Paragraphes de la section

In 2022, the power system proved resilient in the face of the most serious energy crisis since the 1970s

The year 2022 saw a major energy crisis emerge, on a scale not seen since the oil shocks of the 1970s. France and Europe in fact faced three independent but simultaneous crises which compounded one another:

- Soaring gas prices, amid concerns about Europe’s security of supply in the wake of Russia’s invasion of Ukraine. Prices first surged in late 2021, as the economy was recovering from the COVID-19 crisis. They were then pushed even higher by the war in Ukraine and the resulting reduction of Russian gas supplies to Europe, at a time when the entire European continent was worried about security of supply;

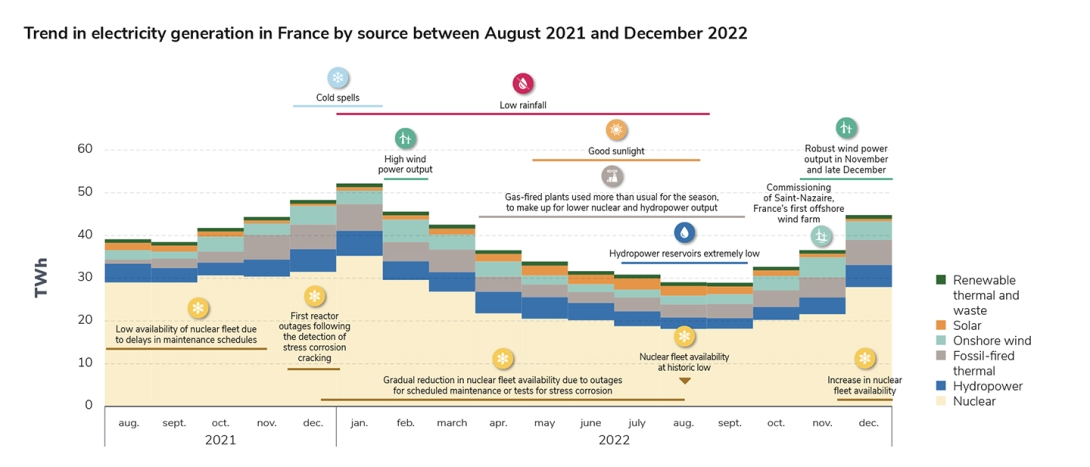

- A crisis of French nuclear power generation after the discovery of a generic fault affecting the fleet’s most recent reactors, following the discovery of a stress corrosion phenomenon, which led to the shutdown of numerous units for testing and repair starting late in 2021. This pushed yearly nuclear power output down to its lowest level on record since 1988, some 30% below the yearly average of the past 20 years;

- A lengthy drought that drove hydropower output in France down to its lowest level since 1976 and had a similar impact across much of Europe.

Against this backdrop, the power system proved resilient: France did not experience any supply disruptions. This outcome is attributable to a structural decline in power demand in France and neighbouring countries, and to the fact that gas and electricity exchanges continued to function in accordance with European market rules.

In particular, short-term markets gave the right economic signals during periods of tight supply. This was notably the case during the summer, when hydropower and nuclear output dropped sharply, and market prices rose to reflect those

economic fundamentals.

The effects of the crisis were thus essentially economic. In particular, forward markets revealed a risk premium for France, leading to unprecedented price increases for deliveries in the winter. Starting in September, the management of the crisis by public authorities, the return of a large number of nuclear reactors on the grid, unseasonably warm weather, and the observation that demand was dropping and interconnections were functioning properly, all contributed to gradually ease uncertainty.

However, the effects will continue to be felt in 2023, as many supply contracts signed in the latter

half of 2022 for 2023 and beyond were based on those high prices. As a result, there will be a delay before the downward trend in market prices that began in late 2022 is felt by consumers that do not benefit from the government’s protection schemes

(tariff shield, electricity shock absorber).

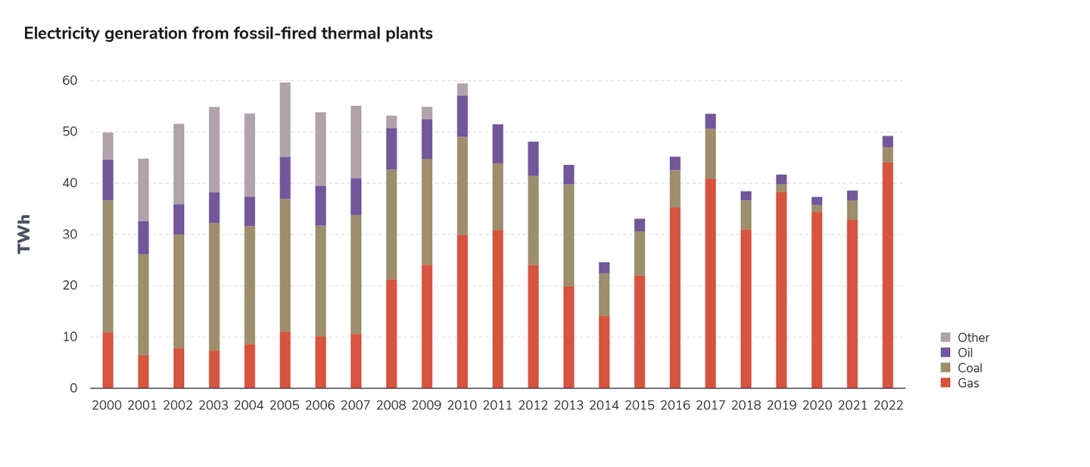

The environmental cost of the energy crisis is real, but contained. Direct emissions from electricity generation reached 25 MtCO2eq (up from 21.5 MtCO2eq in 2021). Coal-fired generation has been almost completely eliminated from the French power mix (it now accounts for just 0.6% of electricity generation in France). Gas-fired plants were dispatched more than any time in the past, though output was lower than what was feared in the event of a cold winter or if energy consumption had been maintained.

France’s emissions remain well below those of comparable countries: emissions in Germany, for instance, were some ten times higher than in France in 2022.

Even when taking into account imports from neighbouring countries, there was no significant deterioration in the carbon footprint of the power consumed in France: the carbon content of imports reflects the average content in neighbouring countries, as France imports in situations of heavy fossil-fired thermal plants use, but also when wind or solar generation is high, for instance.

With all this in mind, it should be noted that there was no pause in the energy transition in 2022. A record 5 GW of renewable capacity were added.

An acceleration remains necessary if France is to meet its targets, but, similarly to other studies published recently in Europe, the 2022 Electricity Report shows that the power system transition continues and that renewable energy sources in France are now contributing both to the structural decarbonisation of the mix and to the security of supply.

In 2023, it will be essential that the situation of the French nuclear fleet improve to make the power system more resilient to international fossil fuel risks and return the broader economy to its decarbonisation trajectory.

Consumption was down sharply from pre-crisis levels in 2022

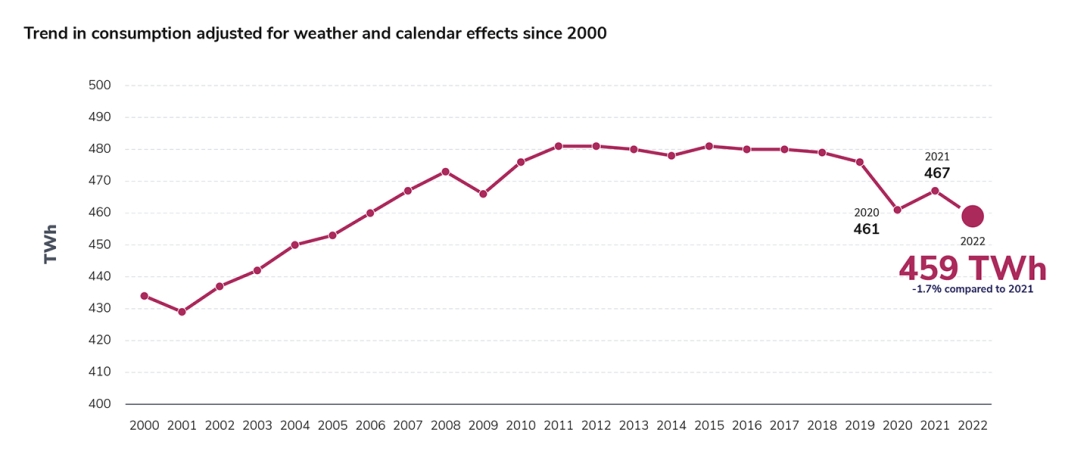

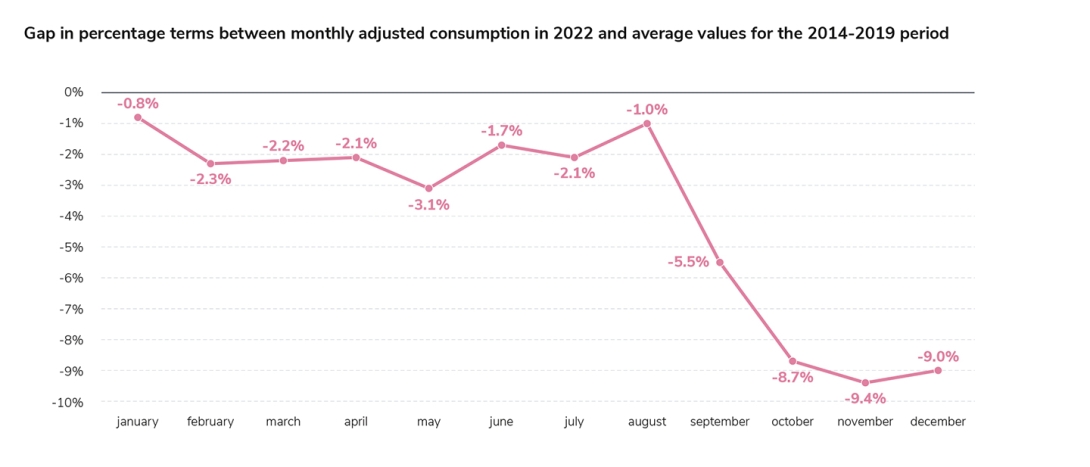

Adjusting for weather and calendar effects1, total electricity consumption was 459.3 TWh in 2022. This represented a 1.7% decrease from 2021, comparable to the drop seen in 2009 after the financial crisis. Compared to the average before the health crisis (2014-2019), consumption was down 4.2% over 2022 as a whole and by almost 9% in the last nine months of the year. The last time that electricity consumption adjusted for weather effects was lower than in 2022 was in 2005, before demand began to plateau in 2010.

Demand was also lower than in 2020 (461 TWh), a year marked by lockdowns and a drop in economic activity resulting from the COVID crisis. The decrease in demand was first observed in the industrial sector, which was more exposed to rising energy prices in the absence of protections. Energy-intensive segments like the chemical industry, metallurgy and steelmaking were hit the hardest (respectively -12%, -10% and -8% over the whole year2 and -19%, -20% and -20% between September and December), in line with the trend observed across Europe. The decrease then spread across every sector, notably the residential (which accounts for most of demand in terms of volume) and services sectors. In the last four months of the year, the average decline in consumption in the residential and service sectors exceeded 5%. It remains difficult to separate the effects of purely economic constraints from those of energy-saving actions. Indeed, despite the “electricity tariff shield” put into place for residential consumers, inflationary pressures impacted households’ overall budgets and may have incentivized energy savings, even in the absence of price hikes on residential contracts.

At the same time, the government’s successful efforts to mobilise residential and business users to reduce their consumption played a central role. The downward trend in consumption became clear from September-October onwards, when the government began issuing energy sobriety messages. Gross electricity consumption was also lower in 2022 (452.8 TWh) than in 2021 (471.5 TWh), a 4% year-on-year decrease. It declined more sharply than adjusted consumption (1.7%) because of the unseasonably warm temperatures in 2022. This notably led to a sharp drop in power demand for heating in autumn and winter, given how temperature-sensitive demand is in France.

1 These adjustments make it possible to compare years against one another and to identify structural trends that affect consumption.

2 Among large industrial users connected to the transmission grid.

Total electricity generation was at its lowest since 1992 due to limited nuclear and hydropower output

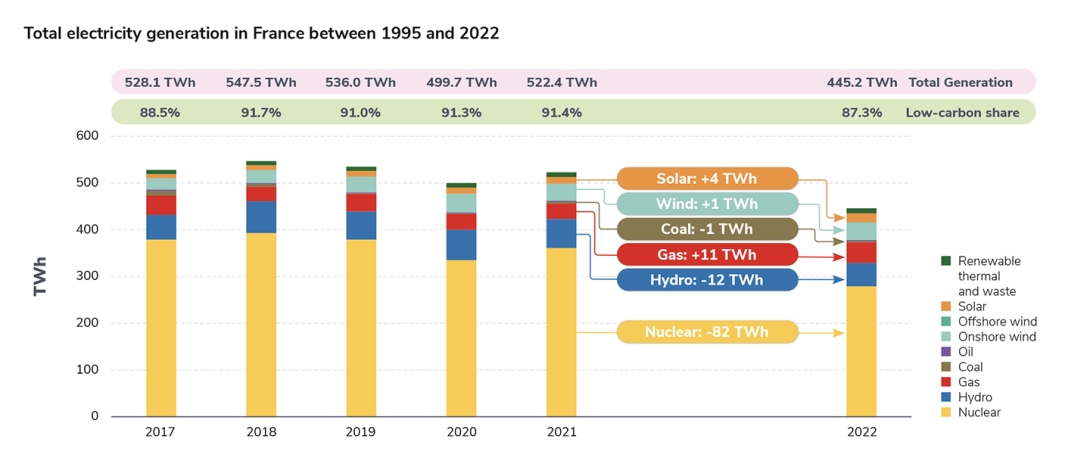

Total electricity generation in France in 2022 was 445 TWh, a 15% decline compared to 2021 (522 TWh). This was the lowest output on record since 1992, before the full commissioning of the nuclear fleet, with, at the time, several reactors still under construction3.

Output was affected by the reduced availability of the nuclear fleet, which produced 82 TWh less than in 2021, and by constraints affecting hydropower generation (-12 TWh). Declines in output from these sources were partially offset by increased generation from gas-fired plants (+11 TWh) and solar (+4 TWh).

3 Since 1992, six reactors were brought into service (Penly 2, Golfech 2, Chooz B 1, Chooz B 2, Civaux 1, Civaux 2) and two were retired (Fessenheim 1 and Fessenheim 2).

The availability of the nuclear fleet hovered at historic lows throughout the year, driving output down to the lowest level on record since 1988

The availability of France’s nuclear fleet was historically low throughout 2022, with a yearly average availability of 54% compared with an average of 73% between 2015 and 2019.

An all-time low of 21.7 GW was recorded on 28 August 2022, when nearly 65% of the fleet was offline. Availability rebounded later in the year but remained well below previous years.

The gap with prior years was particularly pronounced during the summer, which saw a concentration of unscheduled outages following

the discovery, in late-2021, of stress corrosion cracking in several reactors. These outages, or outage extensions to carry out maintenance, tests and repairs where needed, primarily involved the newest reactors in the fleet (N4 and P4’ designs),i.e. reactors that were not targeted for investment in the Grand Carénage refit programme. These additional outages added to an already busy operational

calendar made even busier by the postponements of maintenance caused by the COVID-19 crisis.

The concentration of outages in the summer did make it possible to maximise availability during the winter months.

Graphe

Legend and filters

Availability of the French nuclear fleet over the year, since 2015

Last update: 12 February 2023 at 10:00

Legend and filters

>

Hide

- Incomplete year

- Preliminary data

Informations and sources

This graph shows the daily availability of the French nuclear fleet over the last three years, compared with the 2015-2019 range.

Yet the overall low level of availability during the year drove total nuclear generation down sharply from previous years: output for the

year reached 279 TWh (62.7% of total domestic generation), compared with 360.7 TWh in 2021 and 379.5 TWh in 2019. This was the first time since the construction of the existing nuclear fleet was completed that annual output was this low, falling 30% below the average of the prior 20 years. In absolute terms, it is the lowest level on record since 1988, when installed nuclear capacity in France stood at just 51 GW, or 83% of today’s total capacity (eight fewer reactors).

The more limited availability of the French nuclear fleet was one of the main reasons actors were anticipating issues with the supply-

demand balance. RTE published security of supply analyses in September, underscoring that the period of required vigilance would exceptionally start in the autumn4. Nuclear output was at its lowest during the months of August and September (around 18 TWh

per month, compared with 29 TWh per month in August and September 2021), before gradually climbing back up to 28 TWh in December, close to what was recorded in December 2021 (32 TWh).

In the autumn, the availability of the nuclear fleet was in line with RTE forecasts. By the end of the year, reduced uncertainty about the return online of several nuclear reactors, together with a sharp decrease in demand that was confirmed at the national level in the autumn, and the observation that exchanges with neighbouring countries continued to function per European market rules, all

helped ease the strain on France’s power system.

Graphe

Legend and filters

Annual nuclear power generation

Last update: 14 February 2023 at 11:52

Legend and filters

>

Hide

Annual

Monthly

- Incomplete year

- Preliminary data

Informations and sources

This graph gives an annual and monthly overview of French nuclear power generation.

Hydropower output fell to its lowest level since 1976 due to exceptionally warm and dry weather conditions

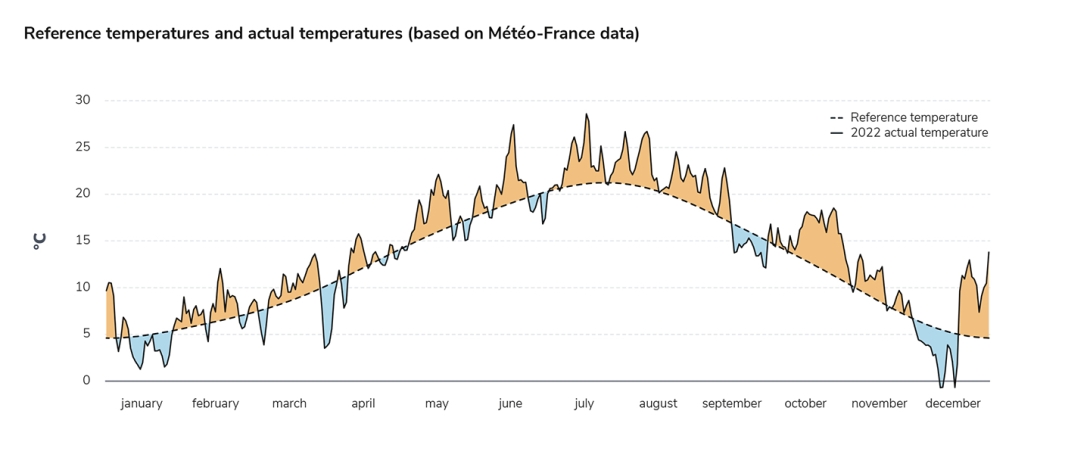

According to Météo-France’s annual climate statement, the year 2022 was the warmest year in France since the early 20th century5. Temperatures were above seasonal averages throughout most of the year: the months of May and October were the warmest since records began in 1900, and summer temperatures were the hottest since 2003.

Overall yearly rainfall was 25% below average, making 2022 the second driest year on record (behind 1989) since measurements started in 1959. The past year was also much drier than 2005, when precipitations were 20% below average.

This rainfall deficit had a significant impact on the availability of hydropower capacity, with water reserves dropping to historic lows mid-July. It took careful management of reserves by operators and favourable weather conditions in the autumn for the hydropower industry to be able to make a substantial contribution to security of supply during the winter months: starting mid-October, reserves returned to usual levels, then hovered close to the average historic range starting mid-November, notably because of reduced capacity use amid lower demand.

Graphe

Legend and filters

Trend in water reserves over the year

Last update: 14 February 2023 at 11:54

Legend and filters

>

Hide

- Incomplete year

- Preliminary data

Informations and sources

This graph shows the weekly evolution of water reserves.

With a total yearly output of 49.6 TWh, hydropower generation was 20% below the 2014-2019 average (61.6 TWh, ranging from

53 TWh in 2017 and to 67.7 TWh in 2018).

Graphe

Legend and filters

Trend in hydropower generation (1995-2022)

Last update: 14 February 2023 at 11:53

Legend and filters

>

Hide

Annual

Monthly

Global

Energy source

- Incomplete year

- Preliminary data

Informations and sources

This graph provides a monthly and annual overview of hydraulic production, broken down by sub-sector (Lake, Hydropeaking, Run-of-river, Other).

The year 2022 saw record renewable capacity additions but an acceleration remains necessary if France is to meet its targets

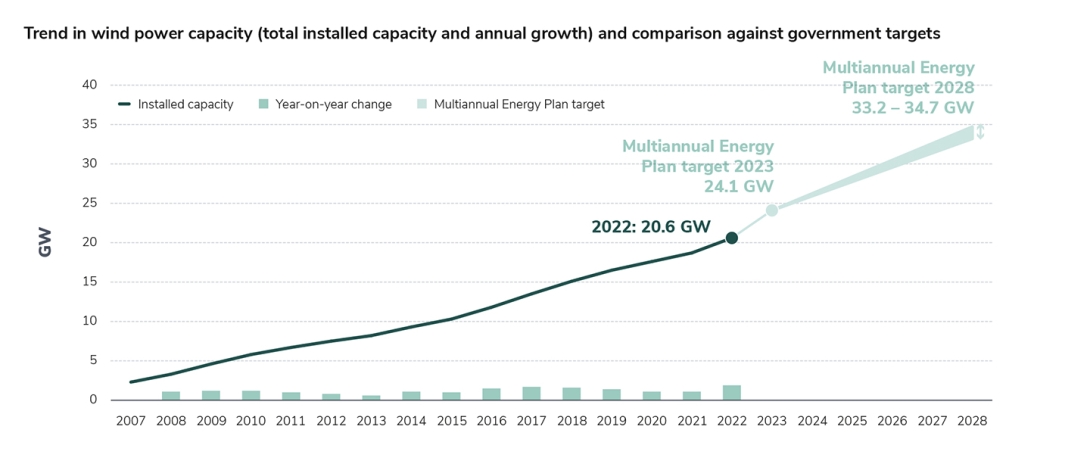

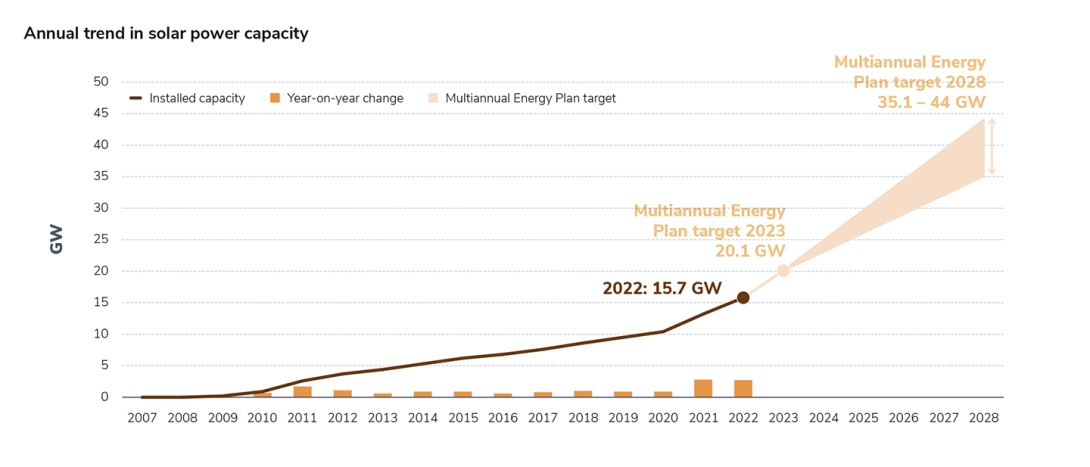

A new record was set for renewable capacity growth in 2022 with 5 GW brought into service. Onshore wind capacity expanded by 1.9 GW year-on-year, from 18.7 GW at the end of 2021 to 20.6 GW at 31st December 2022 (vs. +1.7 GW in 2017). Solar capacity growth was robust for the second year in a row, with 2.6 GW brought into service in 2022, following 2.8 GW in 2021. This expansion occurred despite tensions on supply chains and the rising cost of some components, the effects of which could materialize over the coming years. Installed solar capacity reached 15.7 GW at the end of 2022.

Another key highlight of 2022 was the commissioning of France’s first offshore wind farm off the coast of Saint-Nazaire, with a capacity of 480 MW. The farm is now fully operational and has been injecting power into the French grid sinc the summer of 2022. Offshore connections can be expected to ramp up in 2023 with the planned commissioning of the Saint-Brieuc and Fécamp farms, with a capacity of close to 500 MW each.

In terms of generation volumes, the contribution of onshore wind farms continued to increase as more capacity was added, with annual output reaching 37.5 TWh (up by just under 1 TWh relative to 2021), despite poor wind conditions. The yearly capacity factor for onshore wind was close to 21.6%, the lowest level in ten years. Total production was lower than in 2020 (39.6 TWh), a year which had seen a high capacity factor.

Solar capacity growth, combined with good sunlight conditions, drove solar power output up sharply in 2022 to 18.6 TWh (+31% year-on-year). Solar now significantly contributes to France’s electricity mix, with an output equivalent to three nuclear reactors in volume.

The pace of renewable capacity growth will need to accelerate further if France is to meet the public targets set for 2020-2030. In particular, the currently in force Multiannual Energy Plan (Programmation Pluriannuelle de l’Énergie) mandates that installed onshore wind capacity should reach 24.1 GW by the end of 2023 (meaning 3.5 GW remain to be installed) with solar capacity reaching 20.1 GW by that time (4.4 GW remaining to be installed).

Thermal power generation was higher than in 2021, but not as much as had been feared

In 2022, gas-fired plants were dispatched to unprecedented levels, though output was below the projections for a cold winter scenario

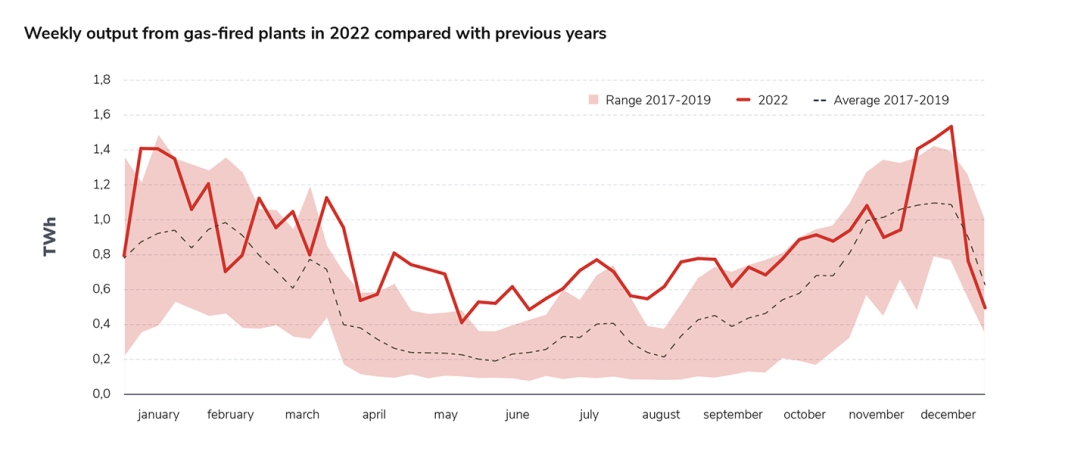

or if energy consumption had been maintained. With yearly output reaching 44.1 TWh (up from 32.9 TWh in 2021), gas once again became the third largest electricity generation source in France, behind nuclear and hydropower, edging out wind, which had held that rank the two previous years.

It was in the spring and summer of 2022, when hydropower and nuclear generation were low, that the use of gas-fired plants most exceeded historic levels. During the winter, on the contrary, it was close to usual levels.

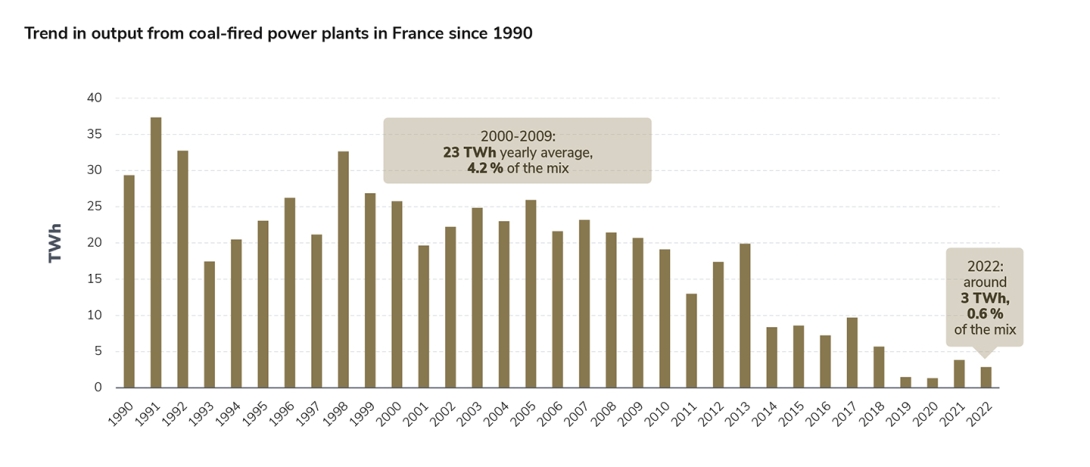

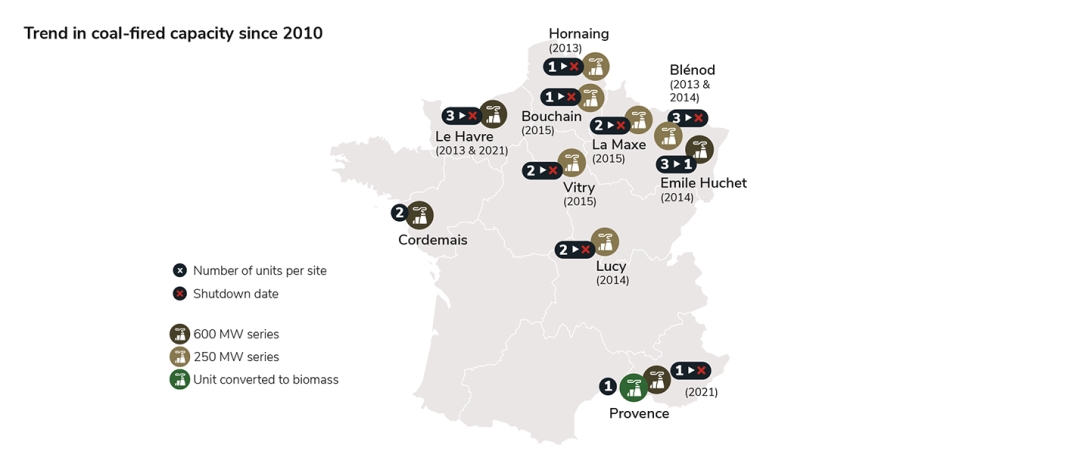

Even amid an overall tight power supply context, coal now makes up an extremely small share of French power generation. Coal-fired plants accounted for only 0.6% of total output in 2022 (about 3 TWh), a decrease from 2021 (about 4 TWh) and well below historic levels. These plants generated around 12 TWh per year on average (2.2% of the mix) between 2010 and 2018, and 23 TWh per year between 2000 and 2009 (4.2% of the mix). With only two plants still in operation at the end of 2022, France’s coal phase-out is almost complete.

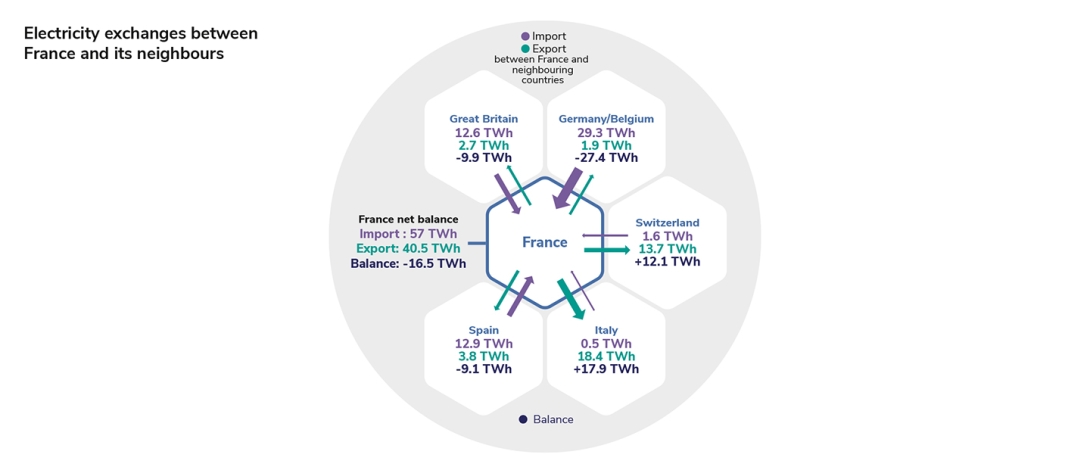

France was a net importer of electricity for the first time since 1980

In 2022, for the first time since 1980, France was a net importer of electricity, with a yearly net import balance of 16.5 TWh, or just under 4% of total domestic consumption6.

The net import balance particularly deepened during the summer, a period during which France usually exports much more than it imports: the months of July, August and September alone accounted for 60% of the net import balance, i.e. 10 TWh. This was the direct result of nuclear fleet availability falling to a historic low, combined with the drop in hydropower output (due to the drought that hit Europe in the spring and the summer) during the period.

Graphe

Legend and filters

Electricity exchange balance between France and its neighbours in 2022

Last update: 12 February 2023 at 10:20

Legend and filters

>

Hide

Annual

Monthly

- Incomplete year

- Preliminary data

Informations and sources

This graph shows imports into France, exports from France and the export balance of trade between France and its neighbors.

The fact that France imports power during periods of tight supply in winter is not unusual, and is explained by the high temperature-sensitivity of the country’s electricity demand. In 2022, this tendency was accentuated by the decrease in domestic power generation. That being said, France was able to export its production (particularly nuclear and renewable) during less tight periods, for instance in February and in the latter half of December.

Imports also allow to benefit from periods when generation in neighbouring countries comes primarily from renewable – and therefore cheap – sources. In the end, France was dependent on imports for security of supply during only a small proportion of the time, even though it was a net importer almost 70% of the time in 2022.

Over 2022, France was a net importer at its border with Germany and Belgium (with a total net import balance of 27 TWh), which was already the case in 2021 (10 TWh)7. It remained a net exporter to Italy and Switzerland (18 and 12 TWh, respectively), but became a net importer from Great Britain (10 TWh) and Spain (9 TWh). The reversal at the Spanish border is explained not only by the decrease in the availability of the French fleet but also by the introduction of a new mechanism in Iberia capping the price of gas used for electricity

generation, which resulted in lower electricity prices there than in other European countries. Therefore, within the limits of available interconnector capacity, electricity generated in Spain was cheaper than in neighbouring countries, and was dispatched in priority before plants with higher operating costs in France or elsewhere in Europe.

6 As a comparison, this is close to the average annual output of the Belleville nuclear power plant (2 x 1,310 MW, P’4 design)

7 It should be recalled that France may be importing at one border and exporting at another at the same time, a situation referred to as “transit flows”..

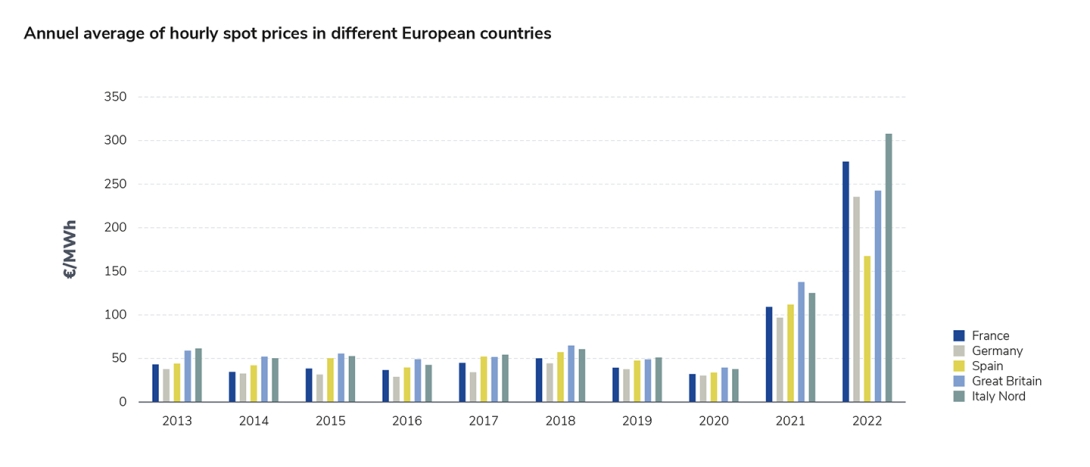

The European energy crisis caused an unprecedented rise in prices on wholesale gas and electricity markets

The year 2022 saw an unprecedented increase in gas prices, fuelled by concerns about supply to Europe in the wake of Russia’s war on Ukraine.

Prices for gas and other fossil fuels first surged in the second half of 2021 as the economy was rebounding from the COVID-19 crisis, causing tensions between supply and demand across the globe. After a short reflux in early 2022, tensions were amplified by the conflict in Ukraine and the resulting reduction in deliveries of Russian gas, amid worries about Europe’s security of supply.

Consequently, electricity prices surged in France, both for deliveries in the very short term (spot prices) and on longer time horizons (forward prices).

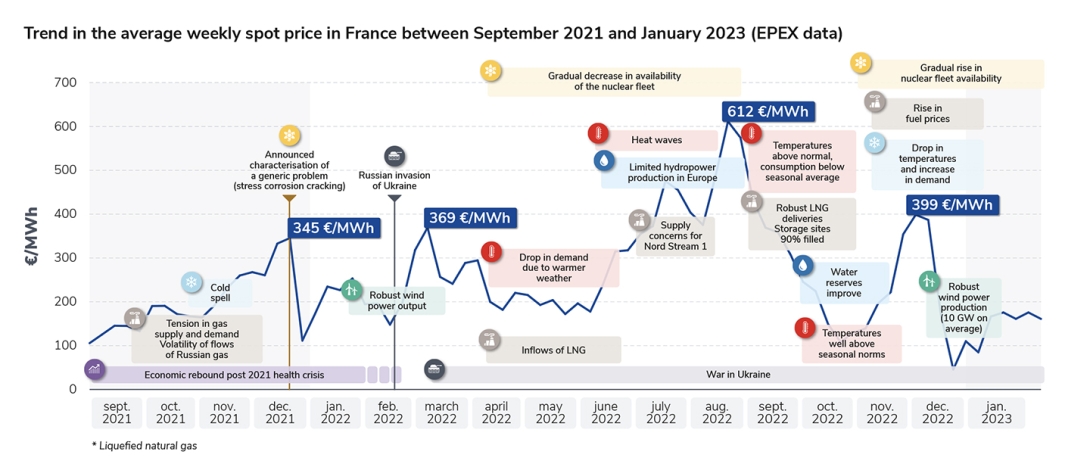

- Spot prices moved in line with the economic fundamentals of the market, reflecting changes in fossil fuel prices and the availability of low-carbon generation capacity. New records were set during the summer (the average spot price during the week of the 22nd of August was 612 €/MWh), when nuclear and hydropower output were at their lowest. From September on, prices eased, but remained higher than in previous years.

- Prices on forward markets in the summer of 2022 for deliveries in the winter of 2022-2023 revealed the existence of a specific risk premium for France that was not consistent with economic fundamentals.The premium was the result of excessive hedging by market actors relative to the supply risks suggested in risk analyses, even considering scenarios that were intentionally very pessimistic and factored in all the most adverse possible events. The risk premium collapsed towards the end of the year as concerns about security of supply began to ease (with the return into service of many reactors in December, a structural decline in consumption and warm weather).

The high market prices recorded in 2022 continue to put considerable strain on public finances and on consumers, since they formed the basis for many of the tariffs that will apply in 2023. A better correlation between costs and prices is essential if consumers are to benefit in a sustainable way, through their electricity supply, from the economic benefits of a national energy mix that is very low-carbon and competitive. In particular, this is essential in order to reverse the current climate trends, make concrete the decarbonisation via the

electrification, where possible, of end-uses that are primarily powered by fossil fuels today, or to support the onshoring of industrial activities.

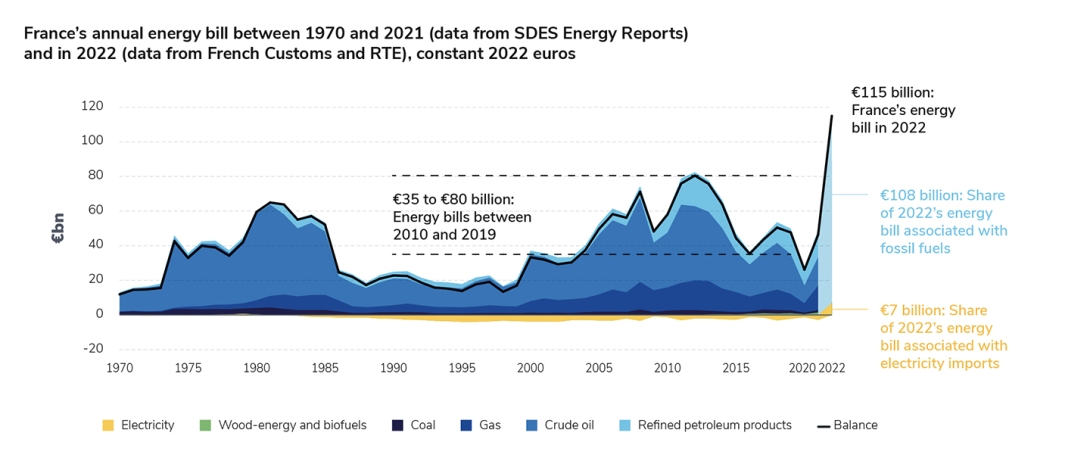

A higher energy bill took a toll on France’s trade deficit, mainly due to fossil fuel energies

France’s energy bill reached €115 billion in 2022, about €70 billion higher than in 20218. The main driver of this increase was fossil fuels, for which France paid some €60 billion more than in 2021. This was the result of higher fossil fuel prices as well as greater use of liquefied natural gas, imports of which surged after Russia invaded Ukraine9. Electricity imports added around €7 billion to France’s energy bill in 2022, whereas exports had generated a profit of close to €3 billion in 2021 (and €2 billion on average between 2014 and

2019).

Emissions from electricity generation rose but not excessively, and remained among the lowest in Europe

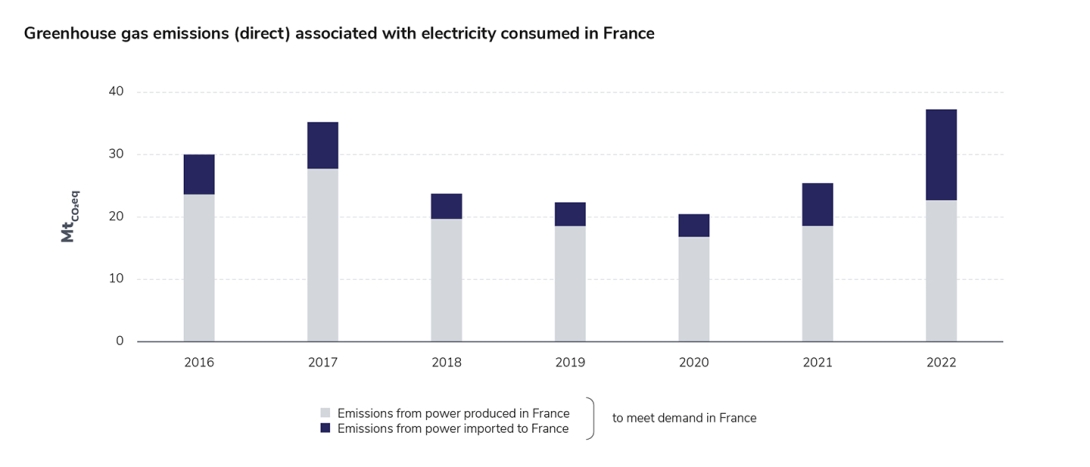

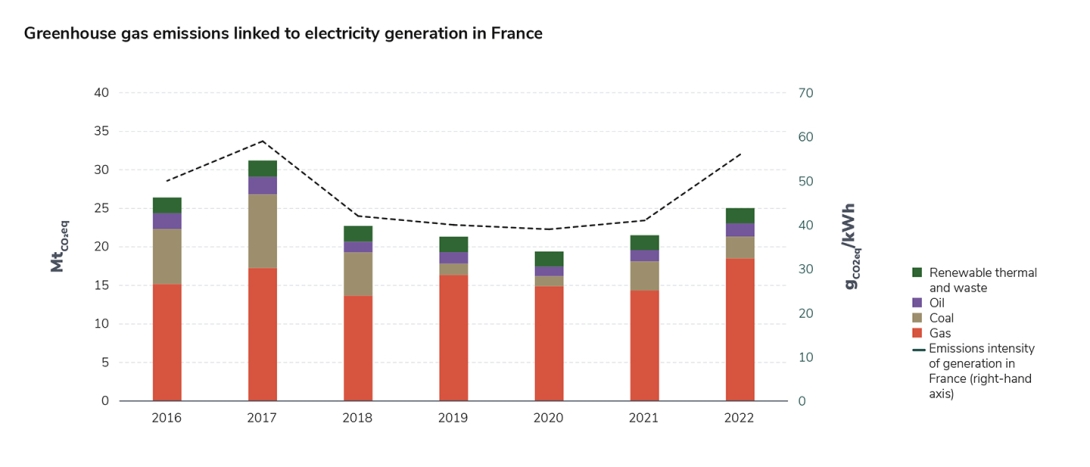

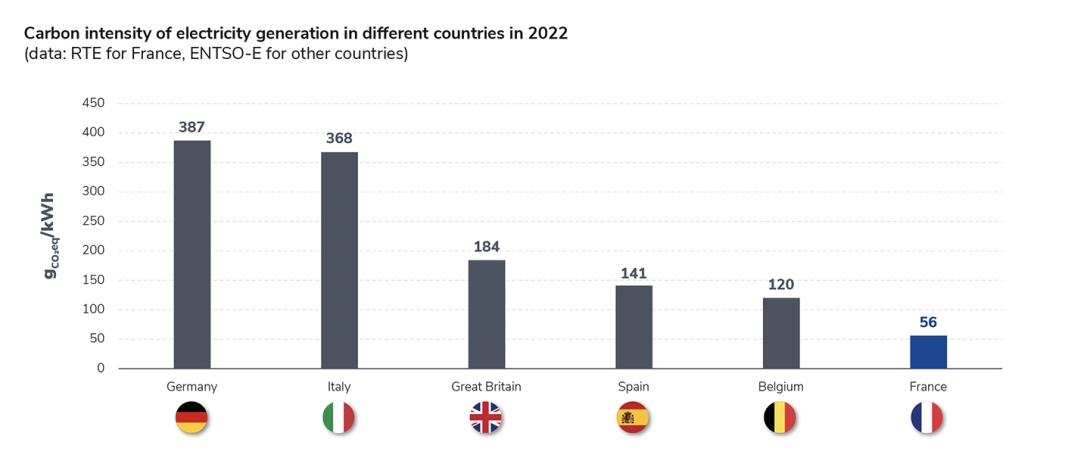

Greenhouse gas emissions from domestic electricity generation reached 25 MtCO2eq in 2022, up from 21.5 MtCO2eq in 2021. This increase reflected heavier use of gas-fired plants during the year. Conversely, emissions from coal-fired plants decreased year-on-year, as output was low. Total emissions from generation were below 2016 and 2017 levels and remained much lower than in comparable countries. For instance, in 2022, emissions from electricity generation were about ten times higher in Germany than in France.

The carbon content of the power consumed in France remains among the lowest in Europe, even when taking electricity imports into account. Though consumption-based emissions were higher in 2022 than in 2021, reaching 37 MtCO2eq, they remained comparable to other years, like 2017. The power imported reflects generation mixes in neighbouring countries, with growing shares of renewable energy.

Lastly, the decrease in low-carbon electricity habitually exported by France had to be offset by the generation mixes of neighbouring countries, where greenhouse gas emissions are higher; this had an impact of around 7 MtCO2eq on their emissions.