Paragraphes de la section

Electricity consumption remained stable in 2025, at a lower level than pre-crisis

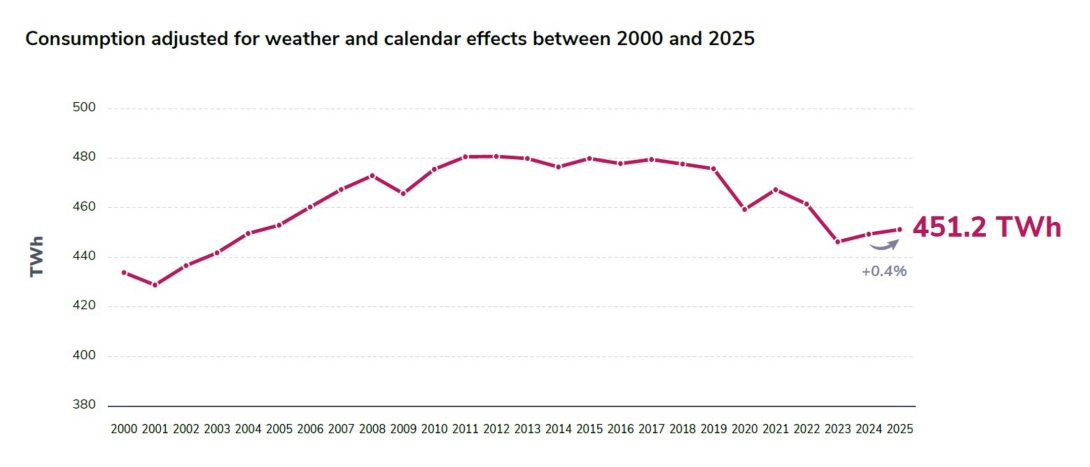

Electricity consumption in mainland France in 2025 (adjusted for weather and calendar effects) remained stable in comparison with the previous year, reaching 451 TWh (+0.4% compared with 2024).

Following the energy crisis, which led to significant falls in electricity consumption in 2022–2023, the downward trend came to a halt in 2024. Since then, however, there has been no recovery in consumption to match what occurred after the financial crisis in 2008–2009 or the pandemic in 2020.

Consumption in 2025 thus remained around 6% below the level seen over the 2014–2019 period (before the pandemic and the energy crisis). The continuing repercussions of the energy crisis and the uncertain geopolitical context, particularly with regard to industrial activity, as well as progress in energy efficiency, are tending to offset the low level of electrification of energy use.

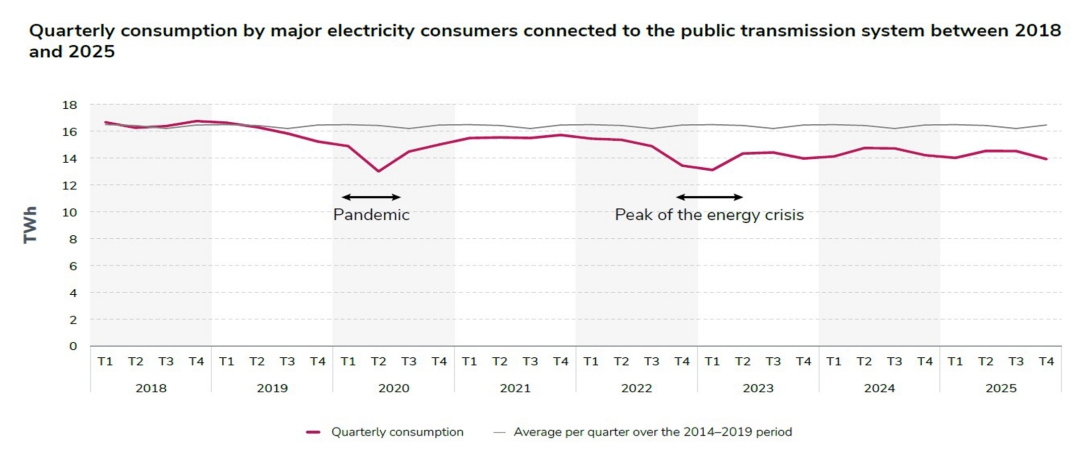

In particular, consumption by major consumers connected to the public transmission system, most of which are in the industrial sector, fell by 1.7% in 2025 (having shown a recovery in 2024) as a result of the macroeconomic context, which was marked by strong geopolitical uncertainty and increased international competition. The fall in 2025 was largely due to the chemical industry. Consumption by these major consumers remained 13% lower than in the pre-crisis period (2014–2019).

The electrification of energy use, which should follow from the decarbonisation of the French economy and from the country’s reindustrialisation, appears to be lagging behind the projected pathway to achieving France’s climate objectives.. Electricity use as a proportion of final energy consumption has remained stable overall for many years, a sign that the switch from fossil fuels to low-carbon energy, and electricity in particular, has not yet found its momentum. While the development of electric vehicles and heat pumps is continuing, the rate of change in energy use remains lower than the speed required to achieve the Fit for 55 targets by 2030.

At the same time, a number of electrification projects in industry have secured grid access for the coming years, but these are currently slow to materialise (see Electrification chapter).

Electricity consumption by data centres on "dedicated sites" connected to the public electricity transmission network has continued to rise, though the volume remains relatively low compared with total French consumption. It reached almost 1 TWh in 2025, compared with 0.8 TWh in 2024 (3 TWh on the Enedis public distribution network in 2024).

Gross French electricity consumption also remained relatively stable in 2025, at 446.2 TWh.

Despite this stagnation in consumption, peak consumption in 2025 reached its highest level since 2021, at 88 GW.

The ambition of reducing fossil fuel imports is now supported by a number of electrification projects that have already secured access to the grid for the coming years

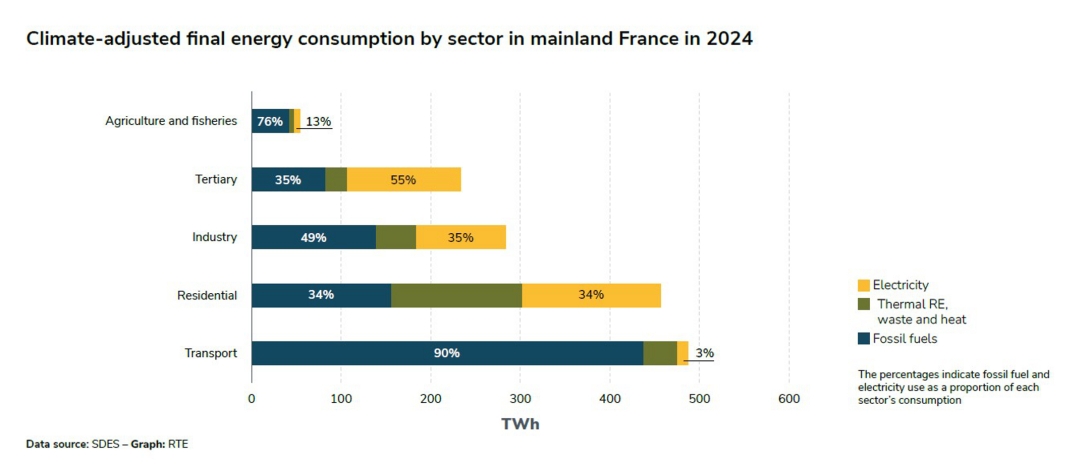

Fossil fuels continue to dominate the French energy mix. They represented almost 56% of the country’s final energy consumption in 2024, while electricity accounted for only around 27%1. This high level of fossil fuel consumption is responsible for most of the country’s greenhouse gas emissions.

Only a small proportion of French emissions (less than 3%) is linked to electricity generation, since this is largely carbon free, unlike in other countries. The main challenge in reducing France’s emissions thus lies in decarbonising other energy uses, with the electrification of fossil uses the main source of leverage.

Transport

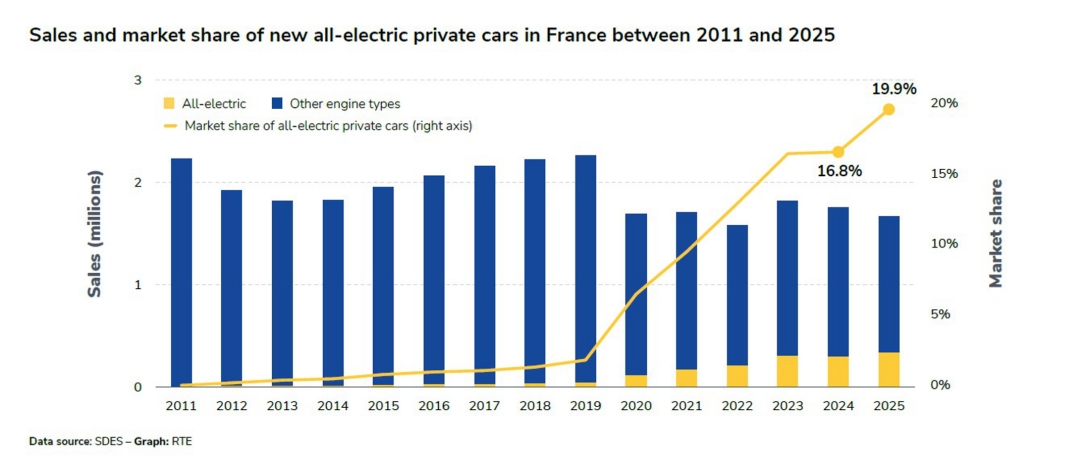

Dependence on fossil fuels is particularly high in the transport sector, where they account for 90% of energy consumption. Transport is also the sector with the highest energy consumption. Electrification is one of the ways in which fossil fuels can be effectively replaced in transport, and particularly road transport. The market share of new all-electric cars began to rise again in 2025 to almost 20%, after a year of stability in 2024.

Buildings

Around a third of the energy consumed in the residential and tertiary sectors still comes from fossil fuels. The biggest category of energy consumption and emissions is heating: despite a higher rate of electrification than in other countries, fossil fuels still account for 43% of energy consumption in residential heating and 68% of energy consumption for heating in tertiary buildings. Electrification of the housing stock is currently being driven primarily by the growth of heat pumps, particularly in new homes. Still very underdeveloped in the early 2000s, consumption by heat pumps exceeded 10 TWh2 in 2023, representing just under 3% of energy consumption in residential buildings.

Major industrial and digital projects

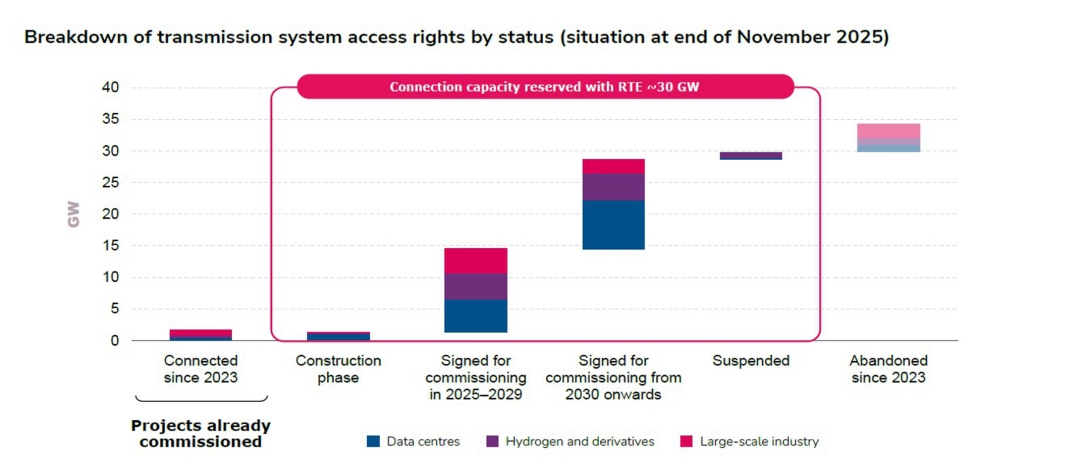

As highlighted in the 2025 Generation Adequacy Report, over 170 major industrial and digital projects are currently under development to help decarbonise existing industrial sites and contribute to reindustrialisation and digital sovereignty.

At the end of November 2025, around 30 GW of access rights to the electricity transmission network had already been allocated, including 14 GW for data centres, 9.5 GW for hydrogen production units and 6.5 GW for electrification projects at existing or new industrial sites. Around half of this 30 GW figure involves projects scheduled to come on stream between 2025 and 2029, which should lead to an increase in consumption in the coming years, though this is difficult to estimate accurately because of uncertainty about the speed with which projects will be completed and scaled up.

France’s abundant generation of competitive low-carbon electricity is now an asset that can strengthen France’s energy sovereignty and reduce the burden of fossil fuel imports on the balance of trade by developing these new energy uses. Speeding up the implementation of this type of project is now essential.

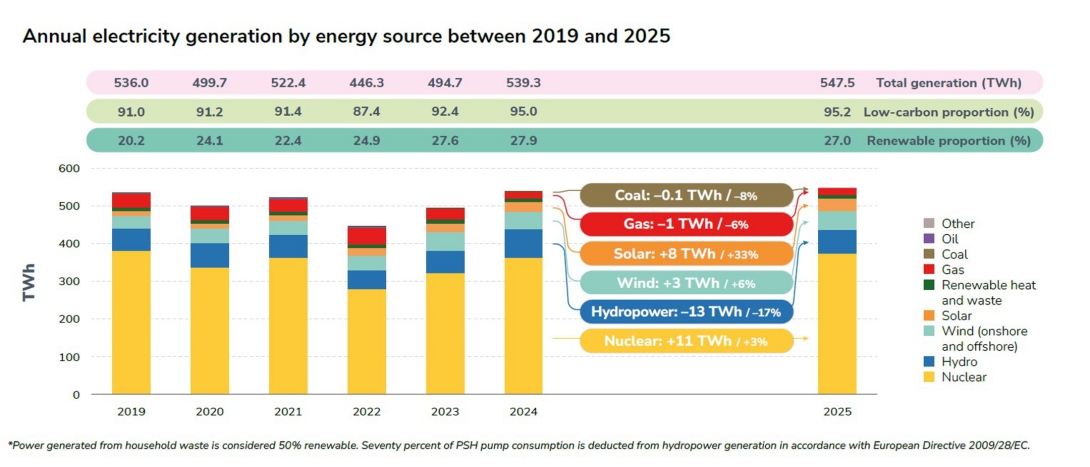

Total electricity generation in France increased slightly in 2025, with the low-carbon proportion remaining at over 95%

Electricity generation in mainland France reached 547.5 TWh in 2025. After two years of strong growth in 2023 and 2024, due mainly to the renewed availability of the nuclear fleet and improved hydropower output resulting from more favourable weather conditions, the volume of electricity generated in mainland France grew very slightly in 2025 (+8.2 TWh, or +1.5% compared with the 2024 level). This stability is the result of varying trends across the generation mix:

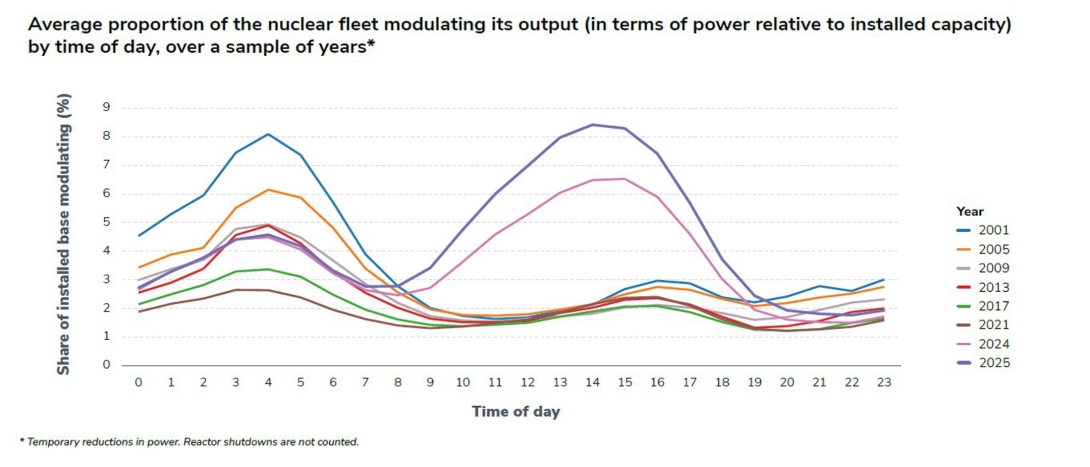

- Nuclear generation increased (373.0 TWh, +11.3 TWh compared with 2024) to a level close to where it was in 2019, thanks to improved availability of the generating fleet. The reactors’ output profile is changing, with more downward modulation in the middle of the day in summer and spring, whereas historically it was more likely to occur at night or at weekends.

- Hydropower generation fell sharply compared with 2024 (–12.9 TWh), when it benefited from exceptional rainfall, but remained at a level in line with historical averages in 2025 (62.4 TWh).

- Solar (+8.1 TWh) and wind (+2.8 TWh) power continued to increase, primarily as a result of growth in the solar and offshore wind fleet, together with improved sunshine conditions in 2025.

- Fossil-fired generation continued its decline in 2025 (–1.3 TWh compared with 2024). Generation from this source was at its lowest level for almost 75 years.

The volume of low-carbon (nuclear and renewable) electricity generated in France reached an all-time high of 521.1 TWh in 2025. This represents 95.2% of the electricity generated in mainland France, a similar proportion to 2024. The greenhouse gas emissions intensity of French electricity generation (19.6 gCO2eq/kWh) remained one of the lowest in the world (see Emissions section).

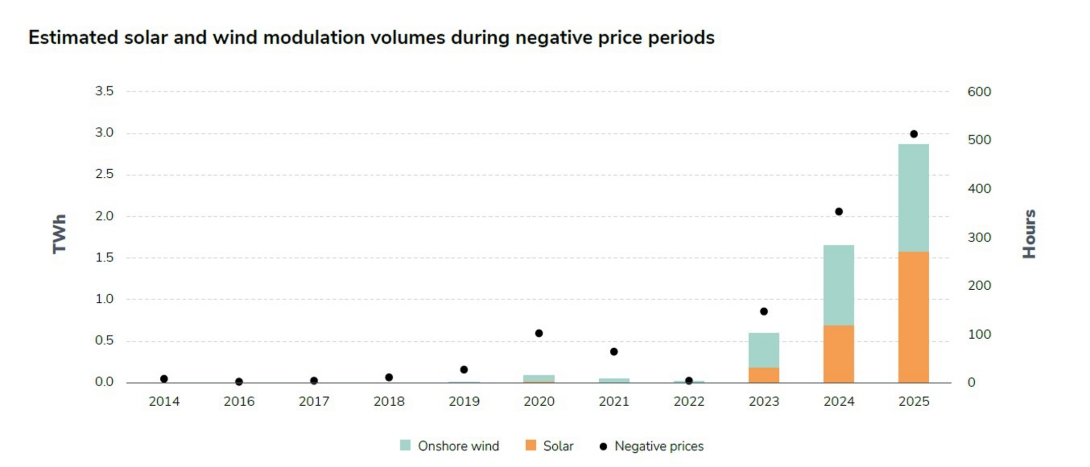

The modulation of solar and wind farms during periods of negative spot prices doubled by volume in 2025 compared with the previous year, reaching around 3 TWh, including 1.3 TWh of onshore wind power and 1.6 TWh of solar power. As a result of regulatory changes, solar and wind capacity contributed more to the real-time balancing of the power system in 2025. The modulation of renewable output contributes to the balance of the power system, but this must now be controlled in order to ensure the balance between supply and demand is managed safely in as nearreal-time as possible.

France’s electricity generation fleet continues to expand, with strong growth in solar capacity and the commissioning of a new offshore wind farm

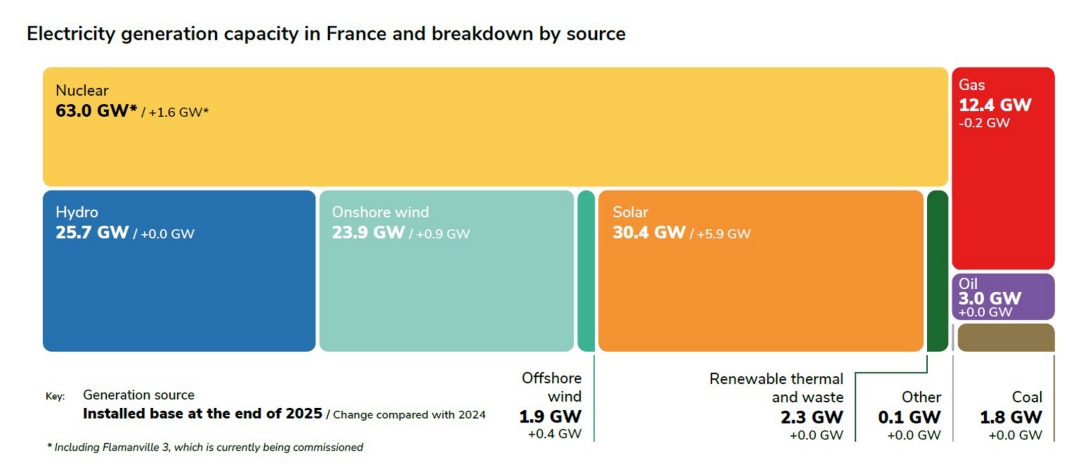

The electricity generating fleet in mainland France reached 164.5 GW at the end of 2025 (across the generation mix). This capacity includes the Flamanville 3 nuclear reactor (1.6 GW), connected to the grid in December 2024, which has gradually been commissioned over the course of 2025 and early 2026.

The increase in French electricity generation capacity in 2025 was driven primarily by solar photovoltaic capacity, which continued to grow at a high rate (+5.9 GW). Installed solar capacity (30.4 GW at the end of the year) overtook French hydroelectric capacity (25.7 GW) in 2025.

The development of French wind capacity also continued in 2025, boosted by the commissioning of the Yeu-Noirmoutier offshore wind farm (+0.4 GW) and growth in onshore wind capacity (+0.9 GW), though the growth rate here slowed for the third year running.

The fossil-fired fleet fell slightly (–0.2 GW), mainly due to closures of small cogeneration plants.

As highlighted in the 2025 Generation Adequacy Report, the evolution of the generating fleet and the sluggishness of electricity consumption mean that the challenges in the operation of the power system are now increasingly concentrated in periods that combine high generation, especially renewable, with low consumption. This new situation requires the ability to accurately control the generation system across the production mix. Over the course of 2025, the degree of flexibility offered by French solar and wind farms increased significantly:

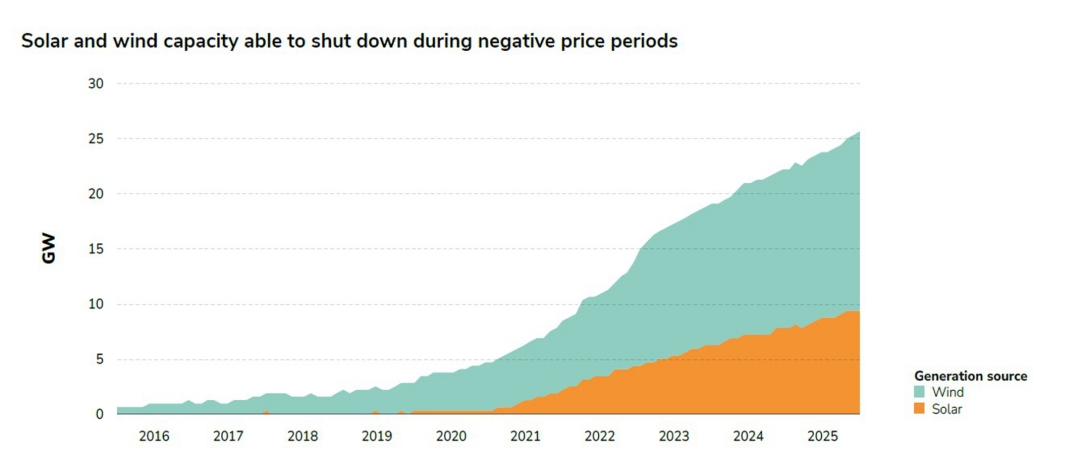

- The capacity of solar and wind installations able to modulate their output based on price signals increased by around 3 GW compared with 2024 (+1.6 GW for solar and +1.7 GW for wind), since the majority of onshore wind capacity and the largest solar farms installed in 2025 benefit from the premium scheme (“complément de rémunération”), which provides an economic incentive to modulate production when market prices are negative. While this flexibility contributes to the balance of the system, its implementation must be controlled to avoid too-sudden variations in the power generated when the price falls below zero.

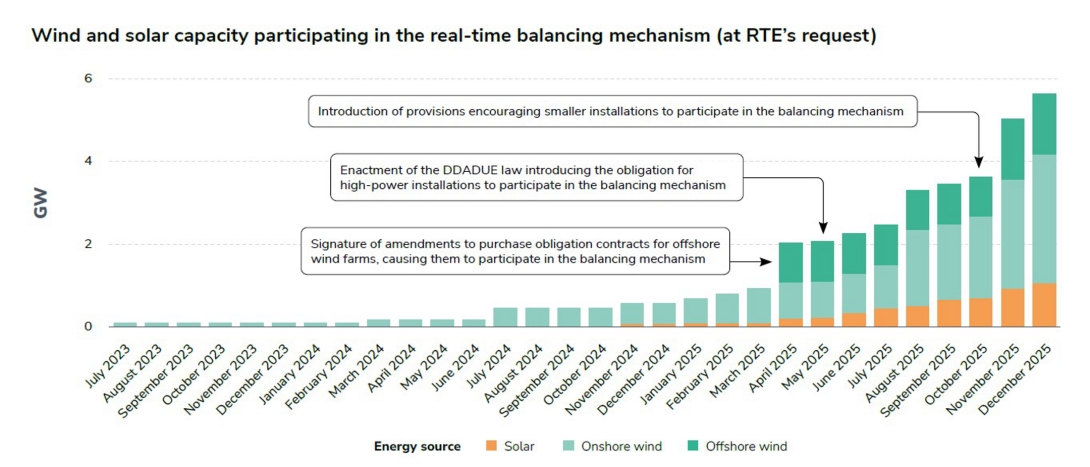

- Wind and solar capacity participating in the balancing mechanism increased almost tenfold over the last twelve months, reaching 5.6 GW by the end of 2025. This increase is the result of successive changes in the legal and regulatory framework during the year.

Spot electricity prices remained relatively stable in 2025, while futures prices fell and are now much lower in France than in most neighbouring countries

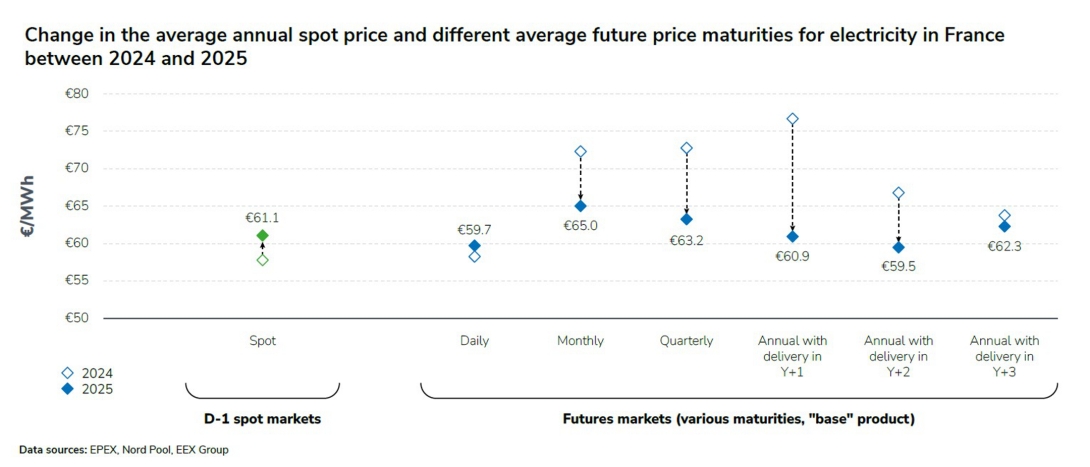

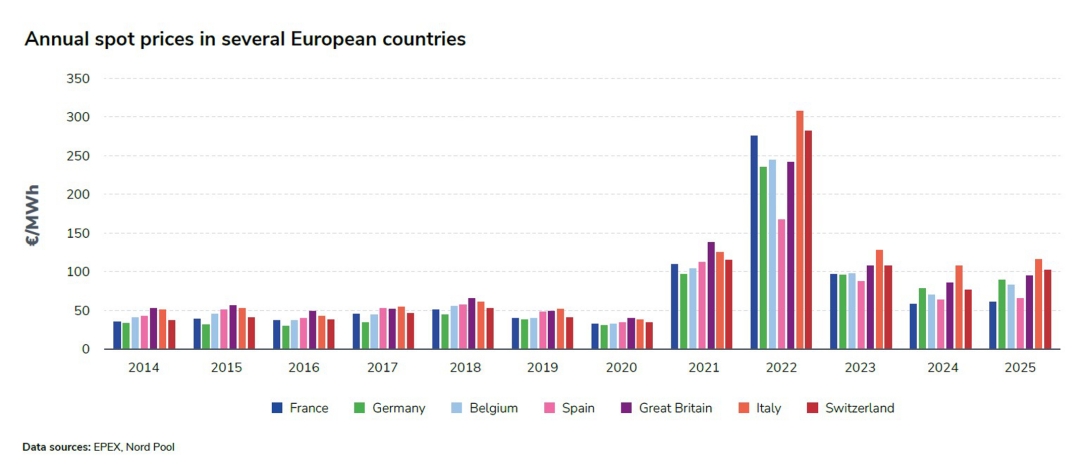

After two consecutive years of decline, the average annual spot price of electricity in France remained relatively stable in 2025 compared with the previous year, reaching €61/MWh compared with €58/MWh in 2024. This level is higher than the prices seen before 2020 (for example, the price was €43.1/MWh on average over the period 2010–2019 and €39.4/MWh in 2019), but is still much lower than the prices reached between 2021 and 2023, at the height of the energy crisis (€275.9/MWh on average in 2022).

In addition, spot prices have been increasingly volatile in recent years, which is reflected in the distortion of the average hourly price curve. On one hand, the morning and evening price peaks are now higher – mainly as a result of the higher price of gas (used by the power plants called on during peak periods) compared with the pre-pandemic period; on the other hand, the mid-day plateau has become a trough, as a result of lower consumption levels combined with the growth of solar generation in France and Europe.

This distortion is reflected in the number of hours of negative prices (513 in 2025 compared with 352 in 2024) but also in the number of hours of high prices: 1,807 hours reached or exceeded the €100/MWh level in 2025, compared with 1,382 in 2024.

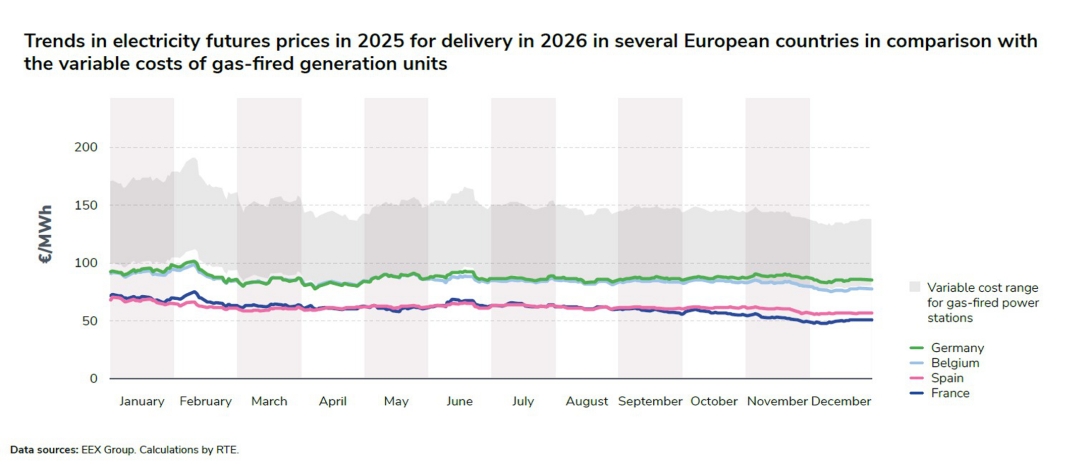

Though significant, the volume traded on the spot market (153 TWh in 2025) represents only part of the electricity traded on the wholesale markets. By way of comparison, the volumes traded on French futures markets in 2025, all maturities combined, exceeded 1,530 TWh, including over 1,300 TWh for total monthly, quarterly and annual products for delivery over the following two years.

In 2025, electricity futures prices continued the fall that began in the summer of 2023, and are now close to spot prices. As a result, the future price of the annual calendar product for delivery the following year (Y+1) fell from €77/MWh in 2024 to €61/MWh in 2025, reflecting changes in market fundamentals (lower gas prices on futures markets compared with the previous year, upward reassessment of projections for nuclear production, stable consumption due to the delay in electrification). Average futures prices remain below the projected variable cost envelope for gas-fired power stations, a sign that players are anticipating spot prices that are often set by low-carbon generation facilities.

As a result, French prices have largely decoupled from those in all the neighbouring countries, with particularly wide spreads with German or Italian prices. For the second year running, the French price also remained lower than the Spanish price. The same applies to annual futures prices (Y+1 delivery), where the French price has been below the Spanish price since September 2025. Overall, the competitiveness of the French electricity mix reflects the abundance of low-carbon production at low variable cost in France and offers a considerable advantage in terms of decarbonising the economy and catering for new energy uses.

The competitiveness of French generation led to a new export record in 2025, in line with the previous year

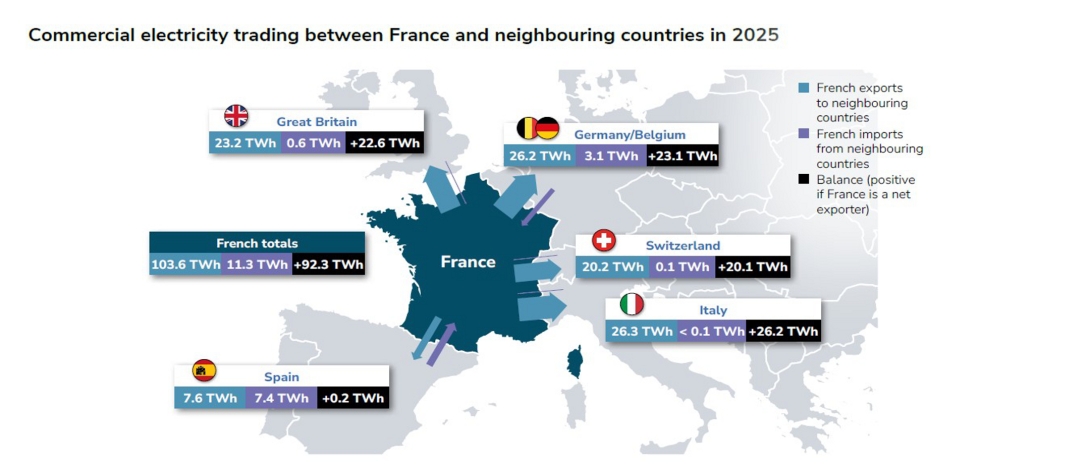

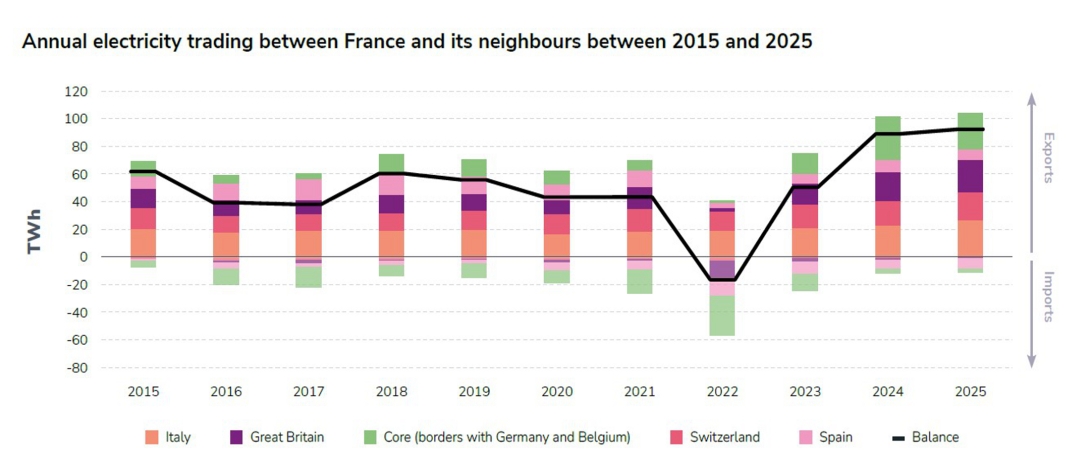

France’s net balance in 2025 was 92.3 TWh of exports. For the second consecutive year, it was the highest in its history, exceeding the 2024 balance (89 TWh). This is a significant volume, comparable to the annual electricity consumption of a country such as Belgium. France remained Europe’s leading net exporter of electricity by volume, exporting the equivalent of 17% of its output in 2025, similar to the 2024 level (16.5%).

The balance of trade was strongly positive across all borders, with the exception of Spain, where trade was more equal: it amounted to 22.6 TWh with Great Britain, 20.1 TWh with Switzerland, 26.2 TWh with Italy, 23.1 TWh with the Core region, i.e. the borders with Germany and Belgium, and 0.2 TWh with Spain.

This export volume reflects fundamentals that have changed little since 2024. National electricity generation remained high in 2025, and essentially comprised a highly competitive (low-variable-cost), low-carbon production base.

In addition, consumption remained stable compared with 2024, and is still below pre-crisis levels.

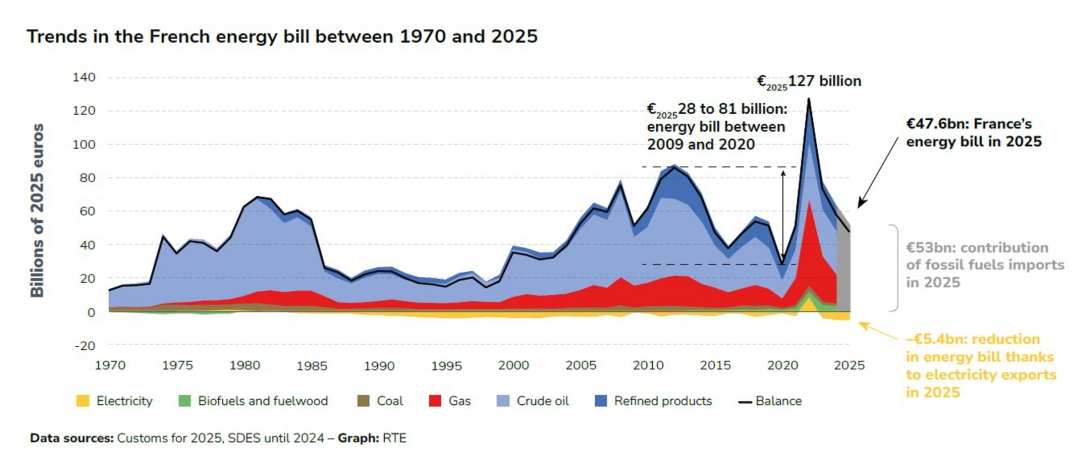

These trends confirm the diagnosis of the recent 2025 Generation Adequacy Report: the abundance of French low-carbon electricity generation puts the country in a very favourable position to decarbonise quickly and reduce its dependence on fossil fuels, which still account for almost 60% of its total energy consumption.

The total net value of France’s electricity exports amounted to €5.4bn in 2025 (or around €9bn taking into account the average price in the countries to which France exports), a level slightly higher than the previous year. This amount helps to reduce France’s “energy bill”, but it is still low compared with the cost of fossil fuel imports, which represent the largest heading in France’s trade deficit. In 2025, fossil fuel imports cost €53 billion3. In 2022, they amounted to over

€2025110 billion in the context of the energy crisis; by comparison, the fact that France was, unusually, an electricity importer that year only cost around €20258 billion.

The average price per MWh exported in 2025 (€59/MWh at the French price) is close to the average French spot price (€61/MWh). It remains close to the level of the previous year and slightly higher than during the 2010s. Valued at the average price of the countries to which France exports, on the other hand, it comes to €101.5/MWh. So, as in 2024, France did not “dump” its electricity at rock-bottom prices in 2025: it exported its competitive surplus production almost continuously, benefiting from a higher price differential with neighbouring countries than in 2024.

France plays the role of an “electricity crossroads”, and its exports reach the whole of Europe, not just neighbouring countries

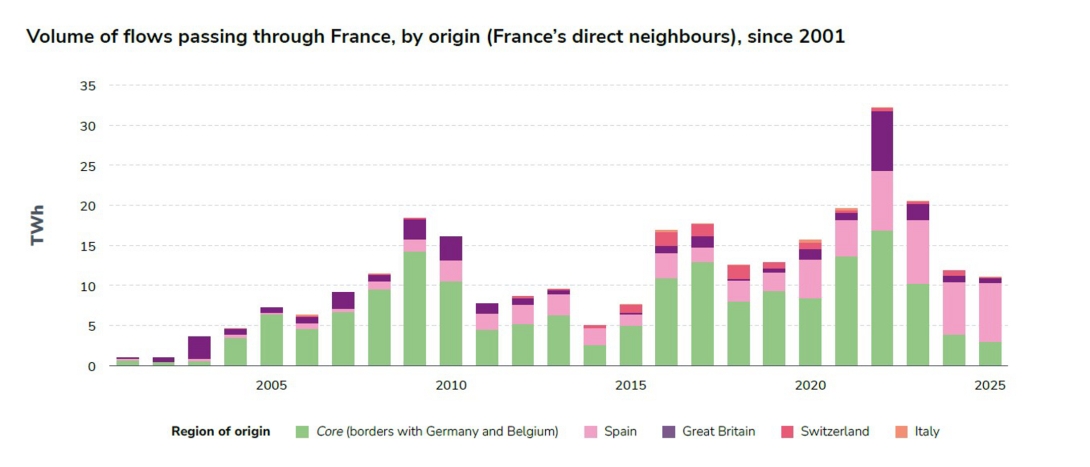

France was a net exporter almost 99% of the time in 2025. In practice, there are many situations in which France can be an exporter overall, while at the same time being an importer across certain borders. This reflects the fact that these imports do not correspond to a need within France during these periods, but to exchanges of electricity that pass through its network. In fact, the volume of imports supplying French consumption is extremely low: less than 0.2 TWh in 2025, i.e. only 2% of the volumes imported. The rest were flows imported from one border to be re-exported to other borders, i.e. “through flows”.

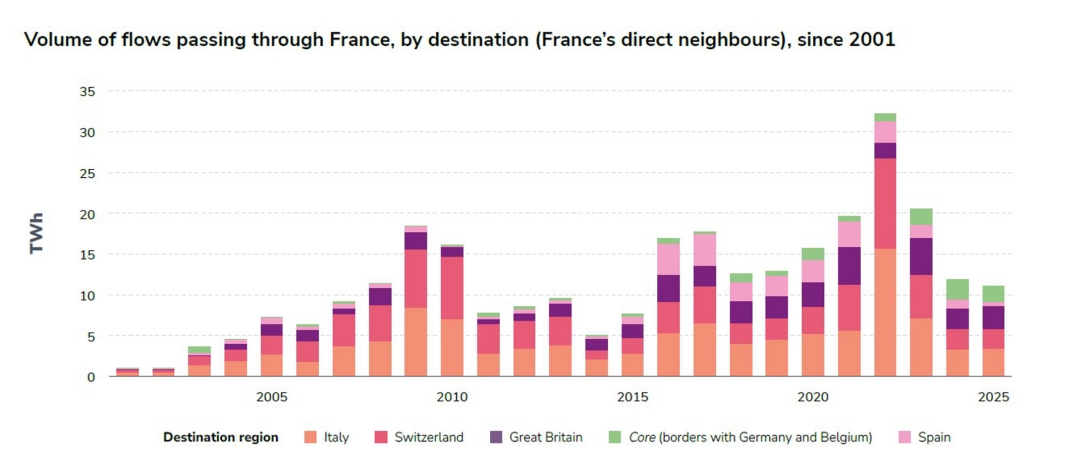

Because of its position as an “electricity crossroads” between its neighbours to the north, south-west and east, France automatically plays the role of a transit country. The volume of flows passing through France in 2025 amounted to 11 TWh, a similar volume to 2024, coming mainly from the Spanish border and to a lesser extent the borders with Germany and Belgium. Through flows reflect the operation of the interconnected European power system, in which economic optimisation leads to the least costly – and generally least carbon-intensive – generation sources across Europe being called on to feed consumption, independently of national borders, within the limits of interconnection capacities and the transit capacities of the national networks.

For example, the increase in exchange capacity with Spain over the coming years should lead to an increase in transits to the rest of Europe, which will generate more cross-border flows on the French network. For these interconnections to be exploited to the full, the internal network routes that will enable these transits to other countries also need to be identified and strengthened.

Due to the extensive interconnection of the European grid, France’s electricity exchanges with its immediate neighbours may also originate or terminate in countries with which it is not directly interconnected.

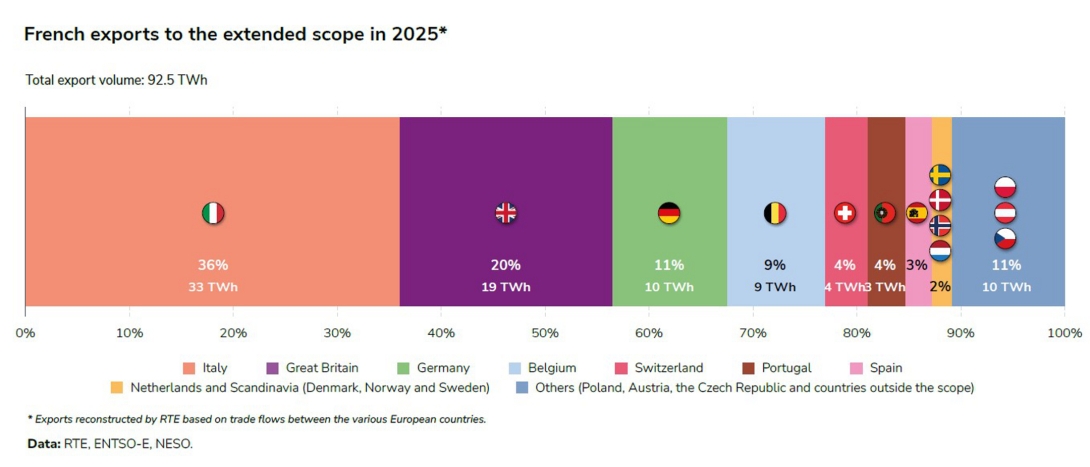

In 2025, 15% of French exports supplied consumption in non-bordering countries. The largest of these markets is Portugal, with 4% by volume (3 TWh), i.e. more than the French exports supplying Spanish consumption (2 TWh). In addition, exports to Switzerland are much lower than those identified by analysing borders with direct neighbours. Switzerland’s imports of French electricity for its own consumption represented only 4% of French exports in 2025 (4 TWh), whereas the total Swiss imports (including “re-exported” flows, particularly to Italy) accounted for 19%. As a result, Italian imports of French electricity, which at first glance represented only 25% of French exports, actually accounted for 36% (or 33 TWh) once flows transiting via countries such as Switzerland are included (see graphs opposite).

Finally, around 11% of France’s exports are destined for the rest of Europe (including Austria, Poland, Denmark and the Netherlands).

The carbon content of French electricity generation is one of the lowest in Europe, representing leverage for decarbonising the country’s energy consumption

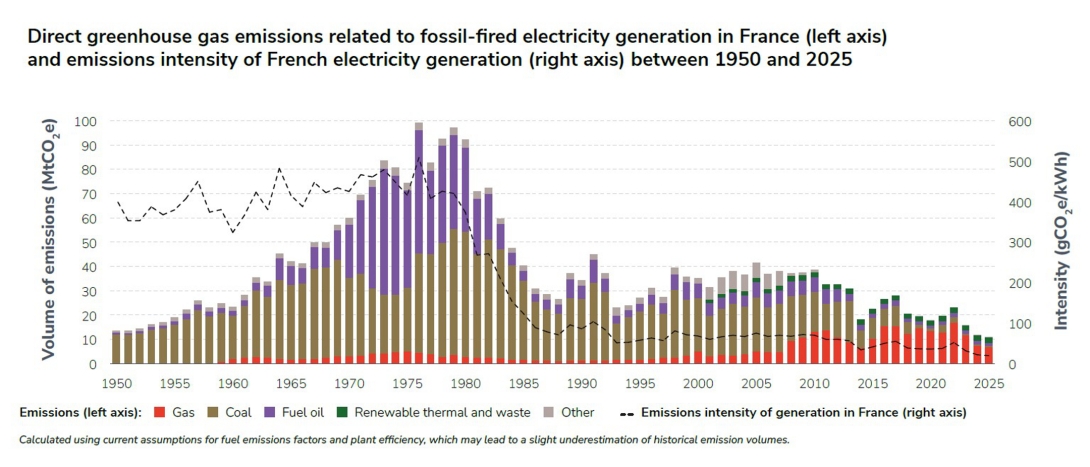

Emissions from electricity generation in France continued to fall in 2025, reaching a historic low of 10.9 MtCO2e, following levels of 11.7 MtCO2e in 2024 and 15.8 MtCO2e in 2023. For the third year running, this is the lowest volume since 1945.

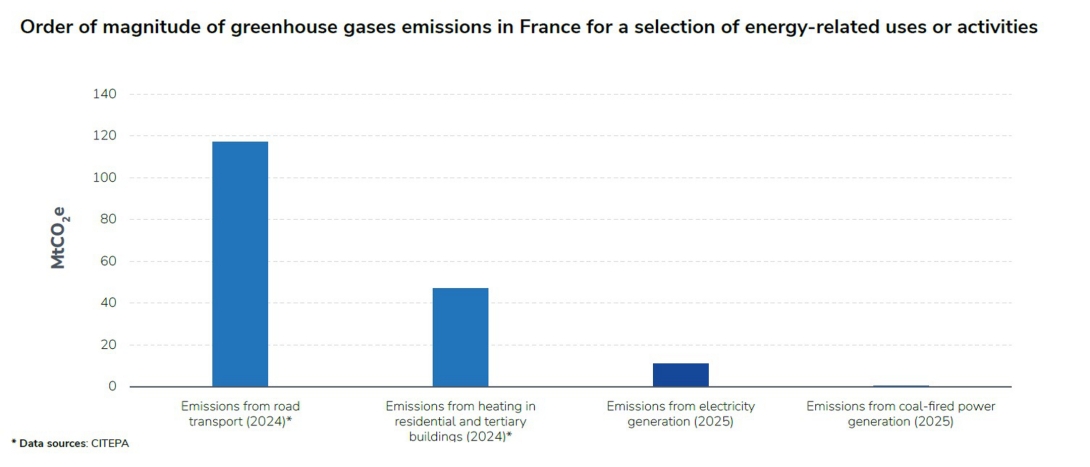

Emissions from electricity generation in France are extremely low compared with emissions from the most-polluting energy uses. They correspond to less than a tenth of the emissions from road transport (120 MtCO2e in 2024) and around a fifth of emissions from heating in residential and tertiary buildings (47 MtCO2e in 2024). This perspective helps to illustrate the overall finding of the 2025 Generation Adequacy Report: with French electricity generation now almost entirely low-carbon, the challenge for the country lies mainly in replacing fossil fuels with electricity on a large scale.

The average emissions content of French generation over the year as a whole was 19.6 gCO2e/kWh; this places France second only to Norway among the European countries with the lowest-carbon electricity mix. Nearly 95% of the electricity generated in France in 2025 was low-carbon. Lastly, emissions remained limited even during periods of high consumption: France’s maximum carbon intensity never exceeded 58 gCO2e/kWh, which is the average intensity that French production was still recording in 2013.

This historically low level can be explained by the use of fossil-fired generation being particularly infrequent, against a backdrop of abundant low-carbon generation. Production from the most polluting sources, coal and fuel oil, was virtually zero. Gas-fired generation, which is the least emissions-intensive of the conventional fossil fuels and now accounts for the bulk of fossil-fired generation in France, also reached an all-time low (see Generation). Total emissions from gas amounted to 6.7 MtCO2e, followed by 2.3 MtCO2e from waste and 2.0 MtCO2e from the remaining fossil fuels, including coal and fuel oil.

Moreover, these emissions are largely due to cogeneration coupled with district heating networks or industrial installations, or to waste incineration: they are thus largely inevitable and independent of the economic fundamentals of the power system.

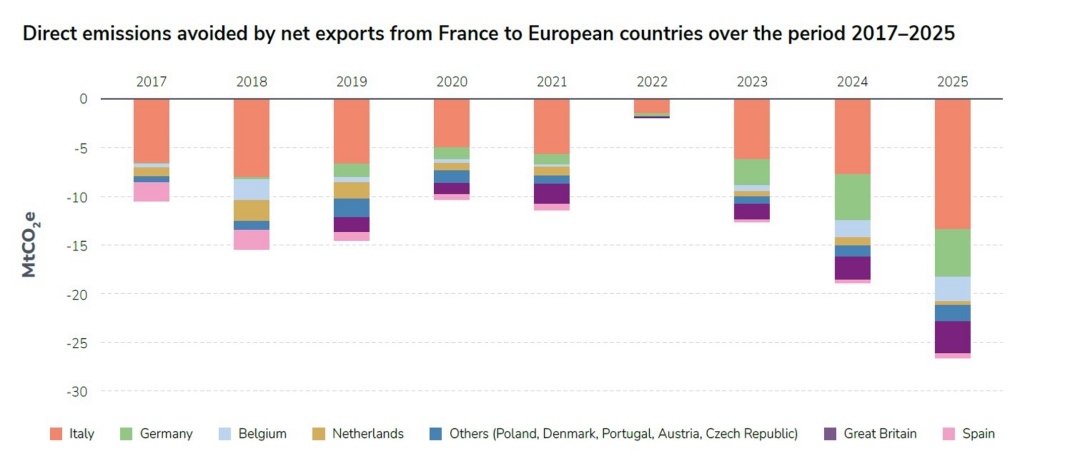

The abundance of competitive low-carbon electricity in France resulted in a very high net export balance (see the Trade section) to countries with more carbon-intensive electricity generation than France. As a result, French exports avoided 27 MtCO2e of emissions in 2025, mainly in Italy (half) and in Germany and Belgium (just over a quarter between them).

Even when life-cycle emissions are taken into account, the French power system still performs very well, with an intensity of 29.0 gCO2e/kWh. Total life-cycle emissions from electricity generation in France amounted to 15.7 MtCO2e in 2025.

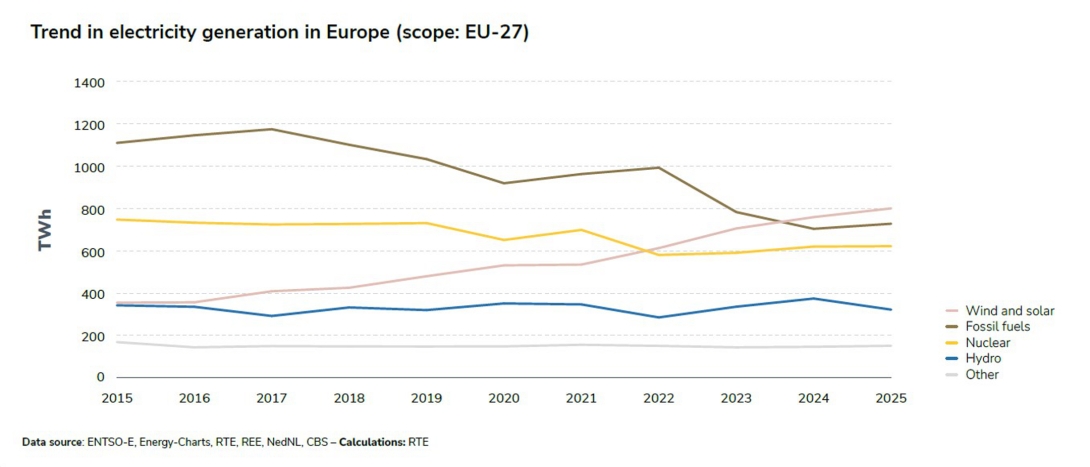

Consumption and generation remained stable in Europe, with solar and wind production outstripping fossil fuel output for the second year running

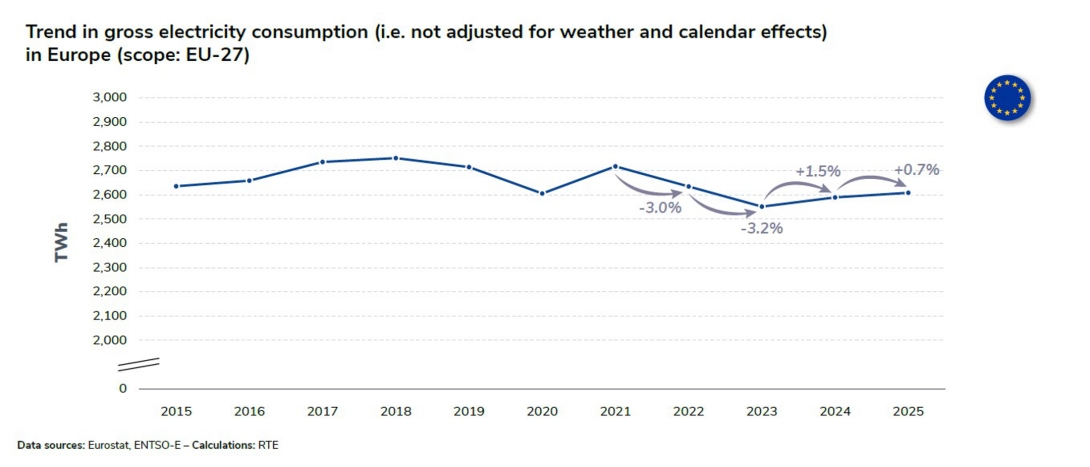

Electricity consumption in the European Union (not adjusted for weather and calendar effects) followed the same trend as in France, remaining relatively stable in 2025 compared with 2024 (+0.7%).

It remains 3.4% below the average level for the 2015–2019 period, which confirms that the drivers of the fall in demand in previous years in Europe have persisted in the short term, and particularly the development of energy efficiency and energy sobriety initiatives as well as the drop in industrial production in several countries.. For the time being, the effects of electrification remain hardly visible, despite progress in electrification rates in some countries, such as Denmark.

The volume of electricity generated within the European Union also remained relatively stable in 2025 compared with 2024 (+20 TWh, +0.8%), though with marked variations across the energy mix.

With an increase of 19% (+51 TWh, including only +8 TWh in France) in 2025 compared with 2024, solar output showed the strongest growth at a similar rate to the previous year. Wind generation fell slightly (–2%) as a result of unfavourable wind conditions, despite the increase in the size of the wind-powered generating fleet. Wind and solar power rose by two percentage points as a proportion of the European energy mix, from 29% to 31%, continuing to replace coal- and gas-fired generation in Europe.

Hydropower production fell significantly in 2025 (–14%, –52 TWh), after an exceptional year in 2024, to a level close to the average of the previous ten years.

European nuclear generation remained stable (+2 TWh), with contrasting trends in different countries: while French output increased by 11 TWh compared with 2024, the figure for other countries as a whole decreased by the same amount, for either structural reasons (reactor closures in Belgium) or cyclical reasons (maintenance, long downtimes).

The sharp fall in hydropower production led to a slight cyclical increase in fossil-fired generation in the European Union in 2025 (+3%), following two years of sharp falls (–21% in 2023 and –10% in 2024). This increase was driven by gas-fired generation, while coal continued to decline (–10 TWh or –4%) and now represents less than 10% of the generation mix. Despite the rise in gas-fired generation, combined solar and wind output exceeded fossil generation for the second year running.

As a result, 69% of electricity generation in the European Union is now low-carbon and 43% renewable, compared with 55% and 26% respectively in 2015.

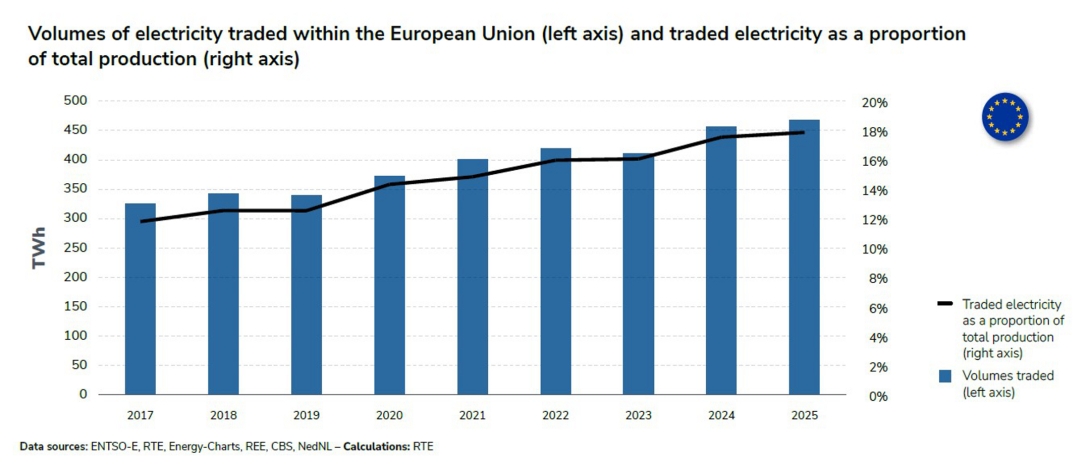

Trading continued to play its role in optimising the electricity generation mix across Europe. In 2025, 468 TWh were traded between EU countries, representing 18% of generation. These volumes have tended to increase over the last twenty years as a result of the development of interconnection capacity on one hand, and the success of growing integration between European markets on the other.

1

The figures presented in this section are calculated by RTE from SDES and CITEPA data.

2

Statistical Data and Studies Department (SDES), “Consommation d’énergie par usage du résidentiel” (Energy consumption by residential use), 2025

3

Source: Customs