BE 2025 - Échanges [EN]

Sections

Section externalisée

Menu tertiaire

Paragraphes de la section

The competitiveness of French generation led to a new export record in 2025, in line with the previous year

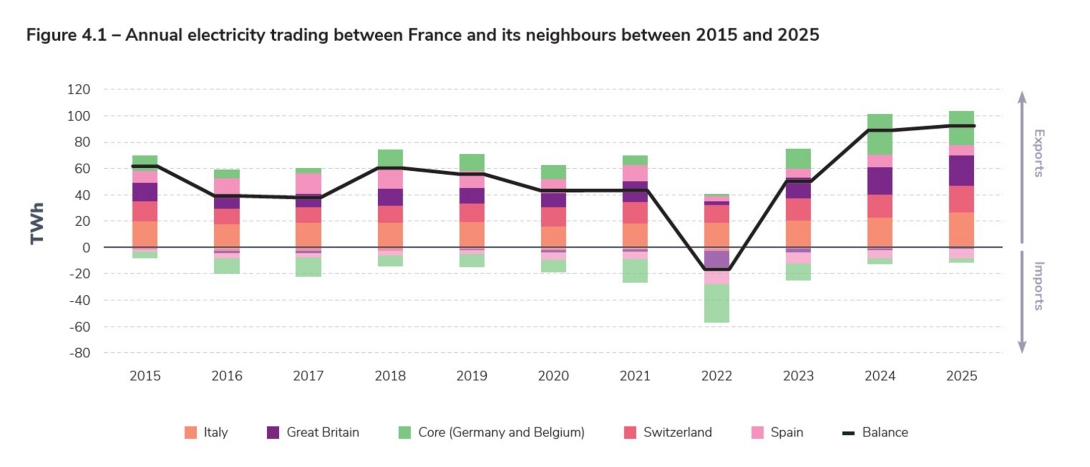

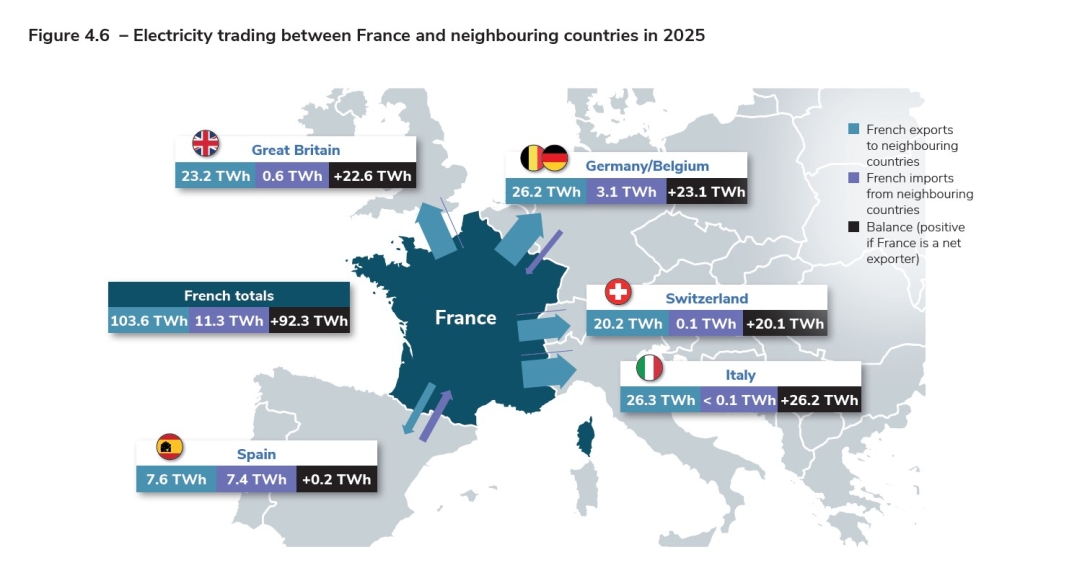

France’s net balance in 2025 was 92.3 TWh of exports. For the second year in a row, it was the highest since the beginning of trading between France and the other European countries, exceeding the 2024 export balance (89.0 TWh), in a generally similar context. For comparison, this represents a volume similar to the total electricity consumption of a country such as Belgium (around 80 TWh in 2025).

The balance of trade was very positive across all borders except to Spain, where trade was more balanced. It amounted to 22.6 TWh with Great Britain, 20.1 TWh with Switzerland, 26.2 TWh with Italy, 23.1 TWh with the Core region, i.e. the borders with Germany and Belgium, and 0.2 TWh with Spain.

The drop in hydropower production was offset by the return of nuclear power to pre-pandemic levels, as well as the increase in solar power output due to growth in the installed base and favourable sunshine conditions.

In addition, consumption remained stable compared with 2024, and is still below pre-crisis levels (see the Consumption chapter). Finally, the large export balances of 2024 and 2025 were enabled by the development of interconnections and the growing integration of Europe’s electricity markets.

These trends confirm the diagnosis of the recent 2025 Generation Adequacy Report: the abundance of French low-carbon electricity generation puts the country in a very favourable position to decarbonise quickly and reduce its dependence on fossil fuels, which still account for almost 60% of its total energy consumption.

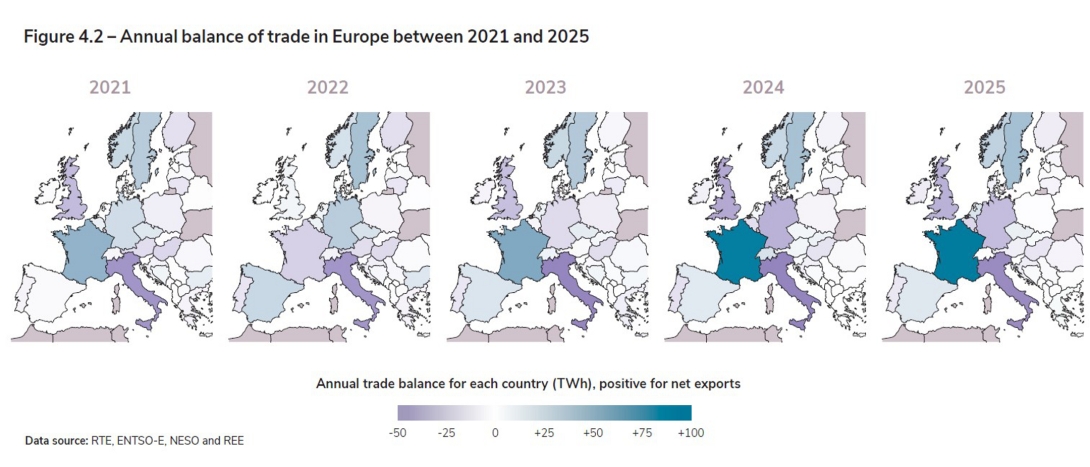

France remained Europe's leading net exporter of electricity by volume, as it has been almost every year for the past three decades1 (excluding 2016, 20172 and 2022). France exported the equivalent of 17% of its output in 2025, similar to the 2024 level (16.5%). France is not the only country to export such a high proportion of the electricity it generates: some northern European countries such as Norway and Sweden also have high export rates – around 22% for Sweden in 2025 – thanks to their large renewable generation capacity, mainly hydropower and wind. Conversely, other countries such as Italy, Portugal and Great Britain3 rely heavily on imports to cover their electricity consumption, in proportions of up to 15–20%.

Comparable proportions of exports had previously been achieved in France between 1992 and 2002, when they oscillated between 12% and 15% of national production. This was a time when the nuclear fleet had grown strongly and consumption was at lower levels than today (see the Focus on the historical view of French power trading).

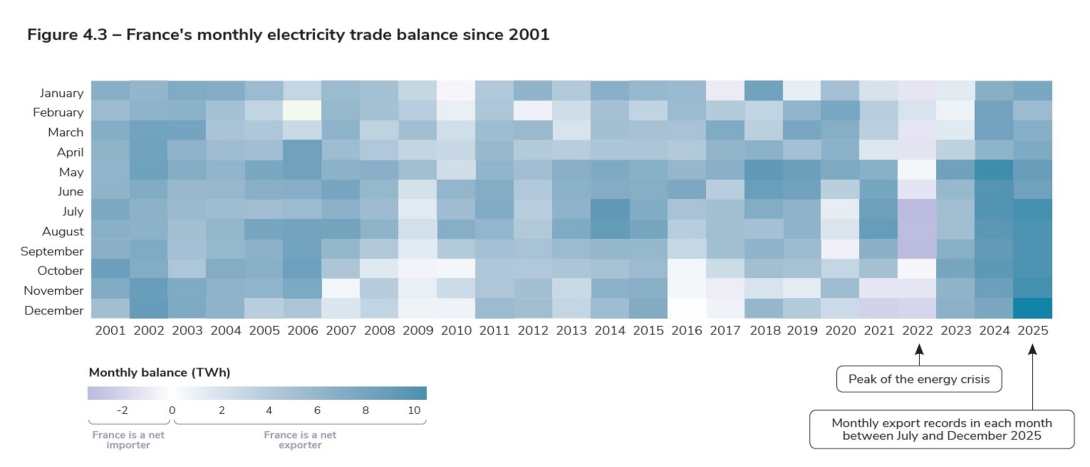

At the monthly level, the export balance remained strongly positive in every month of 2025, extending the trend observed since mid-2023. Values were slightly lower in the first half-year than in the second, driven by consumption and by higher prices at the beginning of the year.

Historically high levels of exports were recorded from July until the end of the year, driven by particularly significant trade with Great Britain, Italy, Germany and Belgium. Over this period, consumption remained virtually unchanged from the previous year (+0.1 TWh per month on average). At the same time, low-carbon generation increased overall: +1.2 TWh per month on average for nuclear, +0.8 TWh for wind, +0.7 TWh for solar. Only hydropower output fell, by an average of −1 TWh per month. December saw a new monthly export record, reaching 10.5 TWh. During this month, nuclear generation reached a level not seen since January 2019.

Focus: Electricity markets aim to optimise the use of the resources available

The power systems of the different European countries are now widely interconnected. Most countries in continental Europe are part of the synchronous continental power system, which shares the same 50 Hz electrical frequency at all times.

By making it possible to take advantage of the synergies between national energy mixes, the interconnection of the power systems benefits the European community in three ways: by reinforcing the security of the electricity supply and operational security, by reducing production costs on a continental scale through the use of the least expensive production resources, and by making it possible to integrate greater volumes of decarbonised energy.

Trade between European countries means that the least expensive (and therefore often least carbon-intensive) generating capacity available can be called on at any given time to cover electricity consumption in Europe, even in high-pressure situations. This possibility proved essential when supply to the French power system came under pressure in the autumn and winter of 2022/2023. As a general rule, the integration of the European power system is particularly beneficial in making it possible to take advantage of the varied consumption profiles in different countries. For example, consumption peaks do not occur at the same time of day or in the same season in different countries – they happen on summer afternoons in Italy, on winter evenings in France and on winter mornings in the Scandinavian countries. To a lesser extent, pooling also enables full advantage to be taken of the different production profiles of variable renewable energy.

Over the past fifteen years, the strengthening of interconnections between countries and the development of variable renewable energy have led to a significant increase in electricity trading between European countries, and France is at the heart of this trading. Located at the intersection of several electrical peninsulas (Iberian peninsula, Italy, Great Britain) and with significant installed generating capacity, France participates fully in European trade. France’s energy mix, made up mainly of low-carbon generation sources (nuclear, hydro and other renewables), is on the whole more competitive than that of most of its neighbours. As a general rule therefore, in the absence of pressures on the national supply–demand balance, the power system is a significant exporter across the scale of a year: supply from French nuclear and renewable generating capacity is called on by the markets before thermal production units, including those in neighbouring countries (within the limits allowed by interconnection

capacity). At other times, even in non-crisis situations, it is normal for the country to be a net importer from time to time, for a few hours or a few days: this is typically the case when it is cheaper to import than to generate additional volumes in France. This happens, for example, when there is high renewable generation in neighbouring countries, particularly Spain or Germany (see the details for each border below).

France’s interconnection with other European countries, and its full integration into the market mechanisms governing trade, mean that it can:

- find economic outlets for its low-carbon generation and contribute to decarbonising the European mix on one hand;

- ensure its security of supply at a much lower cost than if the country had to rely solely on national generation resources at all times, on the other.

By 2030, RTE will have completed work on the two DC connection projects currently under way with Spain and Ireland. In addition to these projects, work is planned on the existing network at the Spanish, Belgian and German borders, which will also increase trading capacity. However, additional projects can only be decided on if the physical situation of the French network, located at a European electricity crossroads, is taken into account. In 2025, a very small proportion (2%) of France's imports supplied French consumption; the rest were flows imported from one border to be re-exported to other borders (see the analysis later in the chapter). These flows have an impact on the domestic power grid, as highlighted in the Ten-Year Network Development Plan (SDDR 2025). The development of new interconnections will thus depend on the acceleration of measures to strengthen the French domestic grid, which will involve greater financing requirements than the SDDR's reference pathway for the period between now and 2035.

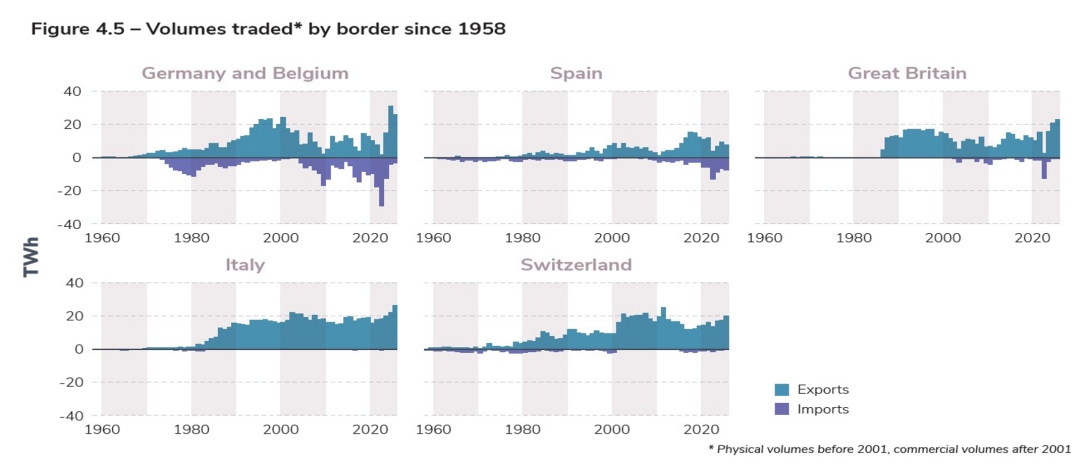

Focus: A historical overview of French electricity trading

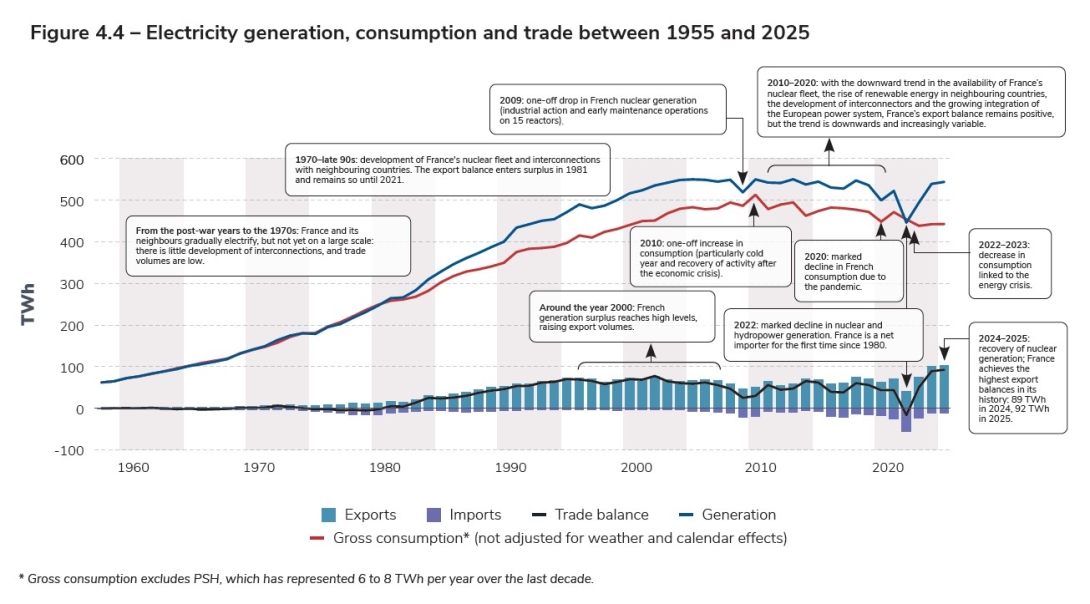

Before 1945, electricity played a relatively minor role in the country’s energy system. The first power stations in France, built at the end of the 19th century, were either hydroelectric or coal-fired. Electricity became widely used over the first half of the 20th century, particularly for lighting, but there was still no unified transmission grid, and generating facilities were mostly private, for industrial use. The bulk of electricity generation came from coal and hydropower.

From the post-war period until the end of the 1970s, electricity consumption increased significantly (+1% per year on average), against a backdrop of strong economic growth and the electrification of the country. The first interconnection between the French, Swiss and German networks was created in 1958.

Following the first oil crisis in 1973, France rapidly developed a large fleet of nuclear reactors to reduce its dependence on fossil fuels. During this period, 48 nuclear reactors were commissioned between 1978 and 19894. At the same time, the development of electrification was encouraged, particularly by incentivising the installation of electric heating and water heaters. However, under the combined effect of energy-saving policies, slower economic growth and the oil crisis of 1986, which led to sustained low fossil fuel prices until the end of the 1990s, electricity consumption did not grow as fast as projected, leading to a structural surplus of electricity generation in France, which could then be exported.

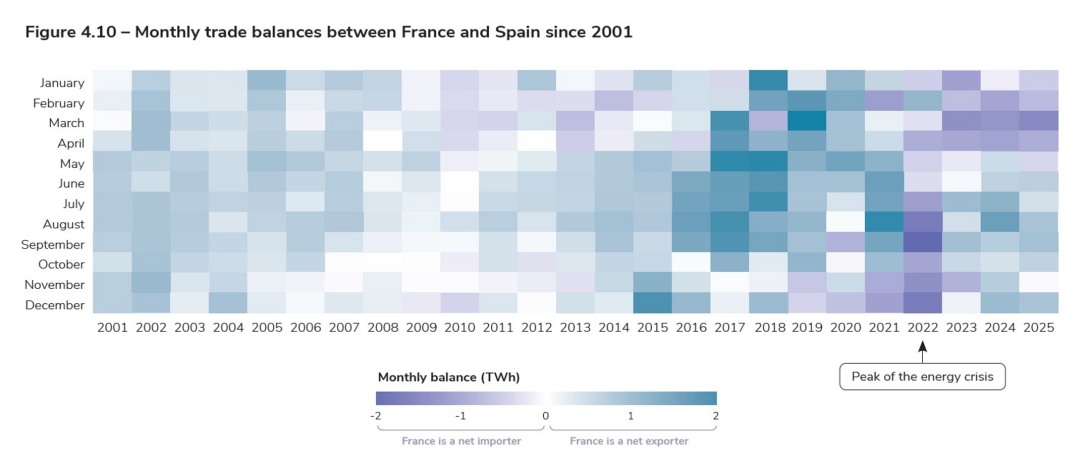

As a result, France's trade balance recorded a surplus from 1981, and exceeded 60 TWh from 1993, supported by the growing interconnection of electricity grids and the competitiveness of France's nuclear fleet. A local peak was reached in 2002, with an export balance of 76 TWh. The last second-generation nuclear reactor was commissioned in the same year.

During the 2000s, electricity consumption continued to increase. At the same time, generation levelled off from the middle of the decade, partly due to the lack of new nuclear projects coming on stream and the absence of any marked drive to develop the renewable fleet.

From the late 2000s and during the 2010s, the availability of the French nuclear fleet declined as maintenance operations became more intensive due to the ageing of the plants and the launch of the “Grand carénage” refurbishment programme. The Fessenheim power station shut down permanently in 2020. In parallel, renewable energy, and particularly wind and solar power, expanded in France and Europe. France's trade balance remained positive, even though the proportion of generation destined for export no longer reached the unusually high levels seen in the early 2000s.

After a marked decrease during the energy crisis in 2022 (when France became an importer), the country's balance broke its 2002 export record (76 TWh) two years in a row in 2024 and 2025, with 89 TWh and then 92 TWh respectively, driven by strong low-carbon generation (thanks partly to the recovery in nuclear availability) and consumption that was lower than in the 2010s.

As a result, the French power system is currently experiencing a situation of national electricity abundance, though this is not unprecedented. In the electricity industry, cycles occur regularly because of the contrast in time scales between the inertia associated with developing generation and network infrastructure, which extends over several years or even decades, on one hand and the occurrence of energy and economic crises or major shifts in consumption, which happen over much shorter periods of time, on the other. This can lead to periods, such as the current one, when the growth dynamic of electricity generation is temporarily out of sync with growth in consumption.

1

The Eurostat data used to calculate the balance for each European country only goes back to 1990.

2

France was Europe's second largest exporter in those years, behind Germany.

3

In analysing trade, we consider Great Britain rather than the whole United Kingdom, as Northern Ireland is part of the integrated Ireland/Northern Ireland market area (see the Focus on the details of trade with Great Britain).

4

Assemblée Nationale – Office parlementaire d’évaluation des choix scientifiques et technologiques, Rapport sur l'aval du cycle nucléaire – Les coûts de production de l’électricité, February 1999

Section externalisée

Menu tertiaire

Paragraphes de la section

Trade with neighbouring countries: contrasting trends at different borders

Although the net balance of electricity trading in 2025 was close to that of the previous year, the trends varied slightly from one border to another.

The balance of exports increased in relation to Great Britain (22.6 TWh, i.e. +2.5 TWh compared with 2024) and Italy (26.2 TWh, i.e. +3.9 TWh compared with 2024), mainly due to better availability of exchange capacity with these two regions. The balance also increased in relation to Switzerland (20.1 TWh, i.e. +3.5 TWh), where a nuclear power station has been shut down for technical reasons since May 20255. However, it fell with Spain (0.2 TWh, or −2.6 TWh), mainly as a result of significant imports from this region at the beginning of the year, when French consumption was at its highest, and with the Core region, i.e. the borders with Germany and Belgium (23.1 TWh, or −4.1 TWh), mainly due to maintenance work on the interconnection lines across these borders in the spring and summer of 2025.

Onglets

Paragraphes

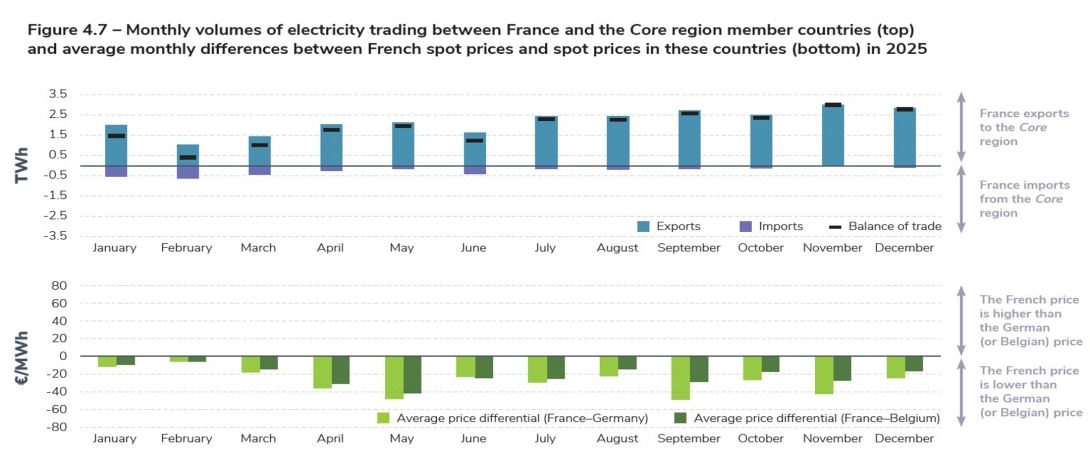

France exported a high volume to the Core region, but less than in 2024

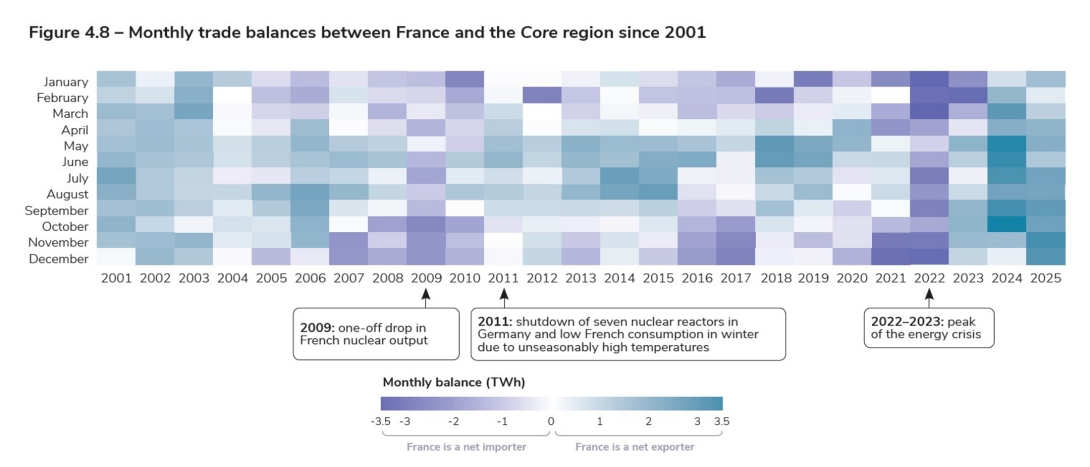

The balance of trade between France and its neighbours in the Coreregion, i.e. Germany and Belgium, was 23.1 TWh in exports. This is the second highest export balance ever recorded across this border, behind 2024 (27.2 TWh) and ahead of 2001 (17.1 TWh). The balance was 4.1 TWh lower than the previous year due to the drop in the volume exported from France to Germany and Belgium (from 31.3 TWh in 2024 to 26.2 TWh in 2025), which was not offset by the drop in the volume imported (from 4.1 to 3.1 TWh). The reduction in volume of trade is mainly due to major maintenance work on the Franco-Belgian interconnections during 2025. The export balance was exceptionally strong at the end of the year (whereas France has generally been a net importer from Core during this period) due to particularly low renewable generation in Germany and high low-carbon generation in France.

The total volumes traded with the Core region (absolute value of imports plus exports) were the highest; exchange capacity is also higher than across the other borders6. Historically, trade with this region has been highly variable, depending on the period or the year: this is due to market integration, but also to the significant change in the generation mix in the region over time, including an increasingly high proportion of low-carbon generation, particularly wind and solar. As of the end of 2025, more than 115 GW of solar power was installed in Germany and Belgium. The effect of solar generation is particularly visible: France was a net importer from the Core region in the middle of the day (12 pm–2pm) on almost 40% of days in 2025, whereas this figure falls to an average of 7% from 5 pm to 8 am.

Prior to 2022, France exported to the Core region during the summer, when French consumption is lower, and imported from the Core region during the winter. This pattern has changed since 2023: the export balance from France to the Core region has been positive every month since May 2023. The annual balance of trade between Germany and its neighbours has tilted towards imports since 2023 (28 TWh of imports in 2024, 22 TWh in 2025), with the nuclear phase-out completed at the beginning of 2023 and the gradual closure of coal-fired power stations (scheduled for complete shutdown by 2038 at the latest). A similar trend is occurring in Belgium, in a similar context of nuclear power plant shutdowns7. French exports to Germany and Belgium also contribute to consumption beyond these two countries, which accounts for 30% of the 26 TWh exported, particularly to other Central European countries (see the analysis of flows exported beyond neighbouring countries later in this chapter).

Paragraphes

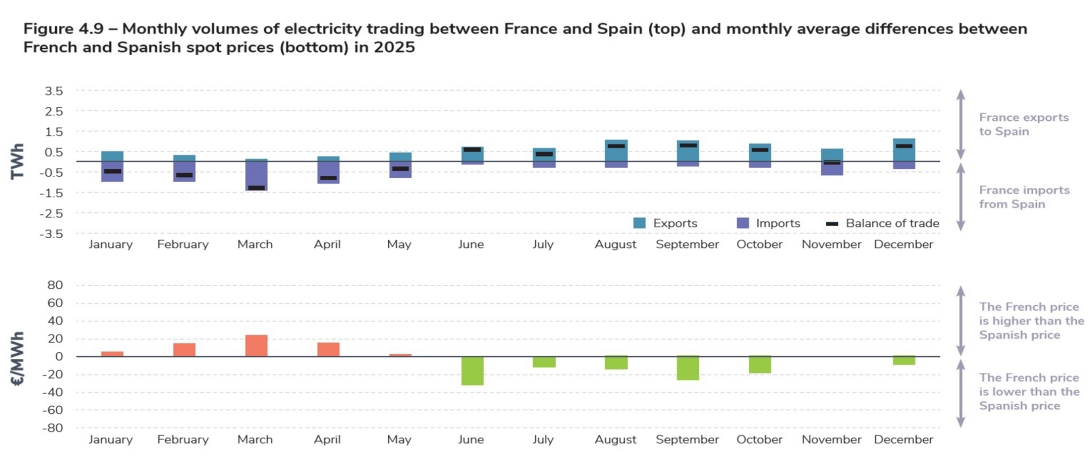

Trade with Spain remained balanced

France's net trade with Spain was close to being balanced in 2025, amounting to 0.2 TWh (7.6 TWh of exports and 7.4 TWh of imports).

Until 2022, France was generally an exporter to Spain; since the energy crisis in 2022, when France exceptionally became a net importer across this border, trade has been more balanced, being slightly negative in 2023 and slightly positive in 2024 and 2025. This results from the increased competitiveness of the Spanish generation mix, with its low-carbon share (nuclear and renewable) rising from an average of 66% over the 2015–2019 period to an average of 78% between 2023 and 2025. Spanish wind production in particular has influenced the direction of trade8. It should also be noted that most of France’s exports to Spain are re-exported by Spain at the same time to Portugal and Morocco (see analysis below).

The average price in Spain was €66/MWh in 2025, compared with €61/MWh in France. This is the lowest price among France's neighbours. Spain was the only country where the average monthly spot price was lower than the French price; this was the case from January to May, and again in November. Between January and May, therefore, trade was mainly from Spain to France. From June onwards, the direction of trade reversed, as consumption fell in France at the end of the heating period and increased in Spain with the rise in air conditioning (+18% in July compared with May), and French nuclear availability remained relatively high for the season. The export balance turned slightly negative in November, before becoming mainly positive again in December.

It is interesting to compare trade trends with the summer – the temperature sensitivity of consumption consumption profiles in France, Spain and even is lower there than in France (see Europe chapter). Portugal. Consumption on the Iberian peninsula As a result, France often imports from Spain in winter has a “flatter” profile over the year than in France, and exports to Spain in summer. although it is slightly higher in winter and early summer – the temperature sensitivity of consumption is lower there than in France (see Europe chapter). As a result, France often imports from Spain in winter and exports to Spain in summer.

Paragraphes

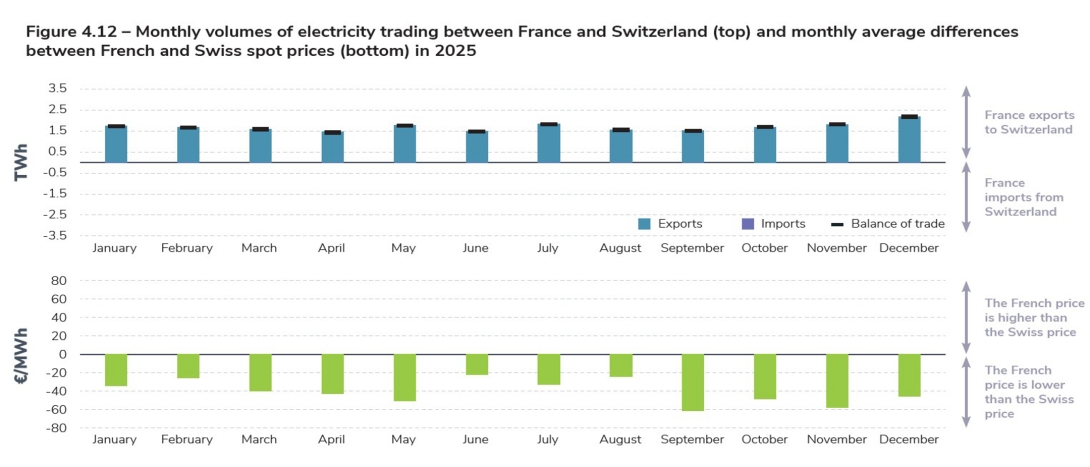

Switzerland imported from France throughout the year

The French export balance with Switzerland was clearly positive, reaching 20.1 TWh, the highest value since 2011, when the balance stood at 25.2 TWh. This 2011 record remained unbroken, however, due to lower exchange capacity resulting mainly from pressures on the Swiss network.

The average spot price in Switzerland was 30% higher in 2025 than in 2024. Only the Italian price was higher among France's neighbours. This increase was partly due to the extended shutdown of the Gösgen nuclear power station, which supplied on average 13% of Switzerland's electricity needs, from May 20259. The difference with the French price (over €40/MWh) is the highest since the creation of the Swiss electricity market.

France's export balance with Switzerland has generally been positive, although growth in solar generation from the mid-2010s onwards has led France to import more often during the spring and summer months. In 2025, trade remained largely export-oriented in every month of the year. In addition, Switzerland plays the role of a “transit country”, given its central position in Europe: about 80% of the flows exported to Switzerland are directed to other neighbouring countries, such as Italy (see the analysis in the “flow tracing” section).

Paragraphes

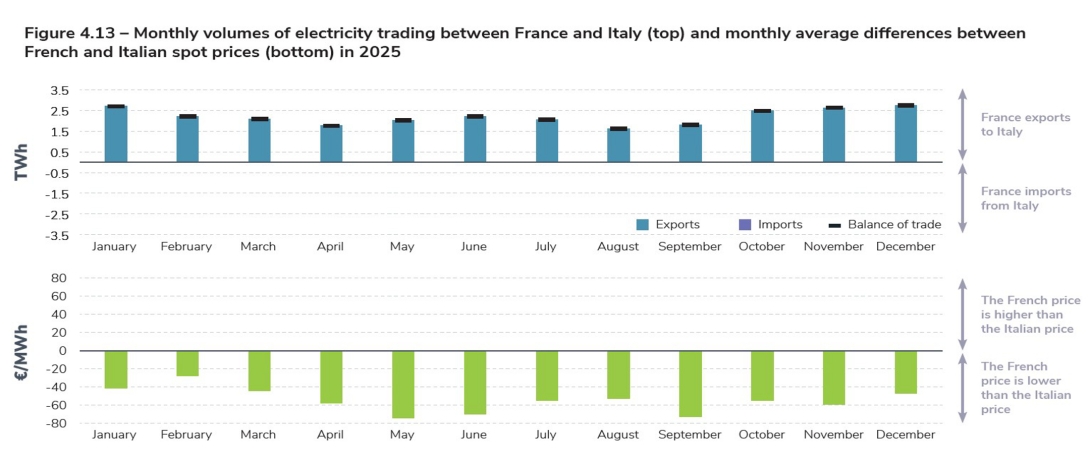

Exports to Italy reached a new peak

Historically, trade between France and Italy has tended to favour exports to Italy: France has been a net exporter to Italy every year since 1979. Italian electricity generation, which is still heavily dependent on gas, is structurally less competitive than French or Swiss generation. Since the late 1980s, imports have accounted for between 10 and 15% of Italy’s domestic electricity consumption10. In 2025, the dynamic was in line with historical trends: France exported massively to Italy. The net annual balance across this border was 26.2 TWh, the highest ever recorded, ahead of 2024 (22.3 TWh) and 2002 (22.1 TWh). Volumes are on the rise, due partly to the abundance of low-carbon generation in France, the commissioning of a new 1,200 MW interconnector between France and Italy in 2023, and the fact that there were fewer maintenance operations on the French–Italian interconnectors in 2025 than in 2024. In addition, the average Italian price was €116/MWh, almost double the French price (€61/MWh). This is the biggest price differential between Italy and France since the markets opened.

Paragraphes

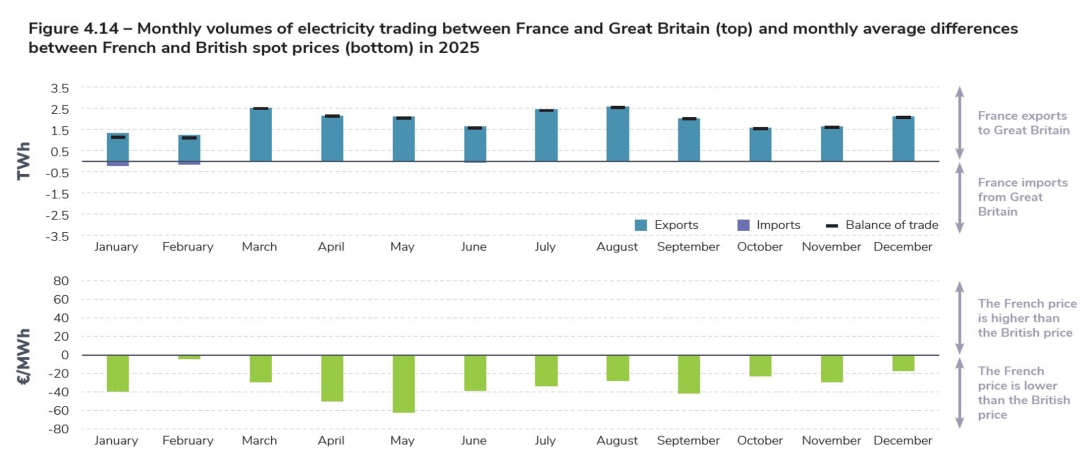

Exports to Great Britain reached their highest level ever

In 2025, the export balance with Great Britain stood at 22.6 TWh; 23.2 TWh were exported, and 0.6 TWh were imported, mainly in January and February. This constitutes the largest net export balance France has ever recorded across this border, beating 2024’s previous record of 20.1 TWh, thanks in particular to better interconnector availability. These consecutive records owe a great deal to the increase in exchange capacity in 2021 (IFA 2) and 2022 (ElecLink).

Since the IFA 2000 interconnector between Great Britain and France was commissioned in 1986, Great Britain has imported large volumes of electricity from France for much of the year, despite the fact that the British electricity generation mix includes a fast-growing proportion of low-carbon energy (mainly wind, but also nuclear and, to a lesser extent, solar, hydro and biomass). In winter, however, during periods of high wind generation in Britain, or when consumption is high in France, the trade is often reversed, with France importing from the UK.

Focus: Background: Why do we talk about the “British” power system?

We refer to trade with Great Britain, and not with the United Kingdom, because the power systems of the island of Great Britain and of Northern Ireland are not synchronous, are not managed by the same transmission system operator (NESO or National Energy System Operator for Great Britain and SONI for Northern Ireland), and do not belong to the same market area. The Northern Irish power system is integrated with the Republic of Ireland’s system; the two Irish transmission system operators (EirGrid for the Republic of Ireland and SONI for Northern Ireland) have jointly operated a single market area for the entire island of Ireland, the Single Electricity Market, since 2007. The Irish network is interconnected

with the British network by three DC links with a capacity of 500 MW each: the East-West Interconnector between the

Republic of Ireland and Wales, the Moyle Interconnector between Northern Ireland and Scotland, and Greenlink between the Republic of Ireland and Wales, which was commissioned in 2025. A fourth HVDC link is also planned, this time between the Republic of Ireland and France: the Celtic Interconnector, capacity 700 MW, with commissioning scheduled for 2028.

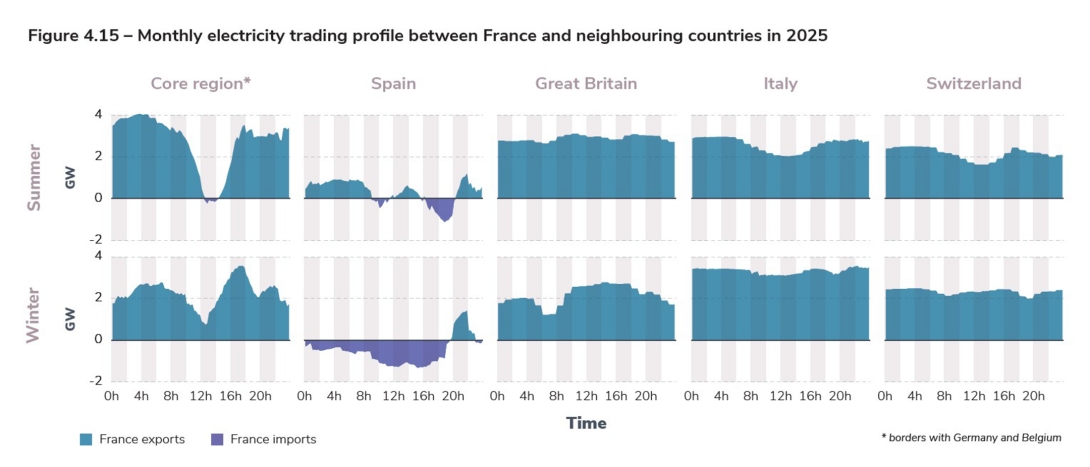

The daily trading profiles at each border are driven by consumption and low-carbon generation levels in France and the neighbouring countries

Although France is generally a major electricity exporter on a monthly or annual basis, electricity trading between France and its neighbouring countries changes significantly from hour to hour and from day to day, depending on the characteristics of the different generation mixes and the structure of daily consumption in each country. As a result, hourly trade patterns vary according to season and border.

For example, France's trade with Italy and Switzerland is largely export-oriented for most of the day. On summer days, however, there is a noticeable drop in French exports in the early afternoon, reflecting the rise in solar generation in neighbouring countries, which makes their electricity more competitive at these times and reduces their need to import. This phenomenon is even more visible in trade with Belgium and Germany, which have over 115 GW of solar capacity in total: excluding the late morning and early afternoon, trade amounts to more than 2 GW of exports on average, but this falls sharply from 10 am onwards, even reversing during the summer period, when France becomes an importer.

Contrary to what one might expect, the opposite phenomenon is observed in summer at the Spanish border. Between midday and 4 pm, although Spanish solar output is high, Spain regularly imports electricity from France, where solar generation is also high. These imports, at a time when Spanish consumption peaks due to the use of air conditioning, are generally re-exported to Portugal and, to a lesser extent, Morocco. France then begins to import from Spain in the late afternoon, when French consumption rises, and then exports again after 8 pm when consumption peaks in the evening in Spain.

In Germany, the evening consumption peak is about an hour before the French peak. This schedule difference is reflected in trade with the Core region: in winter, French exports peak between 4 pm and 6 pm, then gradually decline to a trough around 7 pm to 8 pm, corresponding to the time when French demand peaks. This reduction in exports at the point when French consumption peaks at 7 pm in winter is widespread, and can also be seen in the patterns of trade with other countries.

This illustrates how trade makes it possible to take advantage of differences in renewable energy consumption and generation profiles, even though there is a degree of correlation between French renewable generation profiles and those of neighbouring countries, which can limit outlets on the European market (and therefore the possibilities of exporting surplus production) and lead to power generation being modulated downwards.

5

It is worth noting that a significant proportion of exports to Switzerland are re-exported to Italy – see the “Flow tracing” section.

6

In addition, the border with the Core region is the only French border on which exchange capacity is determined on the basis of a so-called “flow-based” approach, which optimises the use of exchange capacity.

7

Of Belgium's seven nuclear reactors, two were shut down in 2022–2023, and three in 2025. It should be noted, however, that in March 2025 the Belgian parliament repealed the 2003 law on nuclear phase-out, thereby removing any reference to the end of nuclear in 2025, as well as the ban on Belgium building new nuclear generating capacity.

8

View detailed analysis: RTE, 2024 Electricity Review – Trading chapter – details for each border, February 2024

9

The shutdown, scheduled to last until the end of February 2026, was due to the discovery of a potential weakness in the specification of the water supply system.

10

Terna, Dati statistici sull’energia elettrica in Italia, 2023. Since the commissioning of the new Savoie-Piedmont interconnector in 2023, this proportion has risen to 17%–19%.

Section externalisée

Menu tertiaire

Paragraphes de la section

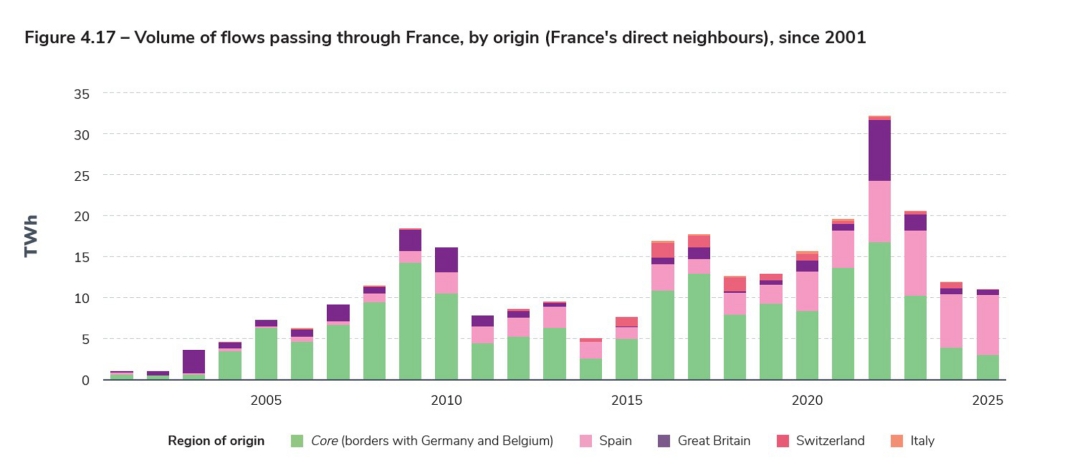

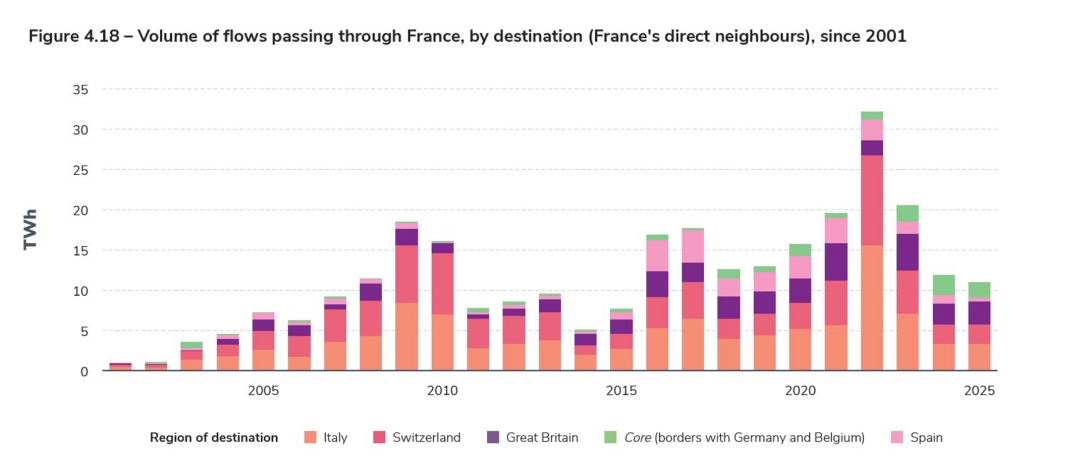

French exports reach all of Europe, not just the neighbouring countries

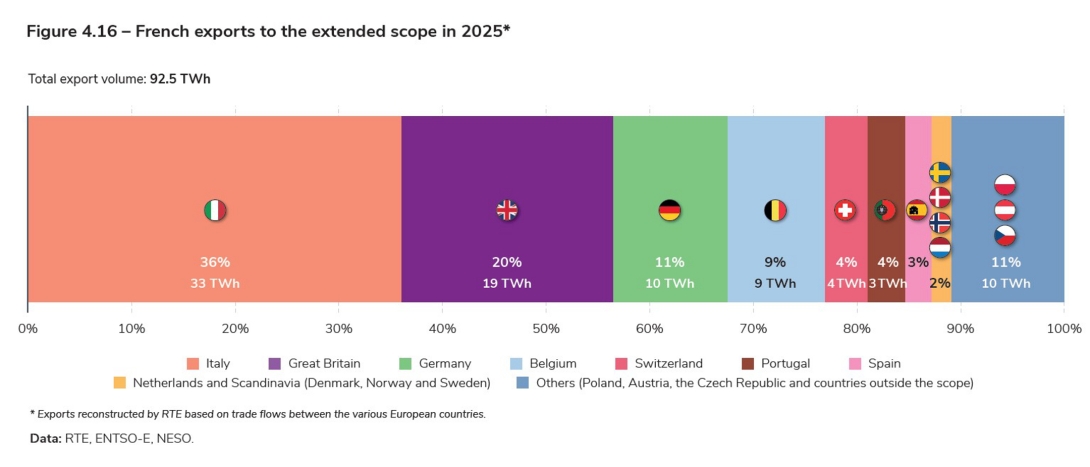

Due to the extensive interconnection of the European grid, France's electricity exchanges with its immediate neighbours, as presented in the border-by-border analysis, may also originate or terminate in countries with which it is not directly interconnected. Schematically, if, over a given period of time, France exports electricity to Spain but Spain exports it to Portugal at the same time, then it may be legitimate to consider that, over the period in question, part of the electricity traded between France and Spain is destined for Portugal. Similarly, if France exports electricity to Italy but imports it at the same time from Germany, it may be legitimate to consider part of these exports as coming from Germany and not from French production. The results of the analysing the trade using this approach, known as “flow tracing”, with a European scope extended to 15 countries11, are presented here. This is not measured data but the results of modelling12, but it can still provide additional information useful for understanding the operation of the European power system.

This analysis shows, firstly, that a large proportion of France’s imports “pass through” the country, and do not supply French consumption. France was a net exporter almost 99% of the time in 2025. In practice, even if France is a net exporter during a given period, it may simultaneously be importing from another country. A situation in which exports exceed imports (net export position) reflects the fact that these imports do not correspond to a need within France during these periods, but to exchanges of electricity that pass through its network. The volume of imports supplying French consumption, as defined by this approach, is thus extremely low: less than 0.2 TWh over the year.

Analysing the trade across each border, we can see that exports to Switzerland are much lower according to the “flow tracing” analysis than those identified in the bilateral analysis for borders with direct neighbours. This is because Switzerland is a transit country13: Switzerland's imports of French electricity for its own consumption represented only 4% of French exports in 2025 (4 TWh), whereas the total Swiss imports (including “re-exported” flows, particularly to Italy) accounted for 19%. As a result, Italian imports of French electricity, which at first glance represented only 25% of French exports, actually accounted for 36% (or 33 TWh) once flows transiting via countries such as Switzerland are included.

Ultimately, 15% of French exports supplied consumption in non-bordering countries in 2025. The largest of these markets is Portugal, with 4% by volume (3 TWh), i.e. more than the French exports supplying Spanish consumption (2 TWh). Finally, around 11% of France's exports are destined for the rest of Europe (including Austria, Poland, Denmark and the Netherlands).

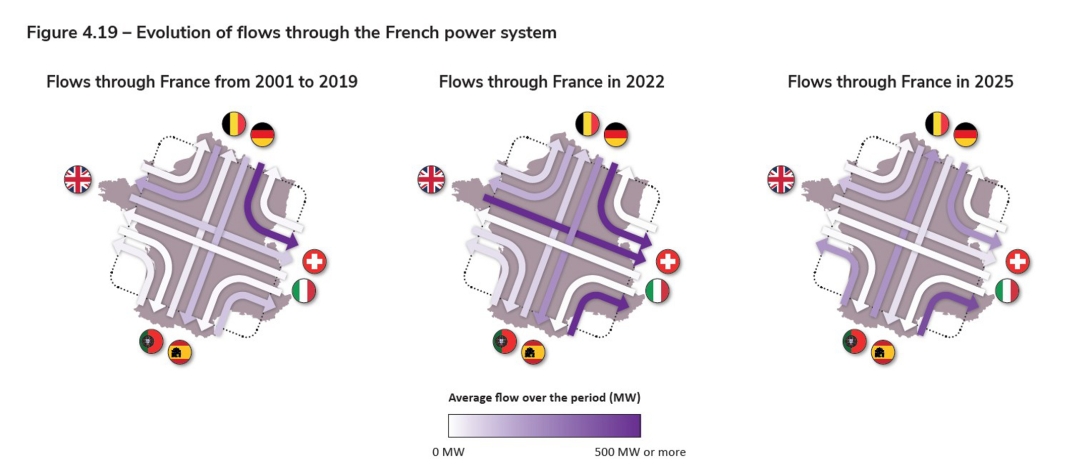

With the transformation of the French and European electricity mix, the French power system is playing the role of an “electricity crossroads”

Because of its position as an “electricity crossroads” between its neighbours to the north, south-west and east, France automatically plays the role of a transit country. In 2025, the volume of flows passing through France amounted to 11 TWh; this is similar to the 2024 volume, down on 2022, and is the lowest since 2015. This can be explained by the abundance of low-carbon domestic production, which made France's average and primarily supplied the import needs of its neighbours. In 2022, when French nuclear output was at its lowest level since 1988 and hydropower production was also low, a record 32 TWh passed through France, mainly from Core, Spain and Great Britain to Italy and Switzerland, where spot prices were higher than in France.

Through flows reflect the operation of the interconnected European power system, in which economic optimisation leads to the least costly – and generally least carbon-intensive – generation sources across Europe being called on to feed consumption, independently of national borders, within the limits of interconnection capacities and the transit capacities of the national networks.

Over the last few years, through flows have risen from Spain, as a result of its increasingly competitive generation mix, but decreased from Germany and Belgium, whose trade balances have recently switched from exports to imports – see the previous section. Of the 11 TWh that passed through France in 2025, 7 TWh came from Spain and 3 TWh from the Core region. Historically, these through flows were mainly destined for Italy and Switzerland14, though the distribution was more balanced in 2024 and 2025.

For example, the increase in exchange capacity with Spain over the coming years should lead to an increase in transits to the rest of Europe, which will generate more cross-border flows on the French network. For these interconnections to be exploited to the full, the internal network routes that will enable these transits to other countries also need to be identified and strengthened.

11

The 15 countries are: France, Spain, Portugal, Italy, Switzerland, Austria, Germany, the Czech Republic, Poland, Belgium, the Netherlands, Sweden, Norway, Denmark and Great Britain. Ireland is excluded due to the insufficient quality of the data available. A wider group of countries, extending as far as Greece and Finland, was also studied: the inclusion of countries further away than the 15 selected, whose power systems are relatively small compared with France’s, does not substantially alter the results presented here.

12

The foundations of the approach used in this section are set out in detail in: J Bialek, Tracing the flow of electricity, 1996.

14

Exports to Switzerland may be re-exported, particularly to Italy. See: RTE, 2023 Electricity Review – Trading chapter – Focus: Switzerland, a transit country for electricity, 2023

Section externalisée

Menu tertiaire

Paragraphes de la section

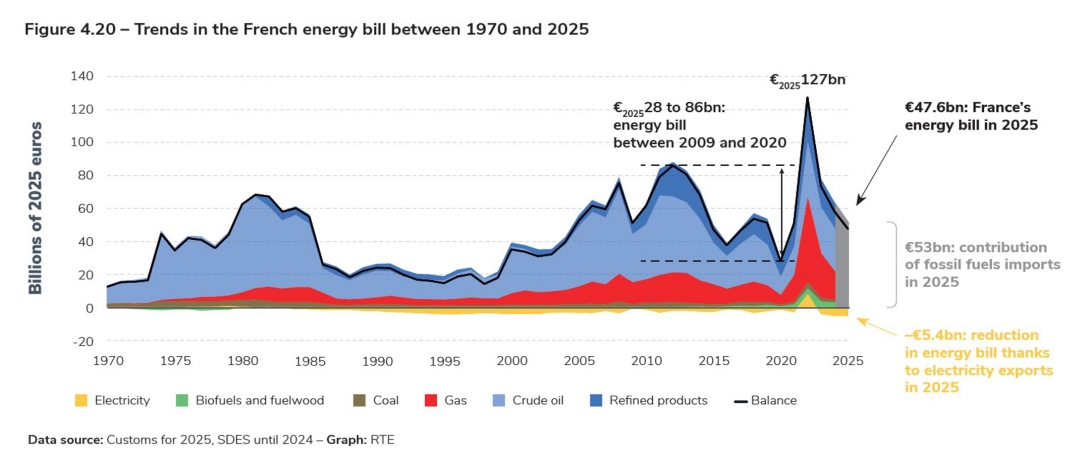

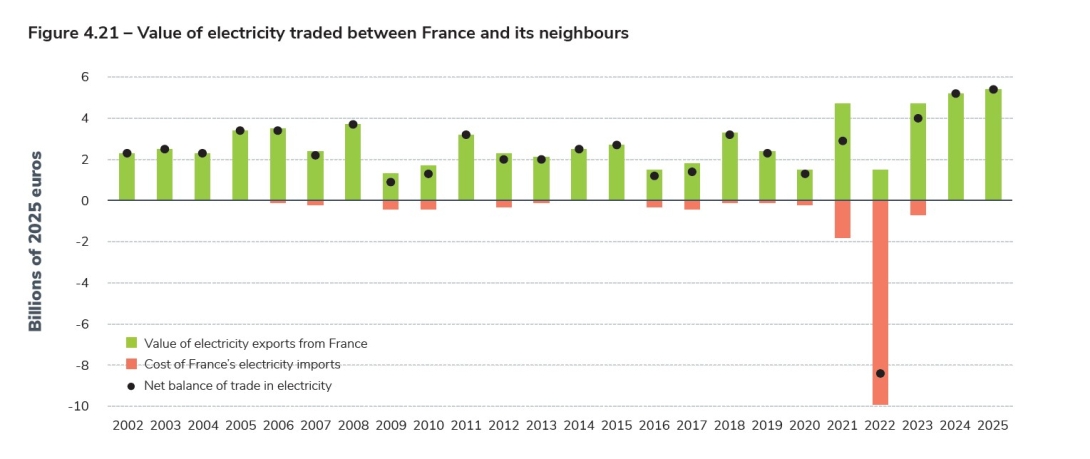

The value of trade is increasing, but remains low compared to the cost of fossil fuel imports

The total net value of France's electricity exports amounted to €5.4 billion in 2025 (or around €9 billion taking into account the average price in the countries to which France exports), a level slightly higher than the previous year. This amount helps to reduce France's “energy bill”, but it is still low compared with the cost of fossil fuel imports, which represent the largest heading in France's trade deficit. In 2025, fossil fuel imports cost €53 billion15. In 2022, they amounted to over €2025110 billion in the context of the energy crisis; by comparison, the fact that France was, unusually, an electricity importer that year only cost around €20258 billion.

As the findings of the latest 2025 Generation Adequacy Report published by RTE also make clear, this provides a valuable opportunity to take advantage of the abundance of low-cost, low-carbon electricity generation to decarbonise the French economy by replacing fossil fuels, which still account for almost 60% of the energy consumed in France. Electrifying energy uses would enable French consumers to benefit from low-cost electricity generation, strengthen the country's energy sovereignty and shield it from the volatility of fossil fuels prices resulting from events affecting the global economy.

Between 2002 and 2019, the annual net value of France’s electricity trade fluctuated between €20251 and 3 billion. From 2021 onwards, the effect of the energy crisis in Europe became apparent: the value of the electricity traded by France rose sharply, driven primarily by prices. In 2024, falling prices partly offset the effect of higher export volumes. In 2025, the value of electricity trading between France and its neighbours was slightly higher, due to a higher export balance and prices that were also slightly higher.

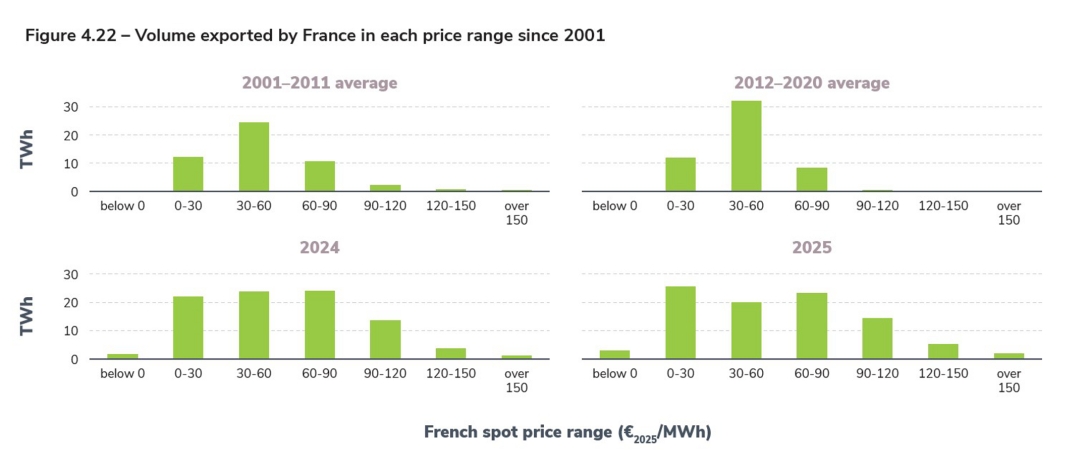

As a result of increased price volatility, volumes traded at relatively high prices increased (23% of volumes were exported at prices above €202590/MWh, compared with 20% in 2024 and less than 1% over the 2012–2020 average). Volumes traded at relatively low prices also increased slightly (13% of the volumes exported were at prices below €202510/MWh, compared with 12% in 2024 and 1% over the 2012– 2020 average).

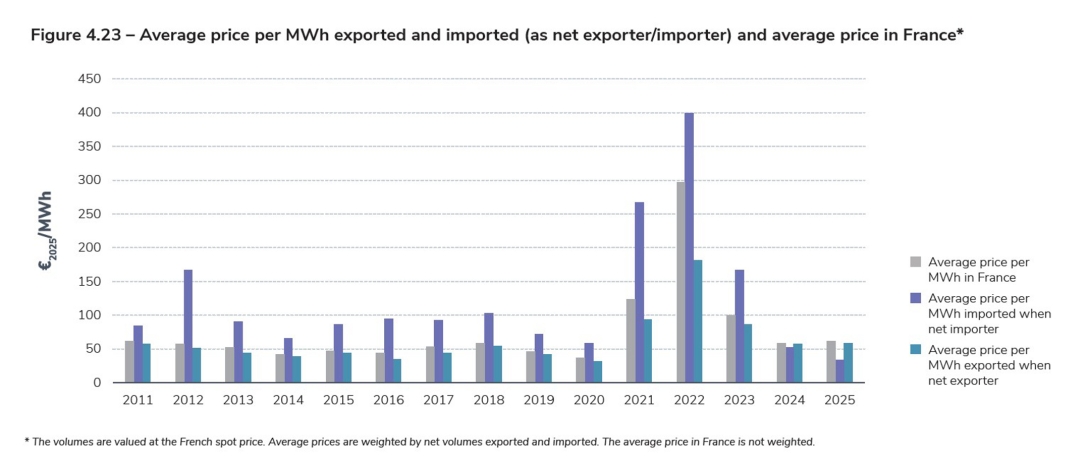

Historically, since the markets were opened up in 2002, the average spot price when France was a net exporter16 has been lower than the price when France was a net importer. This is because most of the periods when France imported electricity corresponded to periods of high consumption, when prices also tend to be higher. This situation was reversed in 2024 and even more so in 2025: thanks to the abundance of low-carbon generation in France, there were only rare periods when France was a net importer (around 100 hours in 2025). During these times, France was mainly importing due to the abundance of renewable generation in neighbouring countries, which meant that half of these hours were characterised by negative prices. The average import price17 was €33/MWh, the lowest level since the markets opened.

The average price per MWh exported in 2025 (€59/MWh at the French price) is close to the average French spot price (€61/MWh). It remains close to the levels of the previous year and slightly higher than during the 2010s. Valued at the average price in the countries to which France exports, on the other hand, it came to €101.5/MWh. So, as in 2024, France did not “dump” its electricity at rock-bottom prices in 2025: it exported its competitive surplus production almost continuously, benefiting from a higher price differential with neighbouring countries than in 2024.

15

Source: Customs

16

I.e. when France is exporting more electricity than it is importing. When France is a net exporter, it is possible that it may still be importing across one or more of its borders.

17

I.e. the average of the spot prices weighted by the corresponding traded volumes, over the time intervals when France is a net importer (i.e. only 0.2 TWh)