes produced are concerned.

13

Between 2001 and 2007 inclusive, the "Other" series included generation from distribution networks, generation from derived gases and generation from "miscellaneous" fuels. Between 2008 and 2010, it contained derived gases and miscellaneous fuels, while the production of distribution networks was divided between fuel oil and gas. From 2011, all the entities in the "Other" series have been broken down into the gas, fuel oil and coal series.

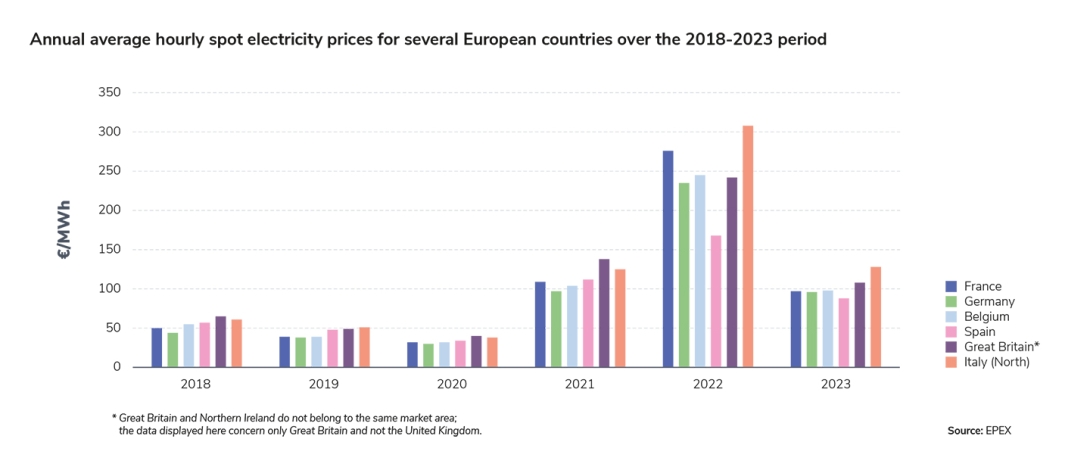

Electricity prices on wholesale markets have fallen significantly compared to 2022, but without returning to pre-crisis levels

In 2022, electricity prices reached unprecedented levels on wholesale markets, as a result of the triple energy crisis that simultaneously affected nuclear power generation in France, hydropower generation in southern Europe and gas prices following Russia's invasion of Ukraine. In 2023, due to the improvement in nuclear power and hydropower generation, the drop in gas prices and a low level of consumption, electricity prices showed a significant drop from €276/MWh in 2022 to €97/MWh in 2023 as an annual average for "spot" prices.

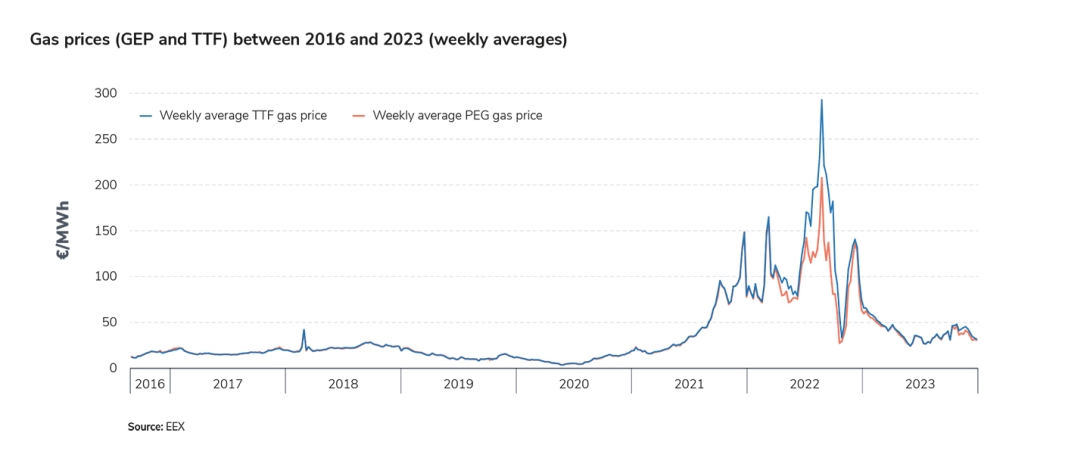

The year 2022 was characterised by an exceptional increase in gas prices on the European market, which reached its peak in the summer. In fact, this increase continued a dynamic that began in the second half of 2021, before the start of the war in Ukraine. At the time, this upward movement was interpreted as the result of a mismatch between gas supply and demand due to the effects of the economic recovery, which led to an increase in energy consumption as the Covid crisis drew to a close against a backdrop of supply chains still disrupted by the crisis. It has now been established that supply restriction manoeuvres on the part of commercial operators linked to Russia have contributed to this increase, in particular by underfilling the stocks held by these players in Europe from summer 202114.

Thus, gas prices reached record levels at the end of 2021 at around €100/MWhth, whereas they have been relatively stable for many years, reaching around €20/MWhth at the beginning of 2019 and €10/MWhth at the end of 2019. Russia's invasion of Ukraine and growing uncertainties over gas supplies then exacerbated the crisis, which peaked in August 2022, with prices above €200/MWhth on average over the month, and above €300/MWhth over the past week.

Since then, tensions between gas supply and demand in Europe have subsided under the effect of two dynamics: on the one hand, action on the supply side, with the diversification of supplies to European countries thanks to the wide use of LNG15 made possible in particular by the construction of new infrastructure (temporary regasification terminals), and on the other hand, the reduction in demand as a result of high prices. As a result, gas stocks at the end of 2023 reached a higher level than the average of the last five years. Consequently, gas prices have fallen significantly, at around €40/MWhth on average over the year 202316, more than half the average for 2022. Despite this considerable fall, prices remain high by historical standards: the replacement of cheaper Russian pipeline gas by LNG is likely to keep prices at higher levels over the long term than those seen until the end of the 2010s.

The fall in gas prices has been one of the determining factors for the reduction in electricity prices on wholesale markets in France. Indeed, despite the low volume of production from fossil fuels, electricity prices in France remain very sensitive, particularly to gas prices, due to France's position at the heart of the European interconnected system and the market price formation mechanism.

The other factors that have contributed to the fall in prices are the decrease in European electricity demand on the one hand, combined with the increase in supply on the other hand (recovery in French nuclear power generation, better production from hydraulic dams, and continued growth in renewable production throughout Europe). These are the same factors which, by reducing the need to call on expensive production resources (mainly in other European countries), have led France to regain its export position (see the next section).

The annual average hourly spot prices in France have thus dropped from €276/MWh in 2022 to €97/MWh in 2023, so they have been almost divided by three, even if the price level remains high compared to those recorded before the triple energy crisis.

Graphe

Legend and filters

Spot electricity prices in France

Source : EPEXLast update: 29 February 2024 at 15:28

Legend and filters

>

Hide

Weekly

Daily

- Incomplete year

- Preliminary data

Informations and sources

This graph compares the evolution of spot electricity prices in the French market. The values shown are weekly averages of spot prices.

Electricity spot markets are used to buy and sell electricity the day before for the next day, on a European perimeter.

General conditions of use of EPEX SPOT data

Without prejudice to the provisions of the present article, all data originating from EPEX SPOT SE are the exclusive property of EPEX SPOT SE or its subsidiaries. The user of the Analysis and Data Portal is however authorized to consult the data made available via the Analysis and Data Portal for internal and/or personal use.

Any other use of data from EPEX SPOT SE by the user is strictly prohibited without the express consent of EPEX SPOT SE, in particular :

- any commercial use,

- the creation of any financial instrument or reference index for external use or for the benefit of third parties,

- any copy, distribution, marketing, exploitation or use with or for the benefit of third parties.

The user of the Analysis and Data Portal acknowledges that he/she is responsible to EPEX SPOT SE for compliance with these conditions by his/her employees, managers and service providers.

Source : EPEX

The extent of price changes in 2023 was much less spectacular than in 2022. Spot prices were at their highest in the first quarter of 2023, when nuclear availability was still very low, rainfall below normal and gross consumption higher due to the winter period. From spring onwards, the normalisation of rainfall, which led to the replenishment of hydropower stocks, and the improvement in the availability of nuclear power led to a drop in prices, which fell below €100/MWh on average. During the rest of the year, prices remained around this level, with more pronounced declines during periods of high renewable production.

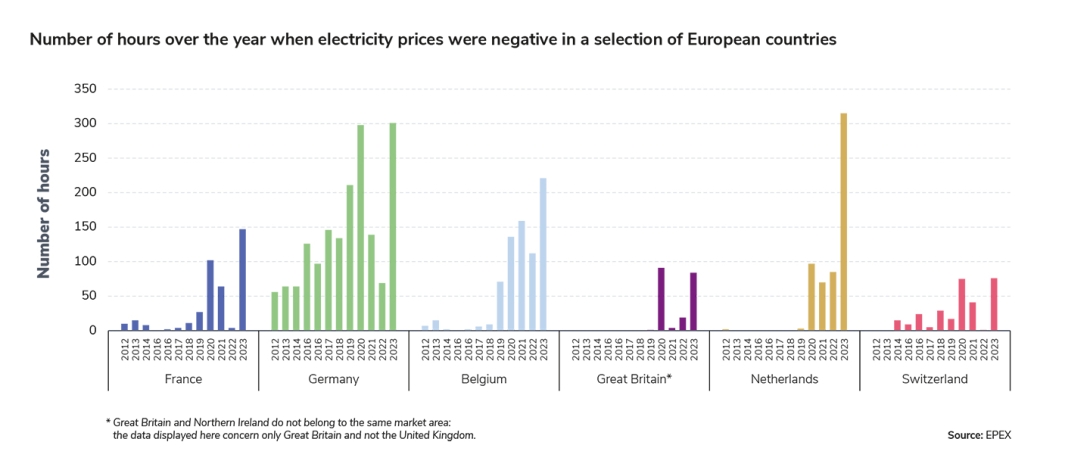

In addition, in 2023, France experienced an unprecedented number of negative price episodes, amounting to 147 hours over the year. 2020, a year marked by the decline in consumption linked to the Covid pandemic, experienced 102 hours of negative prices. In 2023, these episodes were mainly concentrated during the summer, due to the high level of photovoltaic production. With 47 hours of negative prices in July, for the first time since 2020, the average spot price was negative for one day, on Sunday 2 July 2023 (-€1/MWh).

The European power system is characterised by a structural increase in the number of negative-priced episodes over the last five to ten years, linked to the development of variable renewable production capacities: in 2023, Germany experienced 301 hours at negative prices, Belgium 222, the Netherlands 316. These negative price episodes occur at times when renewable generation is particularly strong, until production exceeds consumption. For producers with non-flexible production resources, it may be more economically attractive to continue to produce rather than to stop and then restart production units: in these cases, they can offer negative prices on the market, which means that the players who buy on the market are paid to consume electricity produced in quantities that are too abundant compared to the consumption needs at these specific times. The multiplication of these episodes highlights the importance of structurally changing the consumption profile, in particular by shifting a greater volume of consumption over the long term to the hours in the middle of the day, when solar power generation is at its highest; on the other hand, it demonstrates the importance of developing demand-side flexibilities, to dynamically adapt consumption to variable production over the short term.

On average, prices followed similar dynamics in all European countries, with a surge in 2022 followed by a sharp decline in 2023, but without prices returning to pre-crisis levels. In 2022, prices in Spain and Portugal rose less than in other European countries under the effects of the subsidy mechanism for thermal power plants (gas in particular) set up by these two countries (the “Iberian mechanism”). The latter continued to apply the rules of operation of the European market but imposed a ceiling on the price of gas for electricity generation, granting gas-fired power plants compensation to cover the difference between this ceiling price and the market price of gas17. In 2023, Spanish prices were among the lowest thanks to the high level of renewable production, with the ceiling imposed by the "Iberian mechanism” virtually no longer having any effect due to the drop in gas prices. In 2023, prices in Great Britain, a country whose electricity mix is heavily dominated by gas, were once again, on average, higher than in France, in contrast to 2022, when Great Britain exported exceptionally high volumes to France.

15

Abbreviation for "liquefied natural gas"

16

PEG gas prices.

17

See the Economic analysis chapter of the “Bilan prévisionnel 2023–2035” (Generation Adequacy Report) for a discussion of this mechanism, which it would not be possible to transpose to France with the same effects, unless it were implemented simultaneously in all interconnected countries.

Forward prices in 2023 for delivery in the 1st quarter of 2024 also decreased, in line with the trend started at the end of 2022 with the improvement in the determinants of the supply-demand balance. These prices, observed in 2022 for delivery at the beginning of 2023, reflected the existence of a risk premium specific to France, which appeared to be overestimated in view of the fundamentals of the supply-demand balance (see the RTE analyses for the winter of 2022–2023, and the "Economy" chapter of the “Bilan prévisionnel 2023” – Generation Adequacy Report). This led to a decorrelation between the prices at which futures markets were traded and the equilibrium price corresponding to market fundamentals. This risk premium collapsed at the beginning of the winter of 2022–2023 as uncertainties over supply capacity diminished (renewed nuclear availability, lower consumption, above-seasonal temperatures).

The risk premium specific to France reappeared in the spring of 2023, following the discovery of new defects related to the phenomenon of stress corrosion cracking on repaired welds. It subsided from the end of the summer and throughout the winter of 2023-2024: forward electricity prices are now consistent with market fundamentals and realigned with those of neighbouring countries, although they remain higher than before the 2022 energy crisis and are also characterised by greater volatility. However, the determinants of the price drop observed in 2023 (drop in consumption, strong renewable production and development of renewable energy in France and especially in Europe, improvement in the availability of nuclear power) seem to persist and anticipate a possible trend in prices towards relatively low levels.

The specificities of the French generation mix create a structural misalignment between market prices, which are often fixed at the level of gas-powered units, and production costs, which are lower for low-carbon methods. This misalignment does not result from an "indexation" of prices to those of thermal production methods, but it is the result of market balances that are created at the European level. The European electricity market operates according to a logic of economic precedence (merit order), which leads the spot price of electricity to form every hour at the variable cost of production of the last unit called to cover demand. This is because producers have an incentive to start generating power as soon as the market price exceeds their marginal cost of production (if the price is lower than the marginal cost of production, the producer will not be able to cover their costs, and in the opposite case, not generating power would result in a loss of income). The surge in wholesale electricity prices led the Member States of the European Union to ask the European Commission for a structural reform of the European electricity market, which was presented on 14 March 2023. This reform allows Member States who wish to do so to promote various tools, such as long-term contracts that can take the form of contracts for difference (CfD) or long-term bilateral commitments (power purchase agreements - PPAs). Alongside this work, a number of proposals for dealing with the repercussions of the crisis have stimulated public debate, particularly in France. Against this backdrop, on 14 November 2023, the public authorities presented a proposal for a system to protect electricity consumers, based in particular on the principle of taxing the income earned by EDF from its historic nuclear power plants, the precise terms of which were the subject of a dedicated consultation.

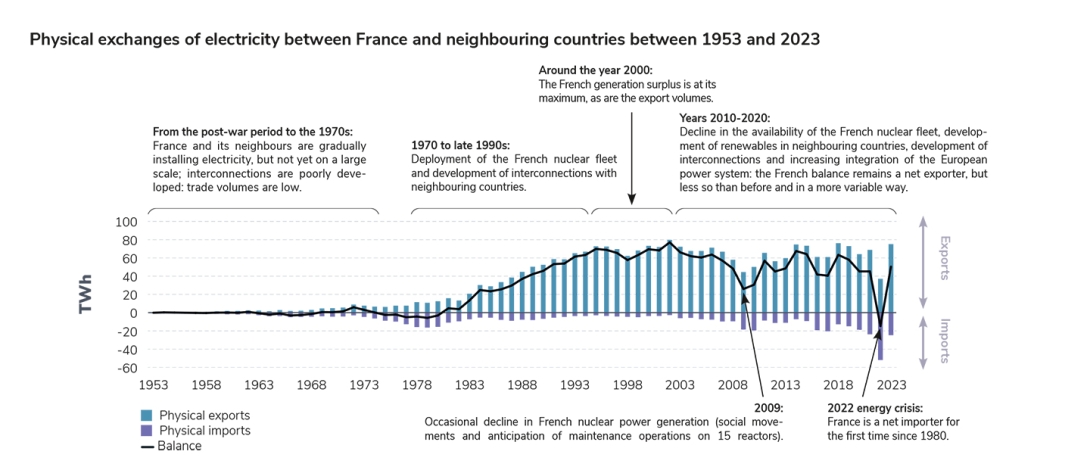

France has returned to its usual role as a net electricity exporter

In 2023, the balance of electricity exchanges between France and neighbouring countries was once again in export mode, amounting to 50.1 TWh. In 2022, the balance was reversed, reaching 16.5 TWh in terms of imports, under the effects of the nuclear and hydro power generation crisis, while France had been a net exporter every year since 1981.

The level of the balance in 2023 is in line with the average for the last decade, reflecting the improvement in the determinants of the supply-demand balance. During the year 2023, the exchange balance was in import mode 12% of the time, well below 67% of the year 2022, while remaining a slightly higher level than those of the years 2010 (7% on average over the period 2014-2019). These figures do not mean that France's security of supply has been based on imports 12% of the time, but they do reflect an evolution in the patterns of electricity exchanges. This gap between the year 2023 and historical levels is, on the one hand, linked to the level of nuclear power generation in France, which is still low in 2023 compared to pre-crisis levels. On the other hand, it reflects the gain in competitiveness of the electricity mixes of neighbouring countries due to their gradual decarbonisation, which allows France to import inexpensive electricity in the event of high renewable production in other European countries.

Graphe

Legend and filters

Electricity trade balance between France and its neighbours

Last update: 02 April 2024 at 14:32

Legend and filters

>

Hide

Annual

Monthly

- Incomplete year

- Preliminary data

Informations and sources

This graph represents an annual and monthly overview of the electricity trade balance between France and its neighbours.

- Increasing interconnections between regions has long been a priority of the European Union's energy policy. The operation of the power system at the European scale is a reality, and it proved essential when the system was under strain during the autumn and winter 2022/2023.

- In past years, France has mostly been a net exporter to neighbouring countries, but significant supply tension in 2022 caused the situation to reverse, with France ending the year as a net importer.

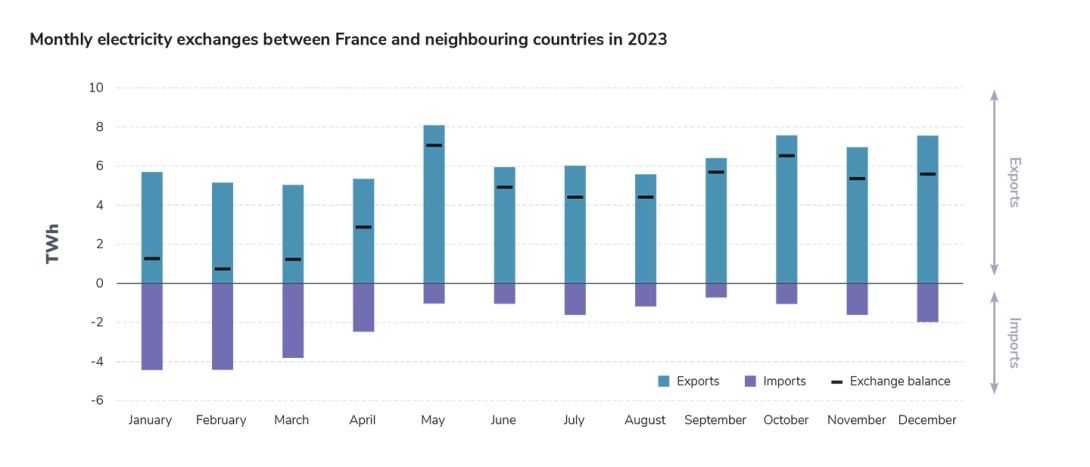

Although the balance was negative for all the months of 2023, it remained close to equilibrium in the first quarter, reflecting the constraints on hydropower generation due to low rainfall and the still very low availability of nuclear power at the start of the year. The volume of imports fell sharply from April, and the balance reached high levels until the end of the year, with a maximum of 7.1 TWh in the direction of exports in May, thanks to lower levels of consumption and the arrival of warmer temperatures. Unlike in 2022, when the energy crisis reached its peak in August, leading to large volumes of imports over the summer, French production was in surplus in the summer of 2023, thanks to the resumption of nuclear power generation, and was therefore able to be exported in large volumes.

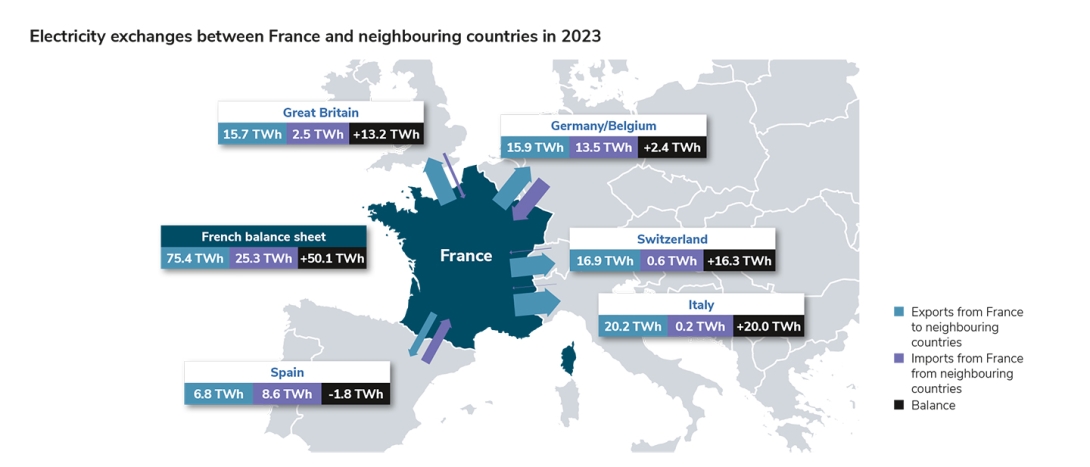

The analysis of exchanges by border shows that the balance was largely export-oriented at the Swiss (annual balance of 16.3 TWh) and Italian (20.2 TWh) borders, which has been the case for nearly twenty years (including in 2022). France became a net exporter to Great Britain again (13.2 TWh), a situation that was usual in the years before the energy crisis but which had reversed in 2022 at the height of the crisis. The balance was also slightly export-oriented (2.4 TWh) at the borders with Germany and Belgium (Core18 region), unlike in 2021 and 2022. This slightly export-oriented balance reflects contrasting trade patterns over the year (on a monthly basis, France was an importer until April, then the direction of trade was reversed until the end of the year). In contrast, France was slightly import-oriented in relation to Spain over the year (-1.8 TWh).

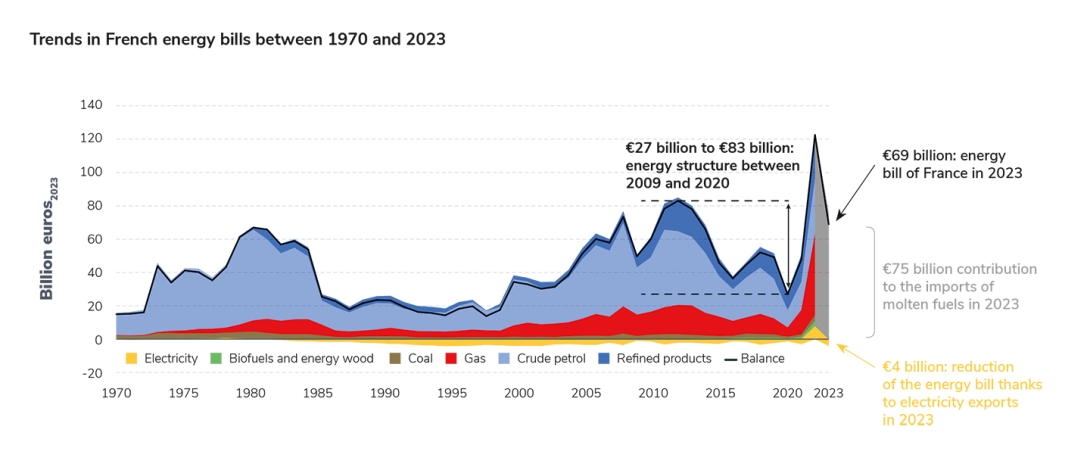

France's energy bill is the balance between the valuation of imports and that of energy exports, all energies combined (electricity and fossil fuels in particular). The reversal of the electricity exchange balance in 2023, and therefore the return to a position of being a net electricity exporter for France, contributed to reducing the energy bill by around €4 billion2023, while export balances during the period 2014-2019 contributed to a reduction of around €2 billion2023 on average. As a reminder, France's net import balance in 2022 contributed to raising the energy bill by about €8 billion in 2023. However, these orders of magnitude remain very low compared to the weight of fossil fuels in this bill, which amounted to more than €110billion in 2022 and reached €75 billion2023 in 2023: the bill related to fossil fuels is indeed the first item in France's trade deficit19.

As a result, the development of low-carbon electricity generation and the reduction of fossil fuel consumption are also an asset in terms of reducing France's energy bill and strengthening its sovereignty.

18

On this border, exchanges are organised on the scale of a set of countries, known as the Core region since 9 June, 2022. Because of this operation, it is not relevant to analyse exchanges with Germany and Belgium separately.

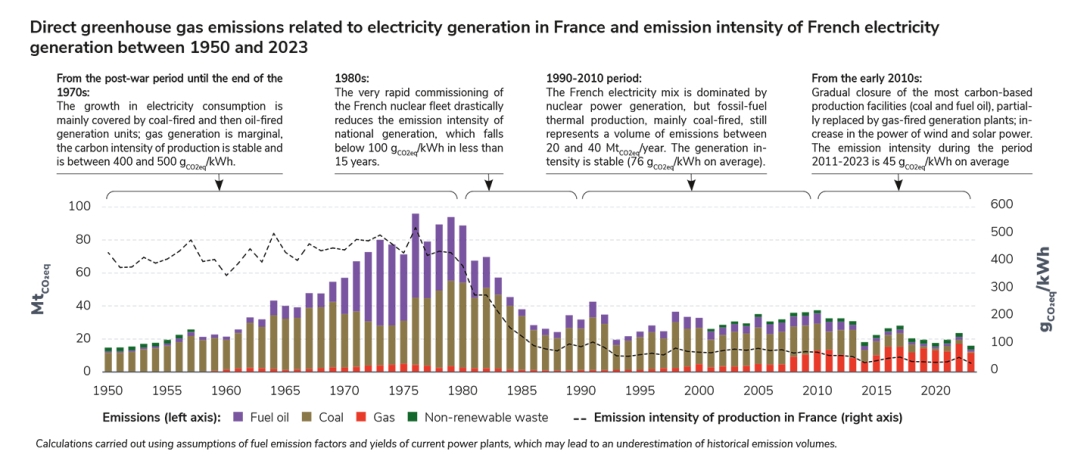

Greenhouse gas emissions from the French power system reached a historic minimum in 2023

Emissions related to electricity generation in France reached 16.1 MtCO2eq in 2023, their lowest level since the early 1950s (including when the volume of production was much lower). This very low level is the result of a relatively low volume of production by fossil-fired units in 2023 compared with pre-crisis years, and of the almost complete withdrawal of coal-fired generation. This is a 32% decrease compared to 2022 emissions (23.8 MtCO2eq). Indeed, in 2022, emissions related to production had increased slightly due to the increased use of gas-fired power generation to compensate for the lower availability of the nuclear fleet and low hydropower generation. In 2023, this particularly low volume was achieved thanks to the fall in the overall level of production, the resumption of nuclear and hydropower generation, and high renewable production, especially wind power during the autumn and winter months.

Since the early 2010s, the gradual closure of coal-fired production facilities and the increasingly insignificant use of the remaining power plants have led to a sharp decline in emissions related to this type of fuel for electricity generation. Emissions related to fuel oil also decreased. At the same time, emissions from gas-fired power plants have increased, this production having partly replaced that of other fossil fuels. These three trends combined lead to an overall decline in the volume of greenhouse gas emissions attributable to electricity generation.

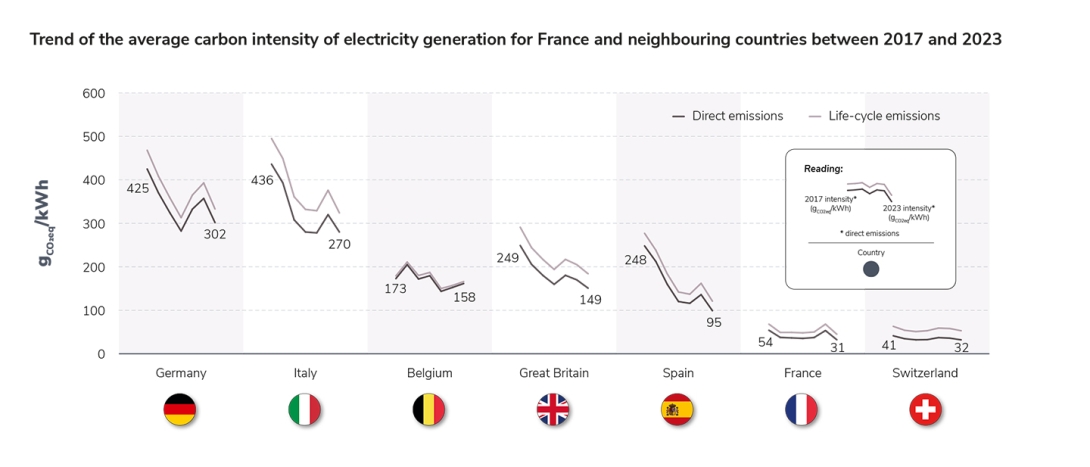

The emission intensity of French production, in 2023, remained much lower than that of most of its European neighbours, at 32 gCO2eq/kWh (against 53 gCO2eq/kWh in 2022). By way of comparison, the carbon intensity of electricity generation reached 303 gCO2eq/kWh in Germany and 270 gCO2eq/kWh in Italy. Only a few countries with the most low-carbon generation mix, especially countries with abundant hydropower generation, such as Sweden, Norway, Switzerland or Austria, have reached a carbon intensity comparable to that of France. In addition, French exports, by replacing carbon-based production, have made it possible to avoid significant volumes of emissions abroad, primarily in Italy (11.1 MtCO2eq) and Germany (5.5 MtCO2eq).

The European mix is also moving towards decarbonisation, with an emission intensity that has been declining for several years (-29% for Germany and -36% for Italy since 2017).

Even if the French electricity mix is already largely low-carbon, the challenge for the coming years lies in increasing the volume of low-carbon electricity generated to supply growing electricity needs, which will result from the gradual phasing out of fossil fuels in high-emission sectors (transport, industry, buildings).

Emissions at the perimeter of electricity consumption in France, taking into account electricity imports and exports20

with other European countries, also fell sharply, from 28.4 MtCO2eq in 2022 to 15.3 MtCO2eq in 2023. In particular, the weight of emissions related to electricity imports on this total has fallen significantly compared to 2022 (from 18% to 5%), a singular year where imports were particularly high and exports low.

Emissions from imports remained on average more carbon-intensive than those from French production, but more than 60% of French imports in 2023 were low-carbon. Indeed, they reflect a varied mix containing an increasingly large share of renewables (more than 50% of the European mix in 2023). The emission intensity of imports has also decreased, a trend that should continue with the gradual decarbonisation of the electricity mixes of European countries21.

Graphe

Legend and filters

Greenhouse gas emissions from electricity consumption in France

Last update: 05 June 2024 at 11:05

Legend and filters

>

Hide

Annual

Monthly

Direct emissions

Life cycle emissions

- Incomplete year

- Preliminary data

* contributing to consumption in France

20

Imports that supply consumption in France are included, while French exports that supply consumption abroad are deducted from the calculation.

The European power system continues to decarbonise

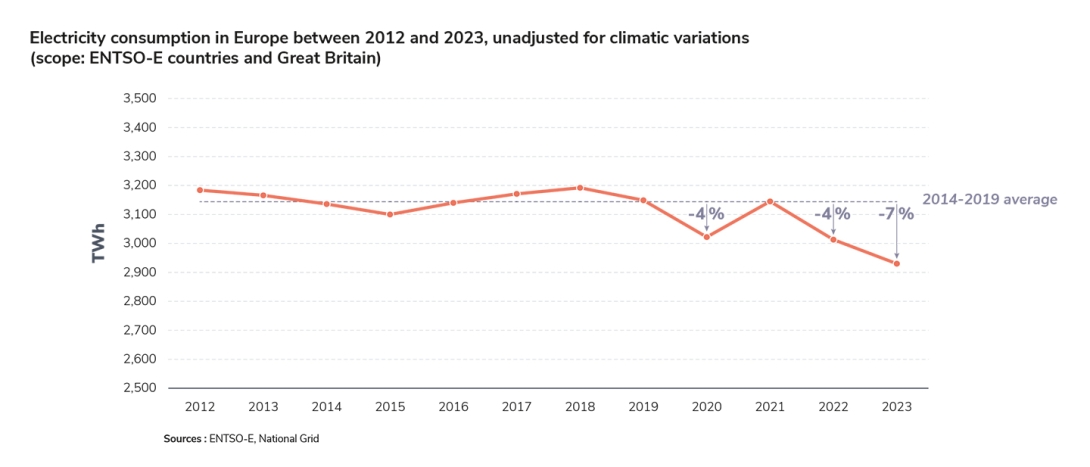

As in France, for the second consecutive year, electricity consumption in Europe22 slowed down: a 3% decrease between 2022 and 2023, which follows on from the 4% decrease already observed between 2021 and 2022.

The dynamic for the interconnected area is very similar to that observed for France: a fall in consumption from 2020 as a result of the Covid pandemic, followed by a slight recovery in 2021, before further reductions in 2022 and 2023. These are the result of the worsening energy crisis that has affected all European countries, with the increase in gas prices and its repercussions on electricity prices.

In line with the decrease in consumption, electricity generation in Europe also decreased: it was 3% lower in 2023 than in 2022, a year that was already characterised by a 3% reduction compared to the previous year. This has been more visible in the "large" generating countries. Only France has experienced an increase in its electricity generation, resulting from the better availability of its nuclear and hydropower fleets.

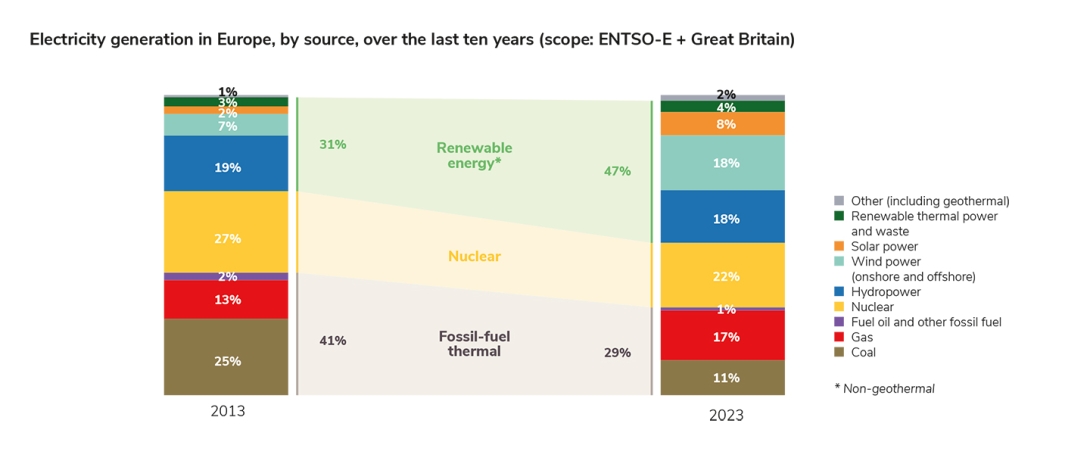

In all European countries, there has been a steady decline in the carbon intensity of electricity generation, which has been ongoing for several years, a direct result of policies to decarbonise energy mixes and in particular the growth of renewable energies. The share of fossil thermal sources, which are historically dominant in the European electricity mix, has decreased from 39% in 2013 to 29% in 2023. This trend is contrasted between the different production sources. The share of coal, a production characterised by a very high carbon intensity, is the area that shows the biggest decrease: coal still accounted for a quarter of electricity generation in Europe in 2013, and its contribution to the mix has been halved in the space of ten years, amounting to 12% in 2023. In contrast, the share of gas has increased slightly, from 14% of the mix in the early 2010s to 17% in 2023 (an increase of 23% in volume) after peaking at 20% between 2019 and 2020. Indeed, the at least partial replacement of coal-fired production by that of gas is an integral part of the decarbonisation strategy of several countries. Thus, gas remains a significant component of the European electricity mix and will remain so for several years, until the transition to a lower-carbon electricity mix materialises23.

The share of nuclear power, the leading production source in the electricity mix, has decreased slightly, from 27% in 2013 to 22% in 2023. This decrease is the result, on the one hand, of the decrease in French nuclear power generation, and on the other hand, of the closure of several reactors for reasons of age or energy policy: in France with the closure of the two Fessenheim reactors in 2020; in Germany, which made its exit from nuclear power in 2023 effective with nine reactors shut down between 2013 and 2023; in Belgium, where two reactors were shut down, although the country maintains a proportion of 45% nuclear power in its energy mix; in the United Kingdom; in Spain; in Sweden and in Switzerland.

On the other hand, the share of wind and solar energy in the mix has increased dramatically in ten years, from 9% in 2013 to 26% in 2023, due to public policies in favour of the energy transition in a large number of countries. In addition, wind power is now the second-largest source behind nuclear power and just ahead of hydropower. The United Kingdom and Germany are among the countries that have recorded the largest increase in renewables in ten years and have the most ambitious growth targets for these sources. The increase in renewable production partly offsets the decline in the historic controllable sources (nuclear and coal), while gas completes the rest of the mix.

The prospects for decarbonising the European energy mix as a whole are based on the extensive electrification of energy uses, a reduction in final energy consumption and a very pronounced development of renewable energies. With this in mind, adapting national electricity networks and interconnections is a major challenge, making it possible to provide flexibility and optimise the operation of the power system on a European scale. This will be all the more necessary as the penetration of renewable energies will continue to accelerate and generate alternating situations of north-south flows (cases of high wind power generation in the North Sea) and south-north flows (cases of high photovoltaic power generation in southern Europe). The envisaged rates of transformation of the power systems of neighbouring countries are even faster than in France.

22

ENTSO-E scope (35 countries) and Great Britain.

23

The countries of the European Union have the objective of achieving carbon neutrality by 2050, whereas the values detailed here relate to a broader scope, that of the countries belonging to ENTSO-E plus the United Kingdom.

24

The carbon intensity of electricity generation is calculated on the basis of direct emissions and the life cycle. The latter makes it possible to take into account, in addition to the direct emissions related to combustion in power plants (if applicable), all the emissions related to the fuel and infrastructure involved in enabling the production of a given amount of energy. Some generation sources, such as wind, solar and hydro power, do not cause direct emissions, but their implementation generates indirect emissions that are included in this scope.

Data updated on 29 February 2024